Featured Research

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a...

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

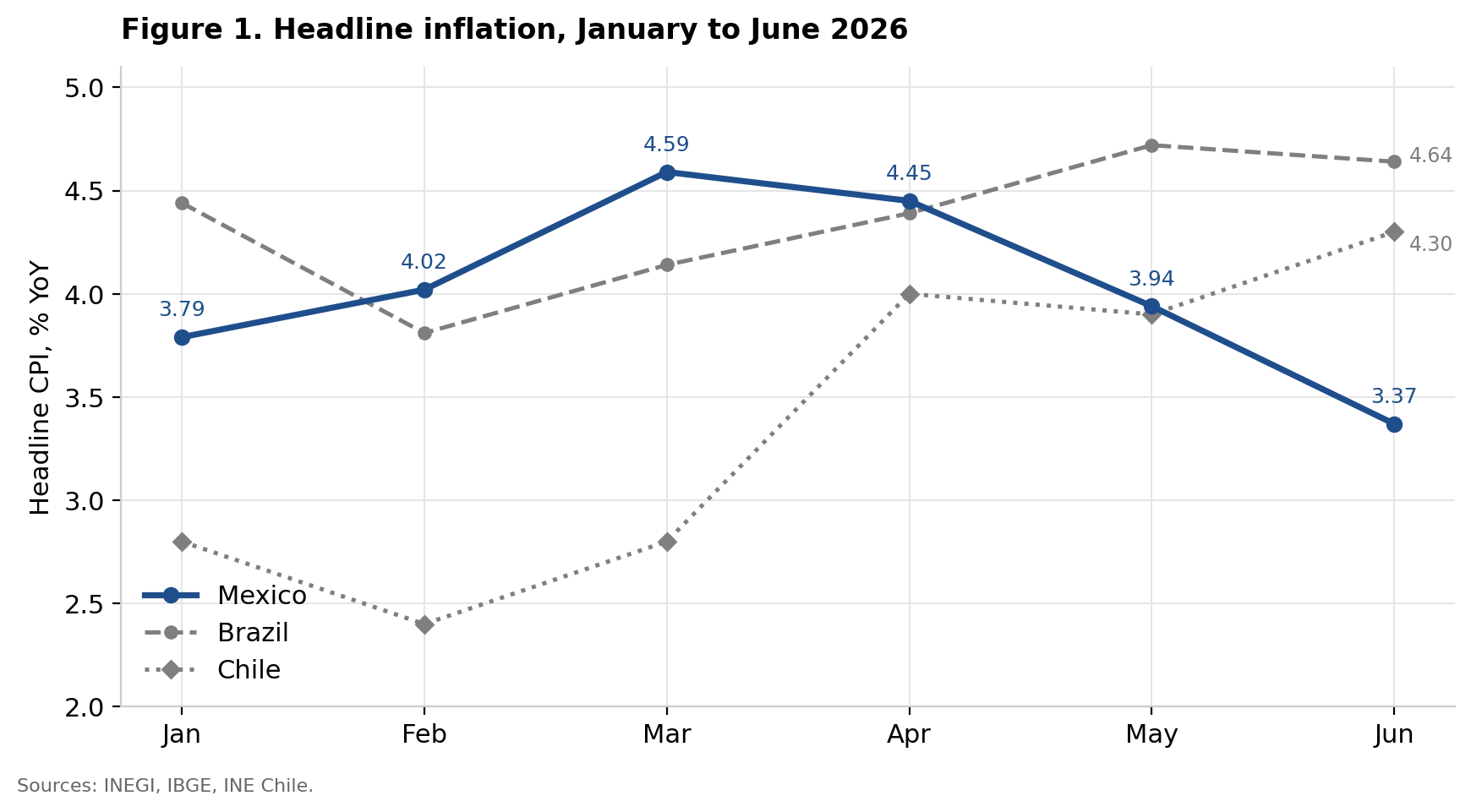

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a second escalation in July pushed Brent back towards USD 97, a rise of nearly 40% on the month. For Latin America’s oil importers this amounts to a substantial imported inflation shock. Chilean inflation has climbed from a five-year low of 2.4% in February to 4.3% in June, its highest since September 2025, while Brazilian inflation stood at 4.64% in June with energy and fuel inflation running at 7.71%.

Mexico has moved in the opposite direction, with headline inflation falling to 3.37% YoY in June from 3.94% in May despite having entered the shock with the highest rate of the three economies, peaking at 4.59% in March. Mexico has largely absorbed the oil shock through weekly adjustments to fuel subsidies and administered price agreements, while underlying core inflation has remained broadly stable.

