Featured Research

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a...

Macroeconomic Insights: Mexico CPI Divergence and the IEPS Fuel Stimulus, July 2026

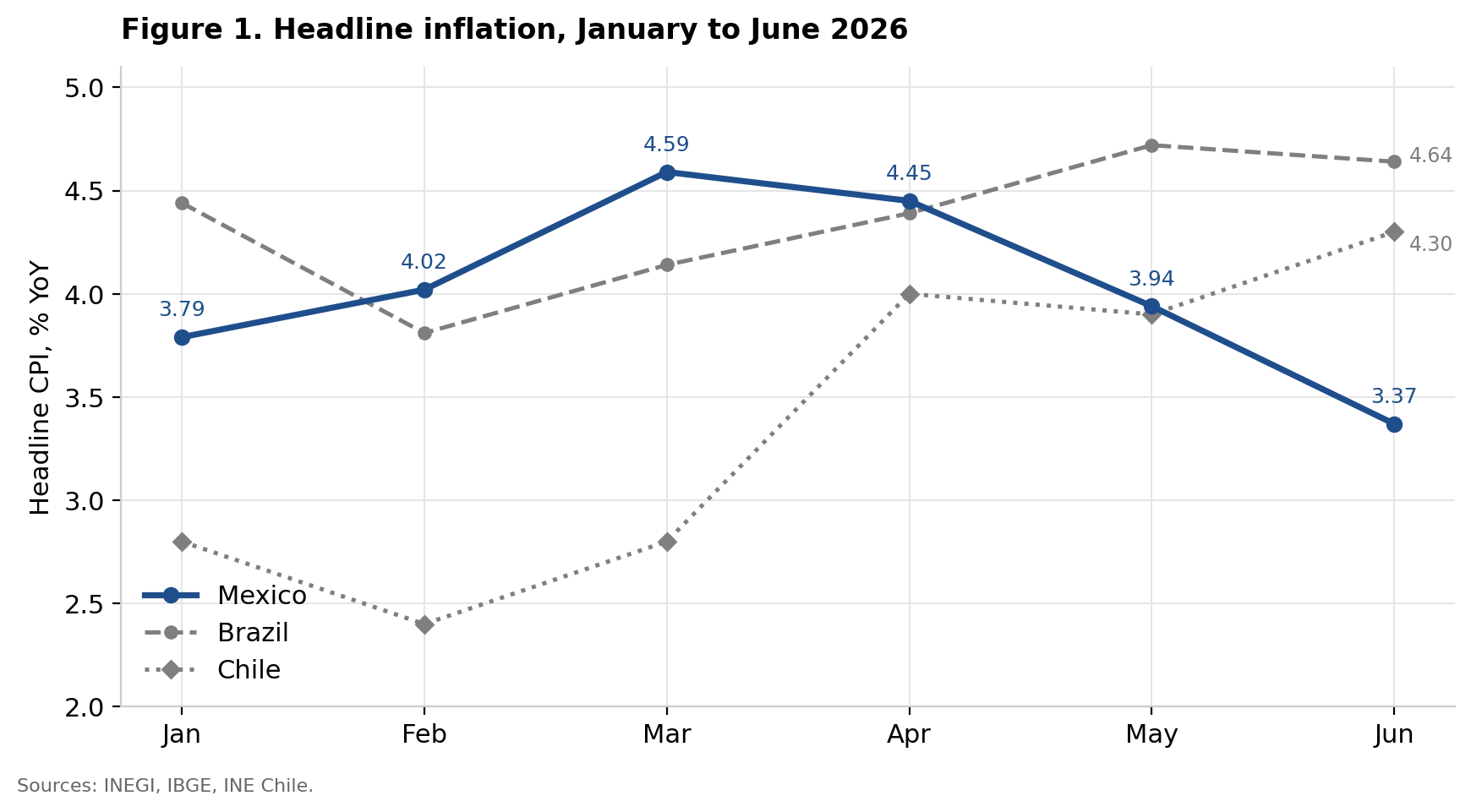

Since early March, the US-Iran conflict has disrupted Gulf oil supply, closing the Strait of Hormuz to commercial traffic and taking Brent crude from roughly USD 70 in January to above USD 100 in April. A ceasefire returned prices to pre-war levels in June before a second escalation in July pushed Brent back towards USD 97, a rise of nearly 40% on the month. For Latin America’s oil importers this amounts to a substantial imported inflation shock. Chilean inflation has climbed from a five-year low of 2.4% in February to 4.3% in June, its highest since September 2025, while Brazilian inflation stood at