The newly announced 25% tariff on U.S. steel and aluminum imports introduces cost pressures across global supply chains. However, the key question is not just how markets react, but how producers adjust their spending behavior in response to rising cost risks. Turnleaf’s approach focuses on tracking producer sentiment, capital spending decisions, and trade flows to assess the real inflationary impact beyond immediate price fluctuations.

Key Takeaways & Market Implications

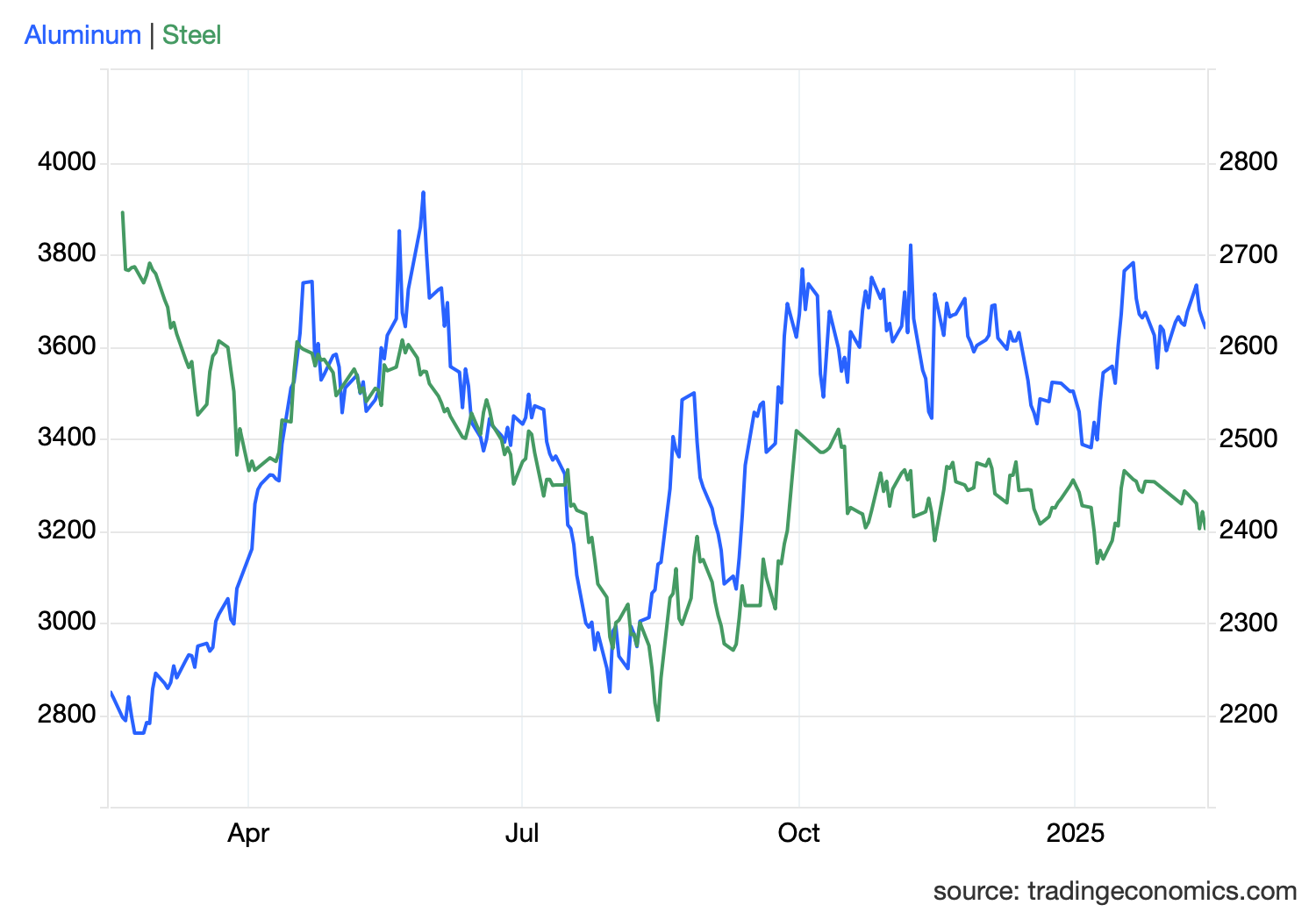

1) Producer Prices & Manufacturing Costs

- Steel and aluminum input costs will rise, but the impact will vary by country based on trade flexibility and supply chain resilience.