A Common Shock, Three Outcomes

Central banks and statistical agencies in Chile and Brazil have linked the recent rise in inflation to the energy and production-cost effects of the Middle East conflict. Banco Central de Chile notes that inflation excluding food and energy remains close to its 3% target, while Brazil’s statistical agency, IBGE, attributes higher energy and fuel inflation to the closure of the Strait of Hormuz. Differences in monetary policy do not fully explain Mexico’s divergence from these peers. Banco de México held its policy rate at 7% in February, cut it to 6.75%, and ended its easing cycle in May. Despite this less restrictive stance relative to Brazil, Mexican headline inflation has continued to fall while inflation in Chile and Brazil has risen.

Where the Recent Disinflation Sits

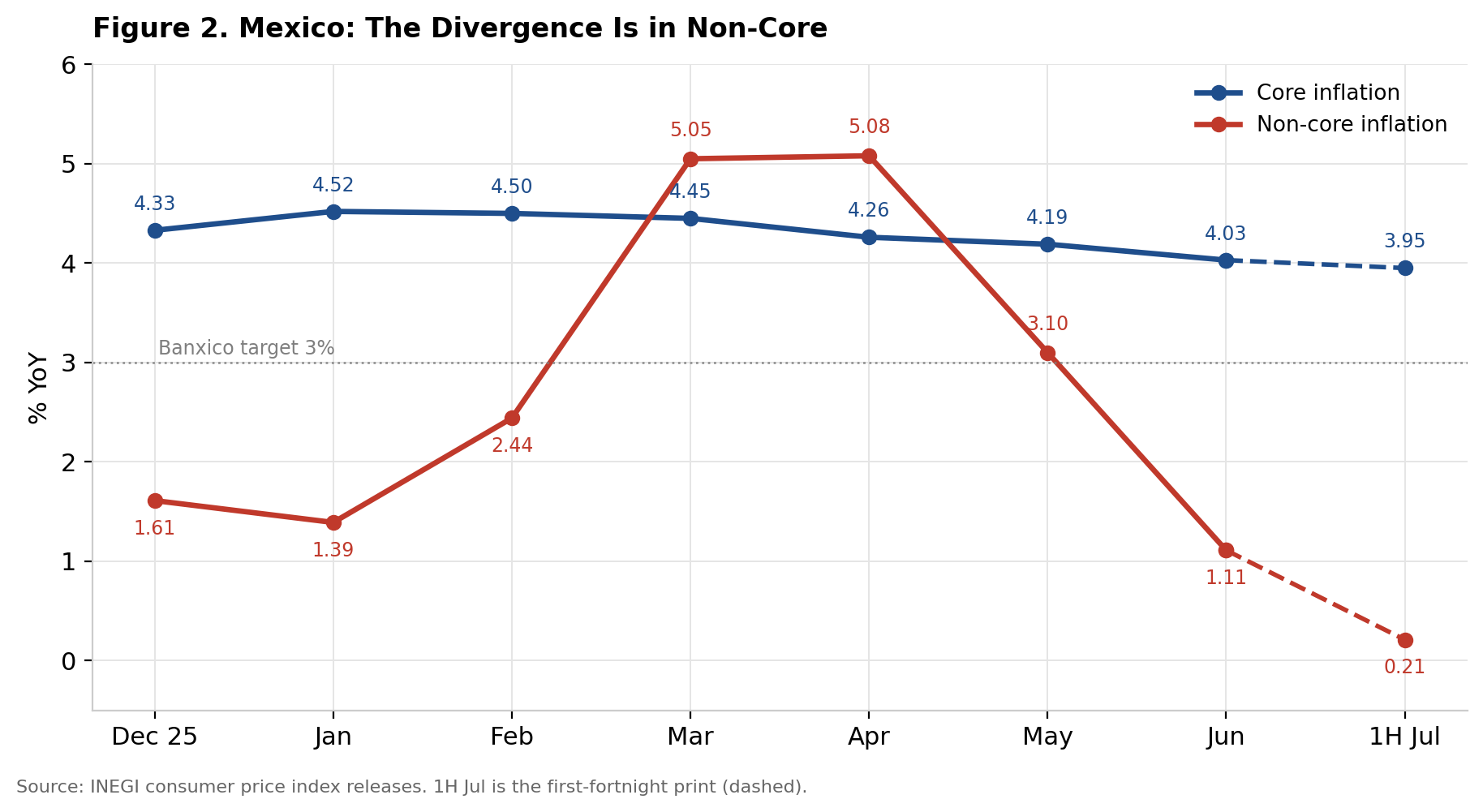

The composition of Mexico’s June inflation print shows that the divergence is concentrated in non-core components. Core inflation stood at 4.03%YoY, compared with just 1.11% for non-core inflation. While core inflation has eased only gradually from 4.52% in January, non-core inflation has fallen sharply from 5.08% in April to close to 1% in June. Fruit and vegetable prices declined 8.99%MoM as crop conditions normalised and government agreements with producers took effect. At the same time, energy prices and government-authorised tariffs rose by only 0.08% despite the oil shock, following a 1.67% decline in May driven by seasonal electricity tariff reductions. Mexico’s headline disinflation has therefore not come from a broad easing in underlying price pressures. It has been driven mainly by volatile and administered components, particularly food, energy and regulated tariffs.

