Featured Research

Macroeconomic Insights: Strait of Hormuz and the Inflation Shock Markets Are Repricing

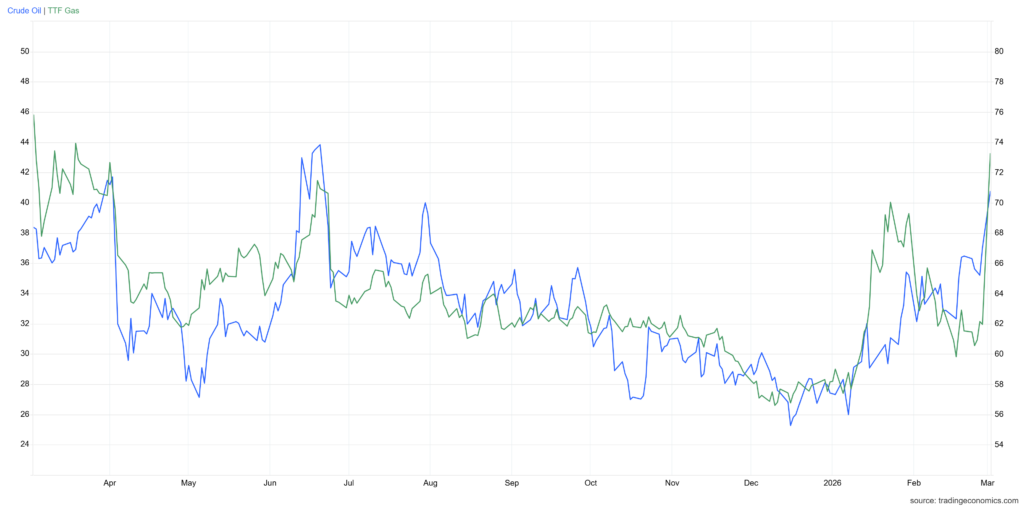

The US-Israel strike on Iran has pushed Middle East risk back to the center of global pricing. Crude has firmed into the low 70s while European gas prices spiked, and gold has extended an already sustained uptrend with a burst of volatility that suggests investors are...

Macroeconomic Insights: Strait of Hormuz and the Inflation Shock Markets Are Repricing

The US-Israel strike on Iran has pushed Middle East risk back to the center of global pricing. Crude has firmed into the low 70s while European gas prices spiked, and gold has extended an already sustained uptrend with a burst of volatility that suggests investors are actively rotating toward hard-asset hedges (Figure 1). For net energy importers, the near-term inflation distribution has shifted meaningfully to the upside.

Whether that shift proves transitory or persistent depends on duration. Futures markets have already repriced, but the physical supply layer has not yet confirmed or contradicted what is being priced. Turnleaf is monitoring that gap using high-frequency AIS-based routing, port call data, and commodity prices.

Figure 1

How the Twelve-Day War Priced Through to CPI

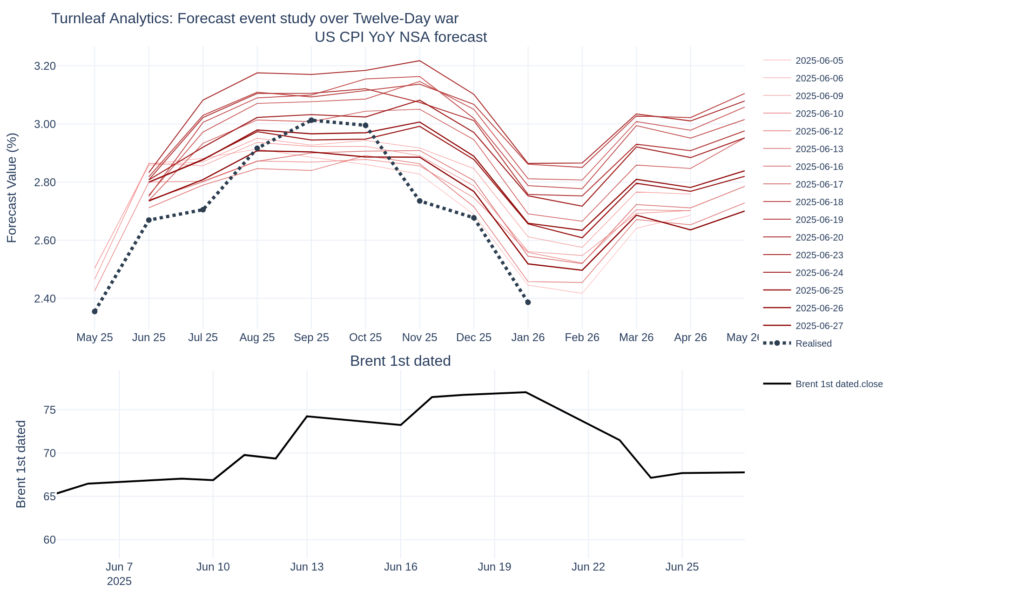

The June 2025 Twelve-Day War provides the most recent comparable template for how an energy shock of this kind transmits into consumer prices. As Brent crude rose approximately 10 dollars per barrel over the course of that conflict, Turnleaf’s daily US CPI year-on-year NSA forecast curve shifted upward by 30 to 40 basis points (Figure 2). After the ceasefire, the forecast curve reverted toward its pre-conflict trajectory and tracked the subsequent path of realized US CPI relatively well, confirming that markets priced the shock as transitory once supply pressure eased.

