Featured Research

Macroeconomic Insights: FIFA World Cup and Inflation, Where Anything Can Happen

Every time I watch the FIFA World Cup, there's always something that surprises me. I didn't expect Japan to score against Brazil in the first half, nor did I expect Cape Verde to tie with Spain. When about 70,000 people flock to host cities like Kansas City to watch...

Macroeconomic Insights: FIFA World Cup and Inflation, Where Anything Can Happen

Every time I watch the FIFA World Cup, there’s always something that surprises me. I didn’t expect Japan to score against Brazil in the first half, nor did I expect Cape Verde to tie with Spain. When about 70,000 people flock to host cities like Kansas City to watch Algeria play against Austria, demand surges for hotels, airfares, restaurants, and local transport. Prices respond, and, like a World Cup match, the inflation data can throw up surprising results.

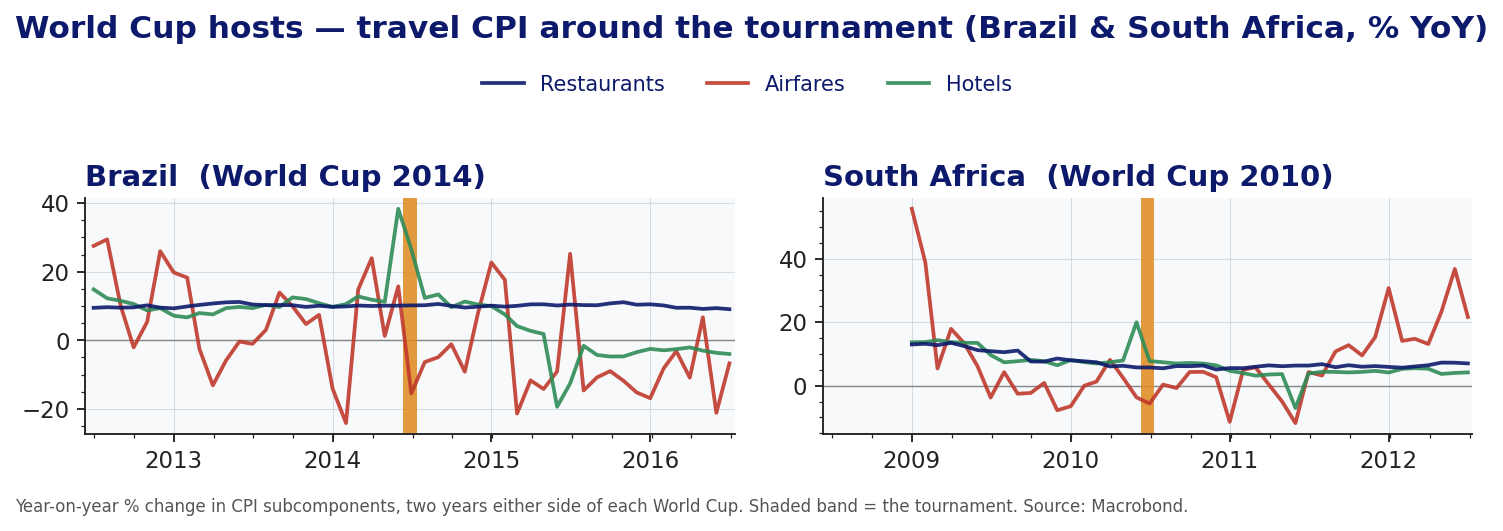

Hosting the FIFA World Cup creates a concentrated demand surge against largely fixed local capacity. Hotel rooms are among the most capacity-constrained prices, so much of the adjustment tends to show up there. To test this pattern, we examine how the relevant CPI subcomponents moved in Brazil and South Africa around the 2014 and 2010 tournaments, respectively.

Figure 1 shows changes in the relevant CPI subcomponents for Brazil and South Africa around the 2014 and 2010 World Cups, respectively. Hotels show the clearest coincident tournament spike before normalising within months. Restaurant inflation is essentially unchanged, while airfare inflation is too volatile to isolate a clean event effect. Hotel inflation rose sharply during the tournament window in both countries, peaking at around 40% YoY in Brazil and around 20% YoY in South Africa before reversing soon after.

Figure 1. YoY change in travel CPI components – hotels, airfares, and restaurants – two years on either side of each World Cup. The shaded band marks the tournament.