- The 2018 steel tariffs led China to reorient supply chains, limiting long-term effects. New tariffs are likely to have a smaller impact on China but a greater impact on aluminum, which is more embedded in U.S. manufacturing, construction, and autos.

- Key Indicator: Aluminum and steel futures prices, as they will reflect how markets expect tariff threats to affect production costs.

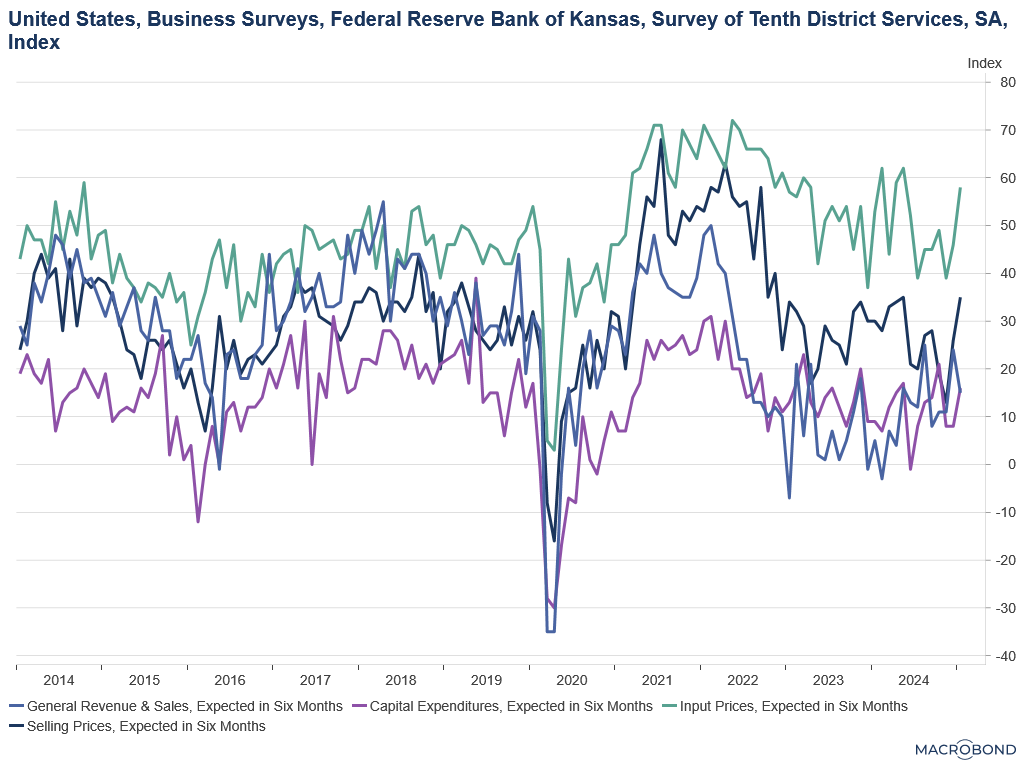

2) Retaliation Risks & Producer Sentiment

- Past tariff disputes led to countermeasures targeting U.S. agriculture and intermediate goods.

- Survey data from the Federal Reserve Bank of Kansas suggests that firms expect input costs to rise but remain uncertain about capital spending. While firms anticipate higher selling prices, revenue expectations are weakening, signaling potential margin compression.

- Key Indicator: February 2025 Kansas Fed Survey, which will reveal whether firms pass costs to consumers or adjust capital investment in response to tariffs.

3) Trade Reorientation & Currency Adjustments

- Export-driven economies like Mexico (manufacturing), Brazil (commodities), and South Korea (electronics) rely on U.S. trade links.