Higher crude prices feed through to transportation, manufacturing inputs, and food production, but conflict also disturbs components not conventionally thought of as energy-linked. Airline fares are a prominent example, responding both through kerosene costs and through the pent-up demand that releases when routes reopen after an airspace closure.

The current episode differs in two important respects. The geographic scope is substantially wider, with simultaneous pressure on Hormuz, the Red Sea, and Gulf LNG infrastructure rather than a more contained exchange. And the macro backdrop has shifted, with tariffs already adding to goods prices and structural gas demand running higher than it was twelve months ago. Even a similar crude price move could produce a larger and more persistent inflation pass-through.

Figure 2

The Strait of Hormuz and What It Means for Energy Costs

Roughly 20 million barrels of oil pass through the Strait of Hormuz each day, approximately a fifth of global petroleum liquids consumption. A sustained impairment cannot be quickly rerouted, and the freight and insurance costs that tanker owners are already building into rates will eventually reach the pump and, from there, the CPI basket.

Recent tanker call data show a meaningful decline relative to recent norms, though the figures do not yet include complete data through March 2, 2026. Kpler tracking data showed that traffic fell roughly 20 to 25 percent within hours of the initial strikes, with the majority of vessels either performing U-turns, idling, or diverting toward alternative routes. By late Saturday UTC, total reductions were approaching 75 percent relative to baseline. We expect tanker transit calls through the Strait of Hormuz to fall considerably in the next few weeks (Figure 3).

Figure 3

![]()

European Gas and the CPI Pass-Through

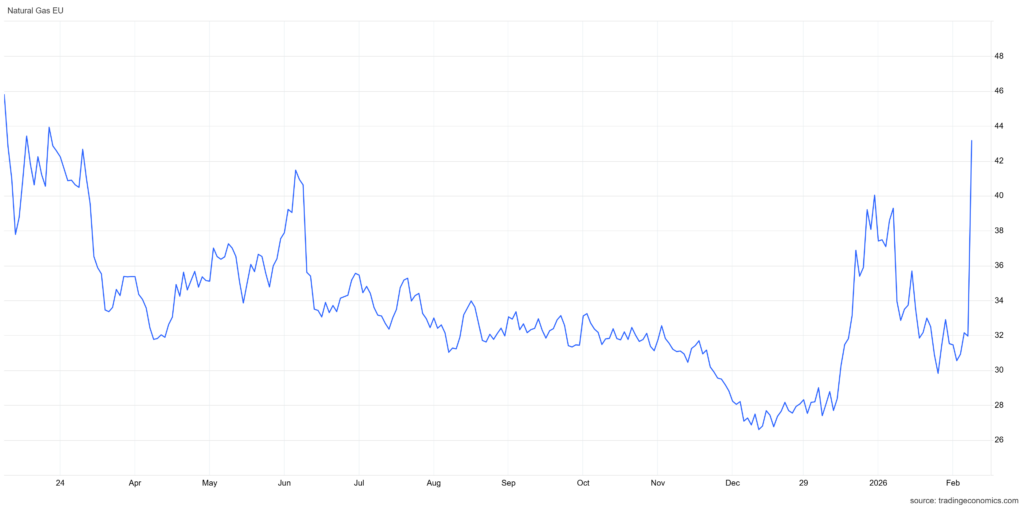

The EU imports approximately 58 percent of its total energy consumption. The post-2022 diversification shifted dependency toward Norwegian pipelines, US LNG, and Qatari LNG. It is that last source now under direct pressure, with QatarEnergy halting all LNG production at its Ras Laffan and Mesaieed facilities after Iranian drone strikes on Monday.

Italy generates roughly 38 to 44 percent of its electricity from natural gas depending on the period measured, making it the most exposed large economy in the bloc to a direct CPI pass-through from higher wholesale gas prices. Germany relies on gas for roughly 15 to 20 percent of its electricity generation with limited storage headroom. Rising structural demand from data centres and the ongoing coal-to-gas transition in Central European power generation make Europe more sensitive to an LNG supply shock in 2026 than it was in 2022, and Turnleaf has flagged both dynamics in previous reporting.