A Weekly Excise Subsidy

The main instrument absorbing the shock is the fiscal stimulus applied to the Special Tax on Production and Services, or IEPS, on motor fuels. Under this mechanism, the Secretaría de Hacienda y Crédito Público publishes a weekly agreement in the Diario Oficial de la Federación specifying the share of the fixed per-liter excise tax absorbed by the federal government. The measure functions as a contingent shock-absorption tool rather than a permanent subsidy. It was withdrawn on April 12, 2025, and remained at zero for 48 consecutive weeks through nearly a year of normal price fluctuations. It was reinstated on March 13, 2026, within days of the closure of the Strait of Hormuz, and has since been adjusted weekly in response to movements in international crude prices. Because the comparison period contained no subsidy, each YoY reading from March onward compares subsidized fuel prices with an unsubsidized base. The resulting downward wedge in fuel inflation will therefore persist for as long as the stimulus remains in place.

Sizing the Wedge

To read the rest of this analysis, visit our latest Substack post, here.

Research Archive

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to...

Macroeconomic Insights: The Red Sea Escalation, the Tariff Regime Reset and the U.S. Inflation Path

The new round of United States tariffs will not add materially to inflation. The 10% Section 122 surcharge lapses today, 24 July 2026, and the Office of the United States Trade...

Macroeconomic Insights: UK Policy Package and the Underlying Inflation Picture

UK CPI printed at 2.6% YoY in June 2026, but the composition of that print sits uncomfortably against a broader policy package now working its way through the price level....

Macroeconomic Insights: The Oil Shock Could Spread Beyond Hormuz

The oil shock has entered a more complicated phase. Since late February, when the US and Iran conflict began, shipping through the Strait of Hormuz has been severely restricted,...

Imperial College Hedge Fund Conference 2026

I’ve been to many finance conferences over the years, very often they are either focused towards academia or towards practitioners. The Imperial College hedge fund conference has...

Macroeconomic Insights: US CPI – The Strange Swing in U.S. Cell Service Prices

The wireless telephone services component of US CPI has been behaving strangely over the past year. The recent behaviour is really two things stacked on top of a long structural...

Macroeconomic Insights: Colombia CPI — Inflation After the Election

De la Espriella's narrow runoff win prompted the market to price a more orthodox, pro-business stance. That meant a stronger peso and lower risk premia, with a chance of...

Macroeconomic Insights: FIFA World Cup and Inflation, Where Anything Can Happen

Every time I watch the FIFA World Cup, there's always something that surprises me. I didn't expect Japan to score against Brazil in the first half, nor did I expect Cape Verde to...

Macroeconomic Insights: El Niño and the Inflation Outlook for the Year Ahead

A developing El Niño is becoming an important force in the inflation outlook over the next year. By shifting global rainfall patterns, it can bring drought to some regions and...

ECONDAT 2026 at Banque de France

I've been to Paris many times over the years. Each time I’ve visited I’m always surprised at how much I still have to learn about the City of Light. I always say I’ll learn about...

Macroeconomic Insights: What Comes Up, Must Come Down?

Today, the United States and Iran have signed a deal ending the war. Among the many points outlined in the agreement, the normalization of trade through the Strait of Hormuz,...

Neudata Summer Data Summit 2026

“Be obsessed with data”, was probably the best line I heard all day at the recent Neudata data summit in New York. I went to my first Neudata event close to a decade ago in...

Macroeconomic Insights: Where Will the Oil Shock Hit Next?

Turnleaf reads the current inflation data as a test of duration. Fuel prices have lifted headline CPI, while core has stayed contained because energy prices have not remained...

Macroeconomic Insights: The Hidden Cost of the Iran War

Over the past several months, Turnleaf has examined the inflationary impact of the Iran conflict across fuel, food and airline prices, as well as the intermediary inputs that...

Macroeconomic Insights: How the Hormuz Closure is Moving Airfares

The Strait of Hormuz closure is best understood as an inflation shock transmitted through energy logistics. The relevant issue is that usable supply has become harder to move and...