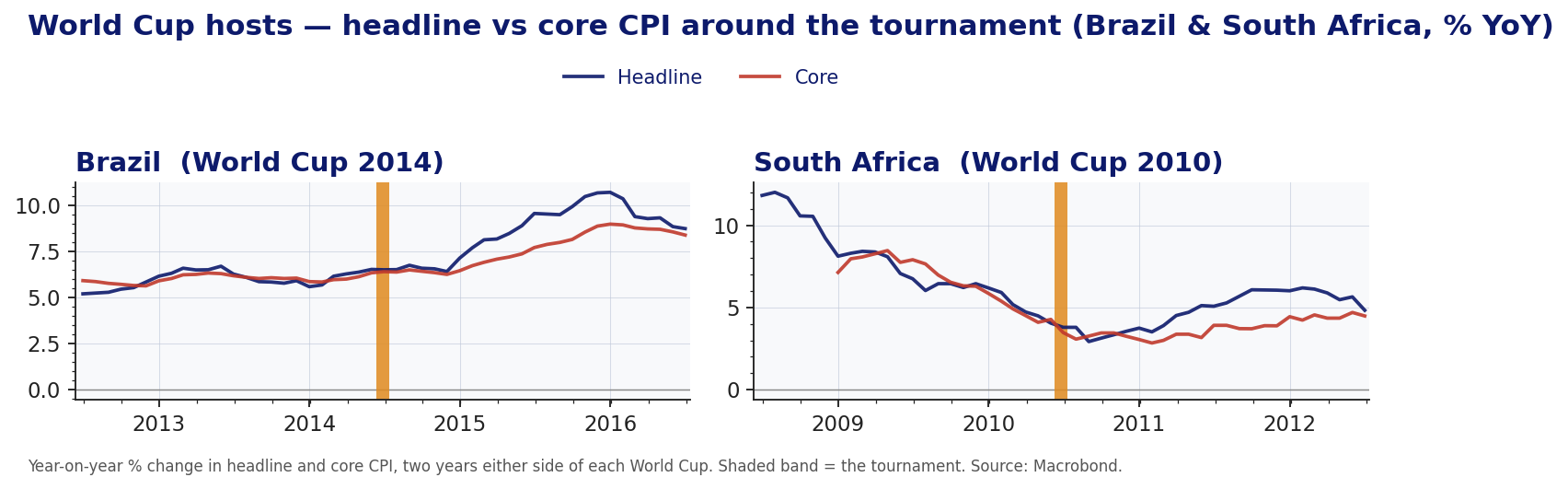

The second stage determines whether the spike reaches the national index. That depends on basket weights. In both economies, airfares and accommodation were small CPI weights, while restaurants were several times larger, so even a sharp hotel spike was small. Headline and core inflation show no discernible tournament break (Figure 2). Brazil held near 6.5% YoY through the window, while South Africa continued a pre-existing disinflation from about 12% YoY toward 4% YoY. Core broadly tracked headline, suggesting no obvious propagation beyond accommodation. The later rise in Brazilian inflation reflected broader macro pressures – including administered prices, depreciation, and recession – rather than the tournament.

Figure 2. YoY change in headline and core CPI, two years on either side of each World Cup. The shaded band marks the tournament.