The TTF spike and partial retracement are consistent with repricing while the market waits for confirmation on duration. Even if the supply disruption is ultimately limited, the path through freight, insurance, and procurement competition can still raise costs, complicate inflation prints, and increase volatility in forward power and industrial input pricing. We will continue to monitor movements in natural gas futures and will account for them in our updated forecasts (Figure 4).

Figure 4

Who Gets Hit Hardest

The inflation channel operates through direct household energy costs; industrial input costs across manufacturing and chemicals; transportation and logistics via freight and air routes; and food production, where energy-intensive inputs and distribution costs amplify the pass-through well beyond headline energy prices.

Japan imports approximately 97 to 99 percent of both its oil and natural gas needs, placing it among the most structurally vulnerable large net energy importers to a sustained increase in global energy costs. South Korea faces similar risks. Different denominators: the 20 mb/d figure above is global consumption; the shares below use Persian Gulf departures and destinations. In 2024, 84 percent of crude oil and 83 percent of LNG leaving the Persian Gulf transited the Strait of Hormuz. China, India, Japan, and South Korea accounted for a combined 69 percent of all Hormuz crude flows.

To read the rest, visit our latest Substack post, here.

Research Archive

Macroeconomics Insights – Beyond Tariffs: How Uncertainty is Steering U.S. Inflation Expectations

When we forecast inflation, our goal is to account for as much explainable variation as possible, using available data and reasonable assumptions about how prices evolve....

Macroeconomic Insights: Tariffs, Manufacturing, and Mexico Inflation

This article marks the start of Turnleaf’s series on how U.S. tariffs shape inflation dynamics across Latin America (LATAM). Among the economies we monitor—Colombia, Brazil,...

Macroeconomic Insights: How U.S. Tariffs and Eurozone Weakness Are Shaping Chinese Inflation

The trajectory of Chinese inflation will largely depend on its sensitivity to U.S. tariffs and its ability to sustain domestic GDP growth through external demand, particularly...

Macroeconomic Insights: Prices to Increase in February 2025 as Canada’s Tax Holiday Takes a Holiday

Between mid-December 2024 and mid-February 2025, the Canadian government implemented a GST/HST tax holiday, exempting beverages, restaurants, children’s clothing and footwear,...

Macroeconomic Insights: Fueling the Inflation Fire – Turnleaf’s Turkish Inflation Curve Shifts Upwards

Turnleaf’s latest data has pushed Turkey’s inflation outlook higher than consensus forecasts. There are multiple reasons for this which we will explain in this note. One of the...

Macroeconomic Insights: Assessing the Inflationary Impact of U.S. Steel & Aluminum Tariffs

The newly announced 25% tariff on U.S. steel and aluminum imports introduces cost pressures across global supply chains. However, the key question is not just how markets react,...

Emerging Markets: January 2025 Colombia and Hungary CPI YoY Forecast Review

2025 Colombia CPI YoY Above Consensus Due to Global Inflation Pressures Turnleaf’s CPI YoY model projects Colombia inflation well above consensus 12 months out, as it more...

Emerging Markets: January 2025 India CPI YoY Forecast Review

In our January 2025 YoY CPI forecast, we projected inflation at 4.57%, slightly above the realized 4.3%, yet outperforming consensus (4.71%)—even with our estimate released a...

Macroeconomic Insights: 2025 Eurozone Inflation Outlook – 4 Key Charts to Watch

Turnleaf is forecasting 2–2.5% headline inflation for the Eurozone in 2025, while core inflation is expected to decline through the end of the year towards 2% as momentum in wage...

DeepSeek, objectives and constraints

When a new burger joint opens up, there's often a buzz. Everyone (well, at least me) wants to try the new burger. Is it as good as it looks on Instagram? Or is it just style over...

Hundreds of quant papers from #QuantLinkADay in 2024

I tweet a lot (from @saeedamenfx and at BlueSky at @saeedamenfx.bsky.social)! In amongst, the tweets about burgers, I tweet out a quant paper or link every day under the hashtag...

What we’ve learnt from reading thousands of Fed communications

We recently had the last FOMC decision of 2024. Market l participants reacted to the hawkish tone including Powell’s comments that the Fed’s year-end inflation projection has...

Flash Inflation Outlook: The Cost of Stability, Poland’s Extended Energy Caps

The Polish government’s decision to extend the cap on electricity prices at 500 PLN/MWh is a critical measure to limit inflationary pressures on households. To understand its...

Macroeconomic Insights: A Pinch of Real Rates, a Dash of Slack: Turnleaf’s 2025 U.S. Inflation Recipe

At Turnleaf Analytics, leveraging our machine learning models, we project U.S. inflation to stabilize between 2–3% through 2025, shaped by the interplay of import inflation,...

Macroeconomic Insights: Rising Costs Hit Germany Where It Can’t Afford It—Manufacturing

Germany, long regarded as Europe’s economic powerhouse, owes much of its success to its export-driven industrial base. However, recent years have seen this foundation weaken...