Featured Research

Macroeconomic Insights: UK Policy Package and the Underlying Inflation Picture

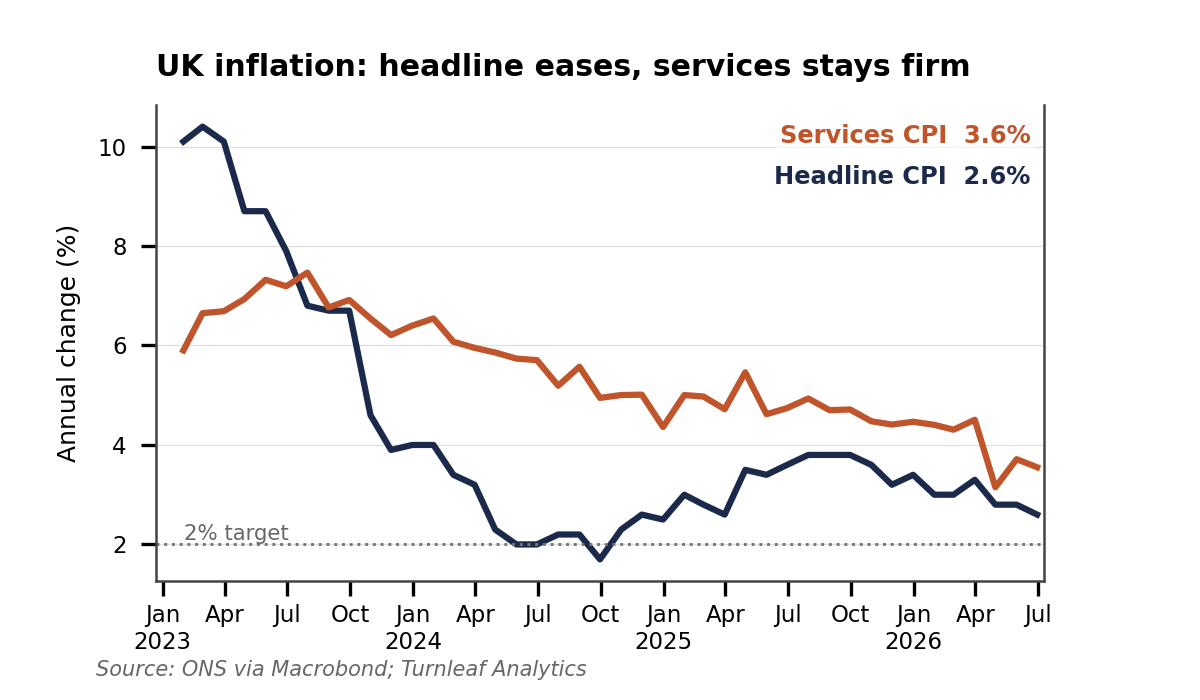

UK CPI printed at 2.6% YoY in June 2026, but the composition of that print sits uncomfortably against a broader policy package now working its way through the price level. Services inflation ran at 3.6% in the same month, a full percentage point above the headline...

Macroeconomic Insights: UK Policy Package and the Underlying Inflation Picture

UK CPI printed at 2.6% YoY in June 2026, but the composition of that print sits uncomfortably against a broader policy package now working its way through the price level. Services inflation ran at 3.6% in the same month, a full percentage point above the headline rate, and that gap is the more informative number for the year ahead. The new government has announced three near-term cost-of-living measures. VAT will be removed from domestic electricity from October 2026, the bus-fare cap in England will fall to £2 from January 2027, and business rates in England will be cut by an additional 20% for eligible pubs, social clubs and live music venues from April 2027, on top of the 15% relief already in place for 2026/27 and with the largest live music venues excluded.

The first two measures act directly on measured CPI, alongside the freeze in regulated rail fares. The business-rates reduction does not, and we treat it in the same category as employment rights, immigration and planning, namely as a potential indirect influence on prices. All of it sits alongside deeper reforms across energy, fuel duty, wages and rented housing. Our reading is that the direct interventions are likely to be visibly disinflationary for measured CPI from late 2026, while the underlying picture is more mixed.

Services inflation remains sticky. Annual producer-price inflation also remains elevated, particularly in services, although monthly manufacturing-cost momentum softened in June, with input prices down 2.0% and output prices flat. The growing role of administered pricing means that simple read-through from wage growth or wholesale energy to CPI is no longer sufficient (Figure 1). Our 12-month forecast curve is currently tracking a widening gap between headline CPI shaped by policy dates and underlying inflation shaped by wages, margins, demand and capacity.

Figure 1. UK inflation, headline eases while services stays firm

Direct CPI effects

The clearest intervention is the removal of VAT from domestic electricity. Electricity accounts for roughly 2% of the CPI basket, and removing the 5% VAT rate could reduce the overall CPI price level by just under 0.1 percentage point under full pass-through. That is a one-off move in the price level which holds down the 12-month rate for roughly a year from October 2026 and then drops out of the annual comparison.

