Since the outbreak of the Hormuz conflict in early March 2026, media coverage has understandably centered on oil prices and their pass-through to fuel and transportation costs. Less attention has been paid to other commodities transiting the Strait, notably urea and nitrogen-based fertilizers, which are critical inputs for global food production. In previous Substack posts we noted that food price responses to supply shocks of this kind tend to lag by several months, buffered by existing inventories, forward contracts, and harvest cycles. Still, the risk warrants close monitoring.

Using Turnleaf’s proprietary food price indices, which track daily supermarket and scanner data across 25 countries, we can now offer a first empirical snapshot (Figure 1). Since March 1, 2026, Turnleaf’s food indicies have risen by at least 1% in over half the countries we cover. The outliers at the top of the table, Peru at +13.2% and Turkey at +9.9%, are almost certainly driven by domestic factors rather than the oil shock itself. Across the rest of the distribution, increases are modest and broadly consistent with pre-crisis trends. At the other end, several Asian economies including Japan, the Philippines, South Korea, and China have actually seen food indices decline over the period.

Figure 1 – visit our latest Substack post, here

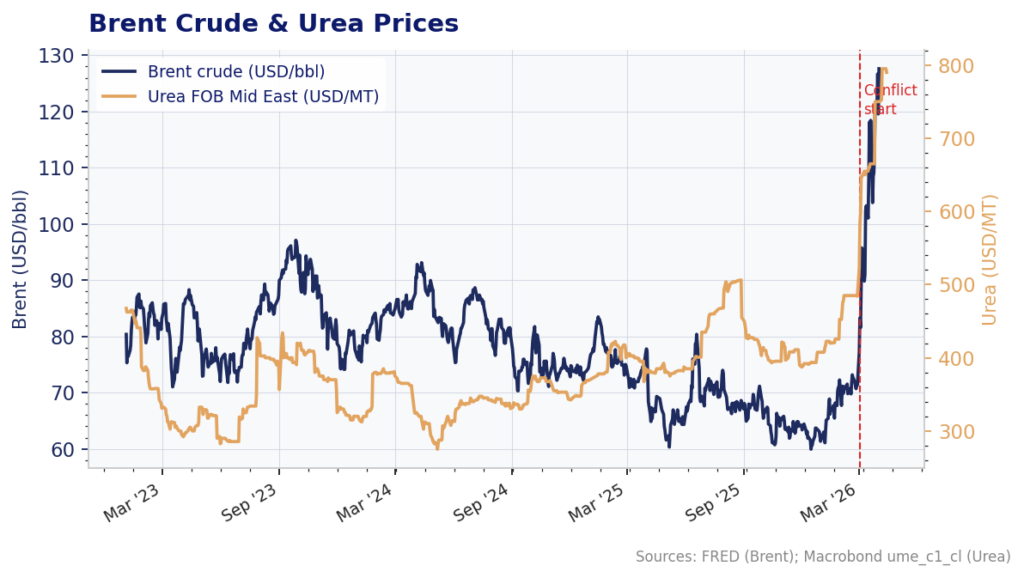

In short, there is no clear evidence that the Hormuz disruption is feeding through to retail food prices just yet. But the forward-looking picture is less reassuring. Urea spot prices have surged from roughly $500/MT to close to $800/MT in under six weeks, a move that, if sustained, will eventually reach farm-gate input costs and from there the supermarket shelf (Figure 2). We will continue tracking these indices closely in the months ahead.

Figure 2