First the Philippines, now Thailand. Who falls next? We take a closer look at how the Iran oil shock is reshaping the 12-month inflation outlook across Asia, and why rising rice demand could further intensify upside risks.

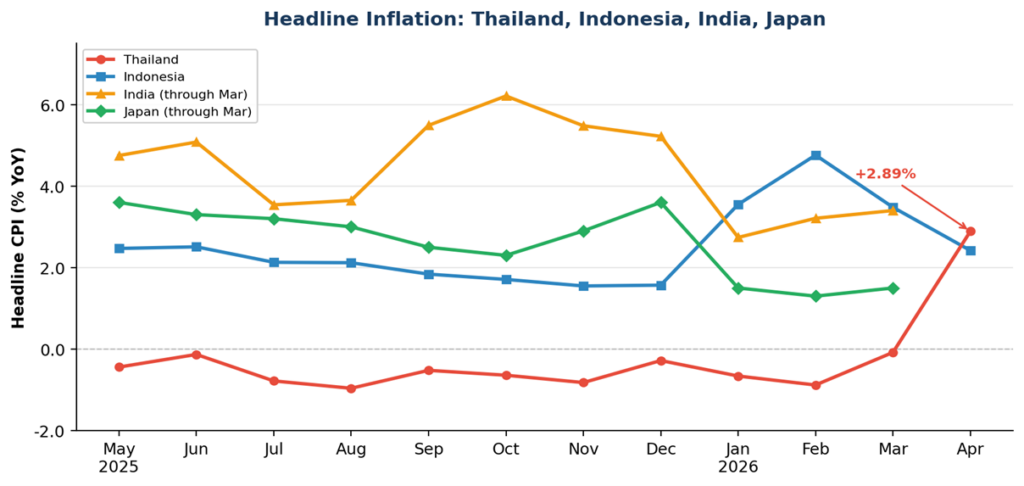

Thailand ran twelve consecutive months of negative headline inflation through March 2026. In April, CPI swung to positive 2.89 percent year on year, a three-year high that pushed the reading toward the upper bound of the Bank of Thailand’s 1 to 3 percent target range. The non-food-and-beverage component rose 4.14 percent, driven by fuel and transport fares, while core inflation accelerated to 0.83 percent from 0.57 percent in March. For now, this is still mostly the first-order fuel channel. The rice channel is slower. It starts with input costs, moves through planting decisions, and only later shows up in harvest volumes, exportable surplus, and food CPI.

Source: National statistics offices. India and Japan April data not yet released at time of writing.

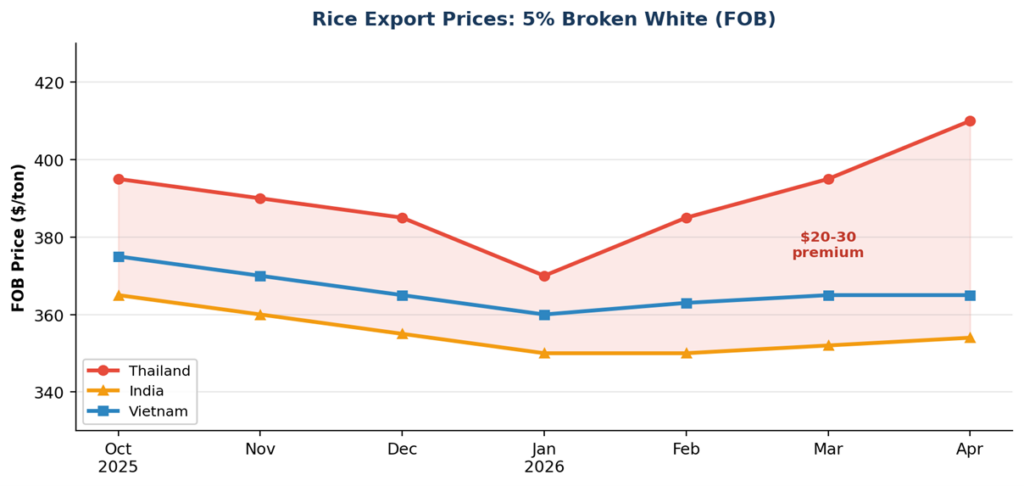

Thailand sets the benchmark price for global rice, and it is losing both volume and margin. The Thai Rice Exporters Association cut its 2026 target to 7.03 million tons, down 11 percent from the 7.9 million shipped in 2025 and the lowest figure in five years. January exports fell 17.5 percent year on year, with export value down 30.7 percent in baht terms.

The pressure starts with producer costs. Thai farmers are roughly 90 percent reliant on imported fertilizer, and when the Strait of Hormuz closed in late February, granular urea jumped from a pre-war range of $400 to $490 per metric ton to roughly $700. That pass-through is already showing up in farm-gate economics, with farmers in central Thailand reporting production costs up 20 to 30 percent and some cutting fertilizer application in half during the May-to-August transplanting window that governs the next harvest. The yield effect is not mechanical. Weather, water availability, and state support can still overwhelm any single input. But fertilizer cuts of that size, if sustained through transplanting, are exactly the kind of adjustment inflation models miss until the crop is already in the ground.

Hence, Thai 5 percent broken white rice is now quoted at $385 to $410 per ton FOB, $20 to $30 above comparable Indian and Vietnamese grades, a premium wide enough to divert buyers (Figure 2). But the more important signal for inflation forecasting is what happens to yields if farmers keep fertilizer use materially below normal levels. That adjustment does not appear in current prices, but it can surface in the next harvest through lower yields, tighter exportable surplus, and a higher floor under the export price curve.

Source: Thai Rice Exporters Association, trade press. Approximate FOB quotes for 5% broken white rice.

Indonesia faces the same compounding dynamics we documented in the Philippines. Its statistics bureau estimated that rice harvest area from March to May would shrink by 10.6 percent, with unhusked rice output down 11.12 percent. Unlike Thailand, Indonesia cannot pass the cost through to export markets. It absorbs the shock domestically. April headline CPI came in at 2.42 percent, down from 3.48 percent in March, but that moderation is partly a policy result, not a clean disinflation signal. The finance minister warned explicitly that removing fuel subsidies would cause inflation to spike, and transport costs were already the largest monthly contributor. The government is absorbing a rising fiscal cost to hold headline inflation inside the central bank’s 1.5 to 3.5 percent target range. Fuel subsidies appear to be materially suppressing the April pass-through.

To read the rest, visit our latest Substack post, here.