Featured Research

Macroeconomic Insights: How the Hormuz Closure is Moving Airfares

The Strait of Hormuz closure is best understood as an inflation shock transmitted through energy logistics. The relevant issue is that usable supply has become harder to move and more expensive to deliver. Prices are set by accessible supply, and the closure has...

Macroeconomic Insights: How the Hormuz Closure is Moving Airfares

The Strait of Hormuz closure is best understood as an inflation shock transmitted through energy logistics. The relevant issue is that usable supply has become harder to move and more expensive to deliver. Prices are set by accessible supply, and the closure has materially reduced the volume of crude and refined product reaching end markets.

Inventories are absorbing the first stage of the disruption. Commercial stocks and strategic reserves can keep the system operating while Gulf flows are constrained, but as buffers are drawn down the market becomes more sensitive to each additional delay or outage. The cost of keeping aviation operating rises even before any visible supply shortage materializes.

Airlines do not wait for supply constraints to materialize before adjusting pricing behavior. Cheap fare buckets are removed first, average fares rise second, and capacity is cut last. A market can appear operationally normal while already becoming inflationary.

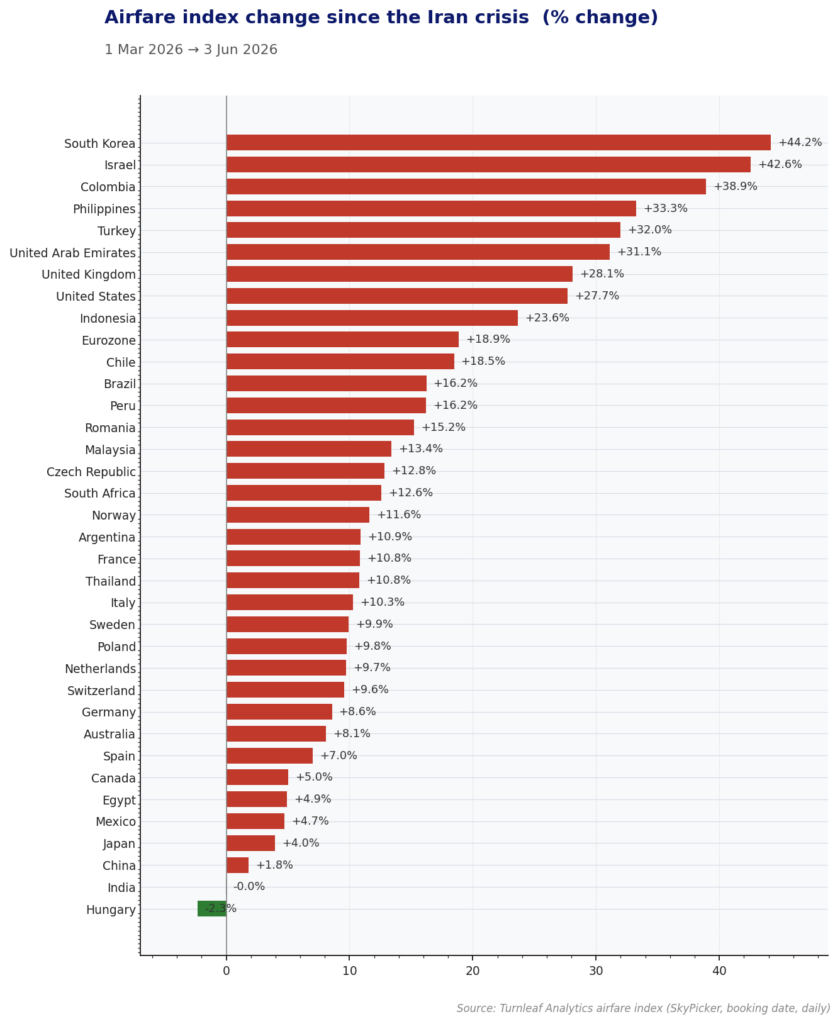

Turnleaf’s airfare indices measure the change in fares before and after the Strait closure (Figure 1). Since March 1, South Korea is up 44.2%, Israel 42.6%, and Colombia 38.9%, with most other markets in the sample showing increases in the range of 10 to 28%. Hungary is the only market to show a decline, at -2.3%.