What we are watching for in 2026

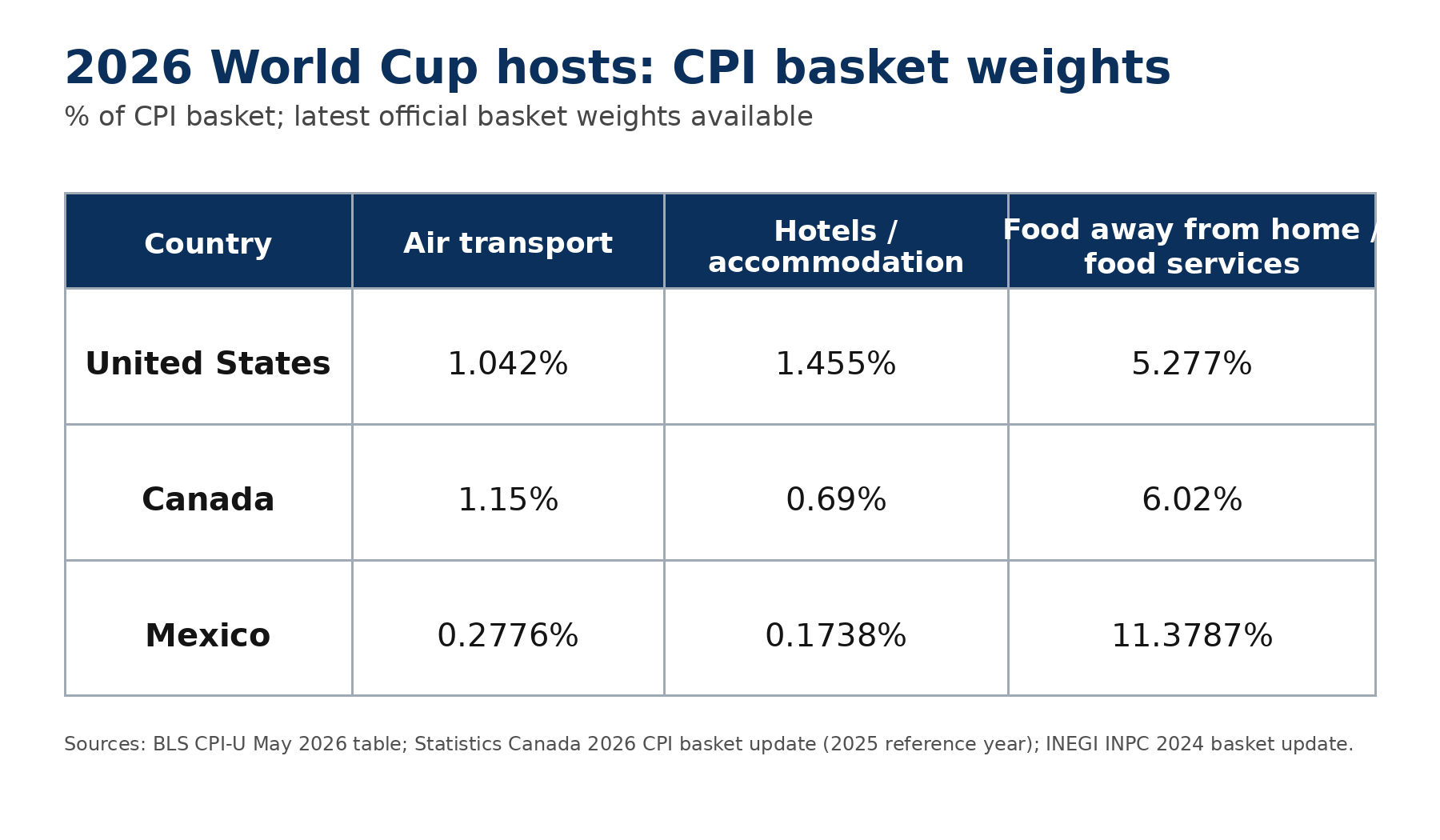

For the 2026 World Cup across the United States, Canada, and Mexico, the base case is a sharp but local rise in service prices with limited and temporary national inflation impact. The scale is bounded by the relevant CPI basket weights: air transport and accommodation are small components in all three hosts, while food services carry a larger weight but are less directly capacity-constrained by the tournament (Figure 3).

Figure 3. Approximate CPI basket weights for selected travel and hospitality components in the 2026 World Cup host countries, percent of national CPI basket.