- If these economies redirect exports toward China, it will be critical to monitor currency movements against the Chinese yuan for signs of trade reconfiguration.

- Key Indicator: FX fluctuations in export-driven market currencies like the Mexican Peso, Brazilian Real, and South Korean Won to assess how trade reorientation unfolds.

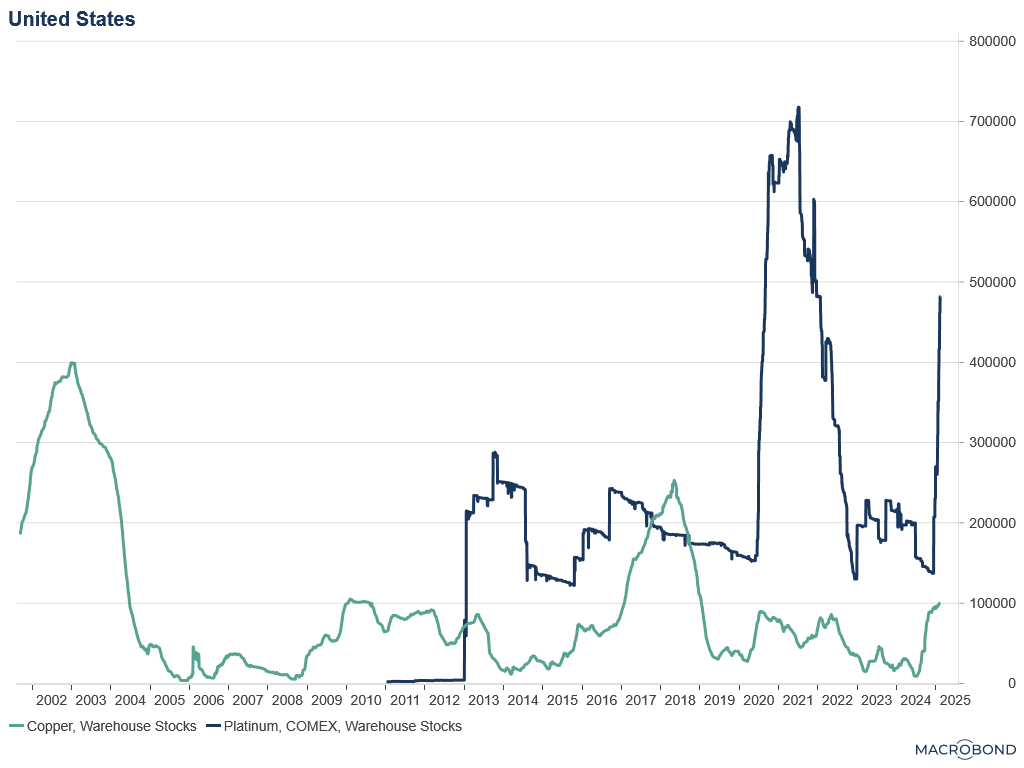

4) Inflation Expectations & Commodity Markets

4) Inflation Expectations & Commodity Markets

- COMEX gold and platinum inventories are rising, not from oversupply but due to increased trading activity and inflation concerns.

- The Fed’s decision to slow rate cuts triggered large inflows into COMEX gold and platinum warehouses. However, platinum’s weaker price response suggests a divergence between monetary policy expectations and industrial demand risks.

- Key Indicator: Gold, platinum, and copper inventory movements, with copper’s recent rally reflecting tariff-related hedging rather than optimism over global growth.

Turnleaf’s Approach: Beyond Market Noise

Turnleaf’s Approach: Beyond Market Noise

Rather than reacting to short-term price swings, Turnleaf focuses on how producers perceive and respond to cost risks. By integrating real-time price data, producer surveys, and capital spending forecasts, our inflation models capture both direct price effects and long-term behavioral shifts.

As global inflation risks intensify, Turnleaf remains committed to delivering forward-looking, data-driven insights that cut through market noise and provide a deeper understanding of economic shifts.