Figure 1

The distribution is not a proximity ranking. South Korea and Colombia rank among the most affected markets despite their distance from the Gulf, with exposure running through imported energy dependence and dollar-priced fuel procurement. The muted readings at the bottom — Japan at +4.0%, China at +1.8%, India flat — likely reflect larger domestic reserve buffers absorbing the shock rather than low structural exposure.

The key signal to monitor is whether pressure broadens beyond long-haul markets into short-haul and domestic routes. We will continue to update the index daily and flag any evidence of acceleration.

Research Archive

Takeaways from QuantMinds 2024 in London

Over the past years, the quant industry has changed substantially. My first visit to Global Derivatives was just over a decade ago. At the time, perhaps unsurprisingly, the...

Macroeconomic Insights – Poland’s Fight with External and Domestic Demand

As Poland navigates a complex economic landscape, its rapid growth, fueled by competitive wages and strong manufacturing, faces challenges from both domestic and external...

Takeaways from Web Summit 2024

Think of Lisbon and no doubt it’ll conjure images of explorers setting sail in centuries past across the ocean, the hills that climb across the city, pastel de nata and salted...

Macroeconomic Insights: UK Autumn 2024 Budget and Global Trade Pressures Add to Inflation Challenges

The UK government's Autumn Budget for 2024, introduced on October 30, is designed to enhance public services through increased capital investments, funded by higher taxes along...

Macroeconomic Insights: U.S. Inflation Outlook Under Another Trump Presidency

As U.S. economic conditions continue to evolve, Turnleaf will actively monitor inflation trends and publish regular updates to keep you informed. Our focus remains on leading...

Macroeconomic Insights: Turkey’s Two-Front Fight with Inflation and the Lira

Turkey’s central bank has adopted a stringent monetary policy to combat inflation, a stark departure from previous unorthodox strategies. With borrowing costs now at a benchmark...

Inflation Outlook for Canada in October 2024- Producer Optimism, Consumer Pains

Canada’s inflation outlook is shaped by a complex mix of declining energy costs, rising food prices, and evolving trade dynamics. At Turnleaf Analytics, we’re closely tracking...

How Bad is Too Bad? Japan’s Reckoning with Inflation and New Leadership

Japan’s battle with inflation has become a key issue, reshaping public sentiment and influencing recent election results. With the Liberal Democratic Party (LDP)–Komeito...

Turnleaf’s Inflation Outlook for Brazil: Rising Costs Amid Currency Pressures

Turnleaf’s Brazil’ inflation outlook for the next 12 months has undergone an upward revision, driven by several significant factors. While shipping costs have eased, inflationary...

Turnleaf’s October 2024 Economic Forecast: Deflationary Pressures Persist in China

Turnleaf Analytics’ forecast for YoY NSA CPI published in October 2024 suggests an inflation trajectory expected to remain well below 2% over the coming 12 months. Specifically,...

FILS Europe 2024 Takeaways

Paris is home to many things, the Eiffel Tower, the Arc de Triomphe, burgers (ok, I made that one up!). In recent years, Paris' financial community has grown, and indeed, every...

Don’t look back in hanger steak

I'm currently in the queue for Oasis tickets. Rather than mindlessly watching the counter of people in the queue ahead of me fall (currently 184,984 people), I thought I'd start...

The Olympic spirit for forecasting

The Olympics finally finished, and the Paralympics are about to begin. I managed to go to some of the Olympic football matches in both Lyon (in the photo above) and Nice. The...

Eleven years of independence

Regrets become ever more edged with the passing of time. Recalling a time long gone, when perhaps a decision made, was not the decision you should have made, wastes little more...

The human part of machine learning forecasts

I've seen a few videos showing a robot making a burger (here's one of RoboBurger for example). It seems pretty impressive that a machine can create a fresh burger. However, one...