The measure follows a 13% increase in the typical dual-fuel price cap in July, although that increase was driven mainly by gas. Ofgem reports that electricity bills rose by around 5% and gas bills by around 24%, with the electricity unit rate moving from 24.67p to 26.11p per kWh. Removing VAT would lower VAT-inclusive electricity prices by approximately 4.8%, offsetting most of the July increase in the electricity component while leaving household gas prices untouched.

The same principle applies to transport. Regulated rail fares have been frozen, while the bus-fare cap will fall from £3 to £2 in January 2027. Both measures are disinflationary but their model contribution depends on the share of fares actually covered.

Fuel duty moves in the opposite direction, but later than previously planned. The temporary 5p-per-litre reduction has been extended until 31 December 2026. Under the current schedule, duty rates will begin returning towards their pre-March 2022 levels in January 2027, with a further increase in March, although final rates remain subject to confirmation at Budget 2026. The upward pressure on petrol and diesel prices therefore sits in 2027, and the size of the effect will depend on oil prices, refining margins and retailer pass-through. Our model treats each fare and duty change as an independent policy adjustment.

Labour

Labour reforms sit in the same category. The National Living Wage rose to £12.71 in April 2026, and new employment protections are being phased in across 2026 and 2027. These measures raise labour and compliance costs, particularly in hospitality, retail, care, cleaning and logistics. The inflation effect depends on whether firms absorb the increase through margins, improve productivity, reduce staffing, or pass costs into prices. Aggregate wage growth alone does not capture this, and regular pay growth has continued to ease even as services inflation has held near 3.6% (Figure 2). We track the wage-floor pass-through through the Average Weekly Earnings total-pay series on a three-month annual growth basis, and combine it with the Total Job Vacancies stock, the Online Job Adverts All Industries flow and the Labour Market Output Net Employment Balance to gauge the direction of sector-level pricing power. The Bank of England Realised and Expected Wage Growth series then anchor the forward path against firms’ own reported behaviour.

Figure 2

To read the rest of this article, please visit our latest Substack post, here.

Research Archive

Macroeconomic Insights: Australia Inflation Sparks Concern

Reaching 3.8% YoY in October 2025, headline CPI is currently above both the RBA's 2–3% target band and the market consensus forecast of 3.6% (ABS CPI October 2025). Turnleaf's...

Macroeconomic Insights: India CPI – Structural Pressures Emerge

In the past month Turnleaf's 12-month inflation forecast for India has edged lower as the pace of food and energy price increases slowed. This moderation reflects seasonal...

QuantMinds London 2025

"Are you on mute?" is perhaps the most succinct catchphrase which most comprehensively describes the post-covid landscape of work. Yet, despite the plethora of video conferencing...

Macroeconomic Insights: Gilt Selloff, Autumn 2026 Budget

The Autumn 2025 Budget, scheduled for 26 November, is expected to deliver substantial fiscal tightening. Independent forecasts estimate a tax-raising package in the region of...

Macroeconomic Insights: US CPI — Shutdown Distortions Shift the Focus to November

The 43-day U.S. government shutdown has materially degraded the quality of October’s inflation data. With BLS field operations suspended for the duration of the collection...

What would you have said?

I recently went back to Imperial College. Whilst, I've been back many times since I graduated, this was the first time that I was returning to stand in front of an audience to...

Macroeconomic Insights: Norway CPI – Hey It’s Okay, Mistakes Happen

The Norway Statistical Institute recently revised the latest CPI print from 3.3% to 3.1%, correcting an error in electricity-price calculations that overstated inflation. Despite...

Macroeconomic Insights: Abu Dhabi GDP Forecast

Turnleaf expects Abu Dhabi GDP growth to slow to 2-3%YoY in the next two quarters before hitting 7%YoY in 2026Q1 and then falling back to a bit over 3%YoY by June 2026 (Figure...

Macroeconomic Insights: Switzerland CPI – Escaping Deflation

Turnleaf expects Switzerland inflation to oscillate around 0% over the next 12 months with some indication of healthy price growth towards the tail-end of our forecast (Figure 1...

Macroeconomic Insights: Japan CPI – Nigiri Sushi Inflation

As of September 2025, Japan's inflation profile remains dominated by food price dynamics. The headline 2.9% YoY reading reflects a disproportionate rice contribution—despite...

U.S. Government Shutdown and the October 2025 CPI Print

The BLS released the September 2025 CPI print on October 24, nine days after its originally scheduled October 15 release date, following a partial recall of staff during the...

Quant Strats London 2025

Quant Strats has been a feature of the quant calendar for a number of years. I went to my first event recently after a couple of years. The event has evolved somewhat over time,...

Macroeconomic Insights: Brazil CPI — Food Costs, Currency Dynamics, and the Path to 4%

Brazilian inflation has proved particularly sticky, driven by persistent wage growth, global trade dynamics, and elevated food inflation from weather-related supply constraints....

Macroeconomic Insights: UK September 2025 CPI Analysis

UK CPI for September 2025 declined to 3.8% YoY, falling below market expectations of 4.0% (vs. Turnleaf estimate of 3.94%). The decline was primarily driven by sustained lower...

Macroeconomic Insights: Japan CPI – Subsidies Reset

Japan’s CPI over the next two months will be shaped by a mix of expiring and newly introduced subsidies. Over the past two years, national electricity and gas subsidies have...