Featured Research

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a...

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

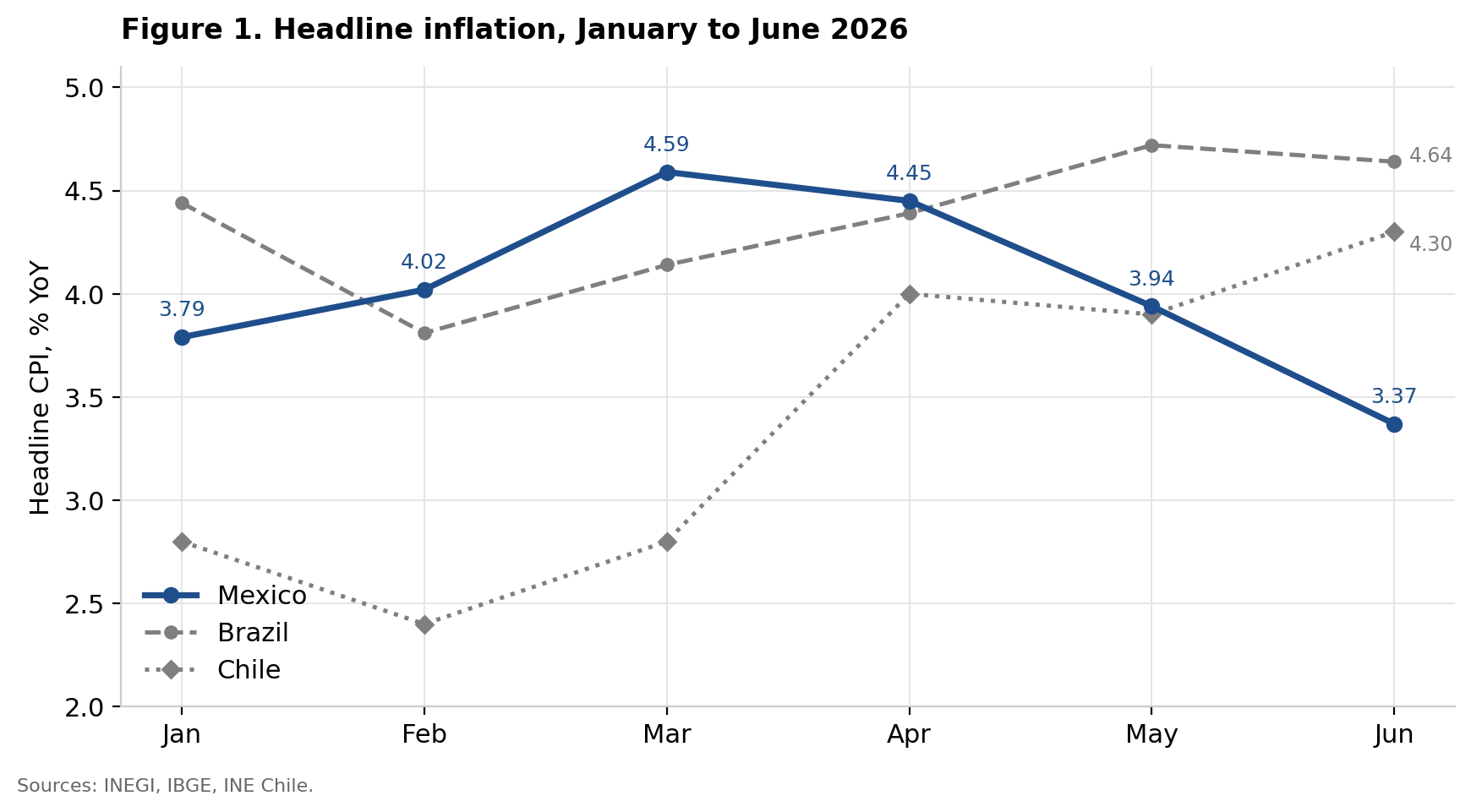

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a second escalation in July pushed Brent back towards USD 97, a rise of nearly 40% on the month. For Latin America’s oil importers this amounts to a substantial imported inflation shock. Chilean inflation has climbed from a five-year low of 2.4% in February to 4.3% in June, its highest since September 2025, while Brazilian inflation stood at 4.64% in June with energy and fuel inflation running at 7.71%.

Mexico has moved in the opposite direction, with headline inflation falling to 3.37% YoY in June from 3.94% in May despite having entered the shock with the highest rate of the three economies, peaking at 4.59% in March. Mexico has largely absorbed the oil shock through weekly adjustments to fuel subsidies and administered price agreements, while underlying core inflation has remained broadly stable.

A Common Shock, Three Outcomes

Central banks and statistical agencies in Chile and Brazil have linked the recent rise in inflation to the energy and production-cost effects of the Middle East conflict. Banco Central de Chile notes that inflation excluding food and energy remains close to its 3% target, while Brazil’s statistical agency, IBGE, attributes higher energy and fuel inflation to the closure of the Strait of Hormuz. Differences in monetary policy do not fully explain Mexico’s divergence from these peers. Banco de México held its policy rate at 7% in February, cut it to 6.75%, and ended its easing cycle in May. Despite this less restrictive stance relative to Brazil, Mexican headline inflation has continued to fall while inflation in Chile and Brazil has risen.

Where the Recent Disinflation Sits

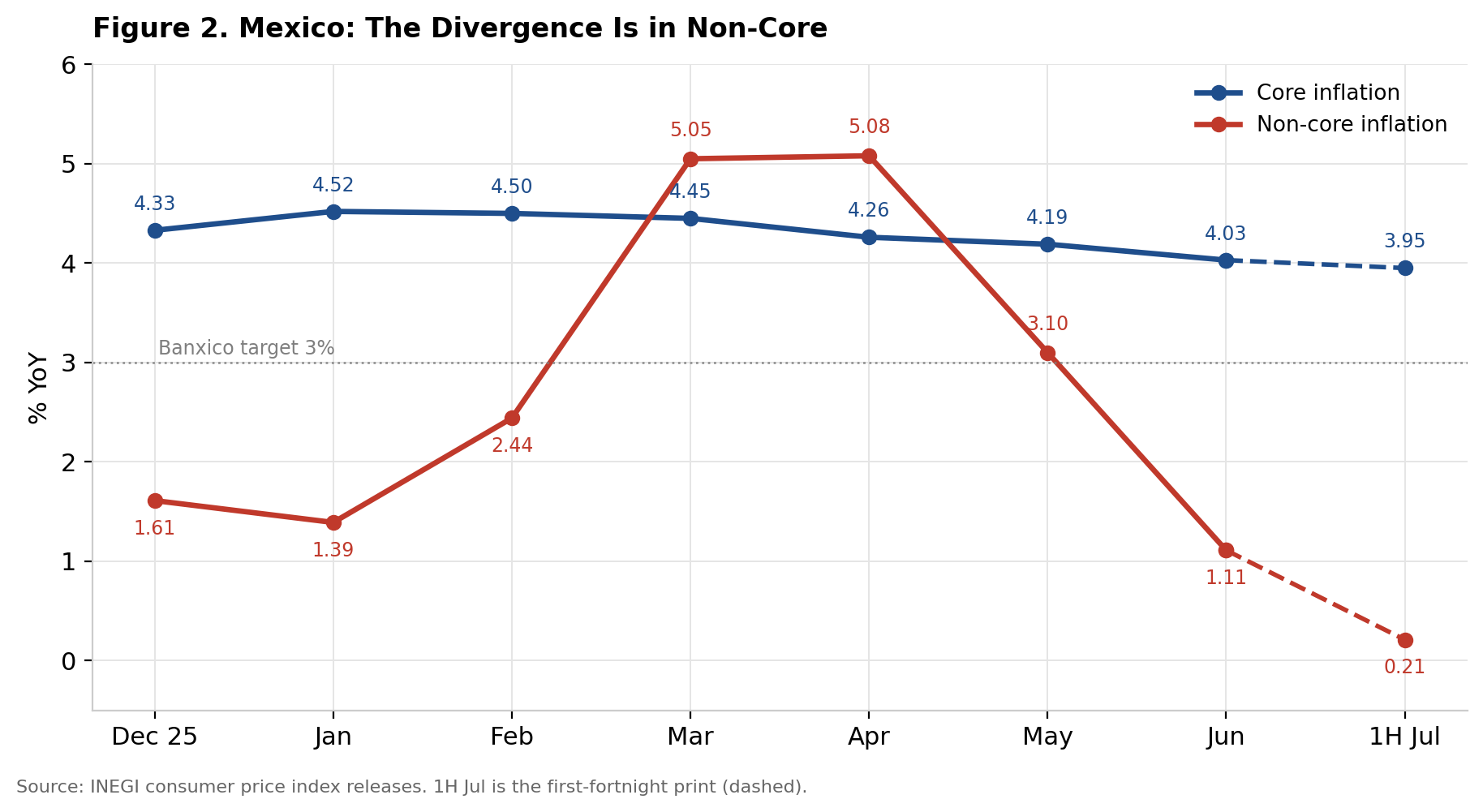

The composition of Mexico’s June inflation print shows that the divergence is concentrated in non-core components. Core inflation stood at 4.03%YoY, compared with just 1.11% for non-core inflation. While core inflation has eased only gradually from 4.52% in January, non-core inflation has fallen sharply from 5.08% in April to close to 1% in June. Fruit and vegetable prices declined 8.99%MoM as crop conditions normalised and government agreements with producers took effect. At the same time, energy prices and government-authorised tariffs rose by only 0.08% despite the oil shock, following a 1.67% decline in May driven by seasonal electricity tariff reductions. Mexico’s headline disinflation has therefore not come from a broad easing in underlying price pressures. It has been driven mainly by volatile and administered components, particularly food, energy and regulated tariffs.

A Weekly Excise Subsidy

The main instrument absorbing the shock is the fiscal stimulus applied to the Special Tax on Production and Services, or IEPS, on motor fuels. Under this mechanism, the Secretaría de Hacienda y Crédito Público publishes a weekly agreement in the Diario Oficial de la Federación specifying the share of the fixed per-liter excise tax absorbed by the federal government. The measure functions as a contingent shock-absorption tool rather than a permanent subsidy. It was withdrawn on April 12, 2025, and remained at zero for 48 consecutive weeks through nearly a year of normal price fluctuations. It was reinstated on March 13, 2026, within days of the closure of the Strait of Hormuz, and has since been adjusted weekly in response to movements in international crude prices. Because the comparison period contained no subsidy, each YoY reading from March onward compares subsidized fuel prices with an unsubsidized base. The resulting downward wedge in fuel inflation will therefore persist for as long as the stimulus remains in place.

Sizing the Wedge

To read the rest of this analysis, visit our latest Substack post, here.

Research Archive

Macroeconomic Insights: How the Hormuz Closure is Moving Airfares

The Strait of Hormuz closure is best understood as an inflation shock transmitted through energy logistics. The relevant issue is that usable supply has become harder to move and...

Macroeconomic Insights: Food Prices Have Moved Past the Ceasefire Question

Since the onset of the March 2026 escalation in the Gulf/Iran conflict, markets have focused overwhelmingly on oil, with Brent pushing past $100 per barrel. Headlines on the war...

Macroeconomic Insights: Repricing Conflict, Inflation Next

On April 17, markets briefly priced in peace. Iran had declared the Strait of Hormuz open, a Lebanon ceasefire had just started, and WTI dropped 6% in a day. Prediction markets...

The choice decision

You always have choices. Should I order cheese in my burger? Should I choose the cheese or cream knafa? There are also additional choices, not immediately obvious from the menu....

Macroeconomic Insights: Mexico CPI— Fuel Smoothing Muting the Shock, Local Prices Still Bite

Turnleaf’s Mexico CPI nowcast for May 2026 is 4.04 percent YoY, slightly below Banxico nowcast of 4.09 percent YoY. Figure 1 shows a softer near-term profile, with the model...

Macroeconomic Insights: Where the Rice Shock Travels Next

First the Philippines, now Thailand. Who falls next? We take a closer look at how the Iran oil shock is reshaping the 12-month inflation outlook across Asia, and why rising rice...

Macroeconomic Insights: Philippines CPI — Who Is Falling First?

Philippines inflation has become a test case for how rapidly an external supply shock can propagate through a domestic food system. The April print was a material upside...

Macroeconomic Insights: Hungary CPI – Orban Out, Magyar In

Hungary’s inflation outlook over the next 12 months is increasingly shaped by a transition away from direct price controls toward a more mixed regime combining gradual...

Macroeconomic Insights: Turnleaf’s Guide to Understanding the Hormuz Shock

The shock has already landed Despite conflicting announcements about whether the Strait of Hormuz may close, vessel traffic remains underwhelming and supply concerns persist....

Macroeconomic Insights: Are Global Food Prices on Their Way Up?

Since the outbreak of the Hormuz conflict in early March 2026, media coverage has understandably centered on oil prices and their pass-through to fuel and transportation costs....

Macroeconomic Insights: Oil Prices and Inflation– Will the Ceasefire Last?

To gauge how markets are pricing the durability of the current US-Iran ceasefire, we aggregated conflict resolution probabilities across four prediction market platforms...

Macroeconomic Insights: There’s No Ceasefire for Inflation

Late last night (April 7, 2026), the U.S. and Iran agreed on a two-week ceasefire to allow for diplomacy. During this time, Iran has agreed to coordinate the passage of vessels...

Macroeconomic Insights: Hormuz Shock and the Return of Global Inflation (Expectations?)

The closure of the Strait of Hormuz following the US-Israeli strikes on Iran on 28 February 2026 has triggered the largest physical supply disruption in the history of the global...

Neudata London March 2026

A decade ago, I liked burgers, and a decade on, well, I still like burgers. However, one thing that has changed greatly has been the alternative data market. What was once an...

Macroeconomic Insights: Spain CPI Downside Surprise and Energy Tax Cuts

Spain headline CPI YoY jumped sharply to 3.3% YoY in March 2026 from 2.3% in February entirely on the back of energy price reversals linked to the Iran conflict and Strait of...