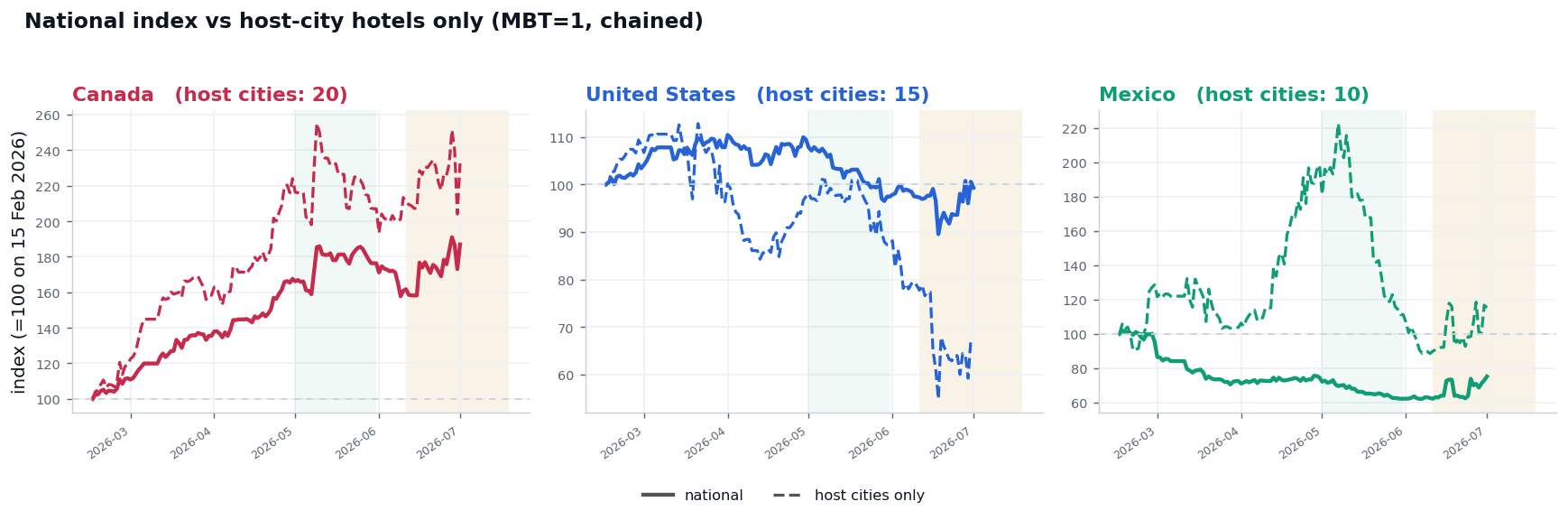

A timely FIFA proxy comes from Turnleaf’s proprietary hotel price index, which tracks daily advertised nightly rates for future stays. Measured one month before travel, host-city rates in Canada and Mexico are running well above their national indexes into the tournament windows – a clear premium of the kind that basket weights then dilute at the national level (Figure 4). In the United States, that premium is absent so far, with advertised host-city rates easing relative to the national index. We read this as early and partial, and expect the host-city premium to build through the June and July match windows before reversing once the crowds leave.

Figure 4. Turnleaf preliminary hotel price index: national versus host-city advertised nightly rates, measured one month before travel and indexed to 15 February 2026. The shaded bands mark the group-stage and knockout windows.

The base case remains a clear local accommodation spike and a limited mark on national 12-month inflation trajectory.

So will inflation surprise us like the last few matches? With Turnleaf’s access to extensive high-frequency and alternative data, that risk is more measurable – and less likely to catch us off guard.

Research Archive

Macroeconomic Insights: Romania CPI Runs Hot

The recent surprise increase in electricity prices in Romania has pushed inflation close to 8%YoY. As Romania begins to rollback inflation fighting policies in the next couple of...

Macroeconomic Insights: U.S. CPI, Evaluating the Impact of Tariffs at Home and Abroad

When evaluating the impact of tariffs on consumer prices, we consider how they affect prices both domestically and abroad. Key factors include the effective tariff rate, the...

Macroeconomic Insights: Switzerland CPI – Just How Much Will Tariffs Hurt Switzerland?

Last week, President Trump threatened to impose a 39% tariff on Switzerland, higher than the initial 31% discussed in April 2025. With the U.S. being a major importer of Swiss...

Macroeconomic Insights: Eurozone CPI – Inflation Running Hotter Than Expected

The Eurozone Grew More Than Expected – Germany & Italy Overall, the Eurozone has enjoyed 0.6%QoQ growth in 2025Q1 despite disinflationary forces like weaker consumer and...

Macroeconomic Insights: Israel CPI – Air Travel Expected to Bump Up August Print

On August 3, 2025, Ben Gurion Airport will resume over 120 international flights for the month, though this remains insufficient to fully meet demand. Israeli travel companies...

Macroeconomics Insights: Europeans Can Finally Buy An Apocalypse Hellfire at 0% Tariff

Recently Trump announced a trade deal with the EU with terms that impose a 15% tariff on all E.U. imports (including motor vehicles) and a 0% retaliatory tariff on the U.S....

Macroeconomic Insights: U.S. Core CPI – Who’s Paying for the Tariffs?

In the first five months of 2025, the U.S. government collected $68.9 billion in tariffs and excise taxes, as the Yale Budget Lab reports the effective tariff rate surged from...

Macroeconomics Insights: Navigating Inflation and Deflation – China and Japan

As we approach the second half of 2025, the inflation trajectories of China and Japan reflect contrasting dynamics shaped by domestic economic conditions, external influences,...

Run to Research

Left foot forward, right foot forward, puncturing the mud, plodding along, the wind in winter, the sun in summer, in the trees’ shadows, patterns of light and dark along the...

Macroeconomic Insights: Ea-Nasir’s Fine Quality Copper Hit with 50% Tariffs in August

Since the inauguration of President Trump, uncertainty has significantly influenced inflation dynamics, primarily through unpredictable tariff policies. However, firms are now...

Macroeconomic Insights: United States CPI – Firms are Still Front-Loading

To date, uncertainty has been the defining feature of the inflation story. Volatile trade policy has deterred many firms from making strategic investments, slowing business...

Macroeconomic Insights: FX, Oil, Copper, and Tariff Risks in Emerging Markets

Across Colombia, Chile, Brazil, and China, inflation dynamics are currently shaped by common external themes: exchange rate movements, global commodity prices—particularly...

Twenty years in financial markets

Time is a curious thing. We say time passes, yet rather than simply pass, time tends to dissolve. Once gone, it dissolves leaving an imprint behind. At times, it's a clear...

Macroeconomic Insights: Czech Republic CPI – House Prices on the Rise

Recently, housing prices in the Czech Republic have increasingly exerted upward pressure on inflation. Our June 2025 Forecast Word Cloud highlights the primary drivers...

Macroeconomic Insights: Malaysia CPI – Electricity Tariff Reform from July 2025

Malaysia has changed its electricity tariff schedule, and allegedly, it should save the average consumer up to 19% on their bills. However, after an announcement in June 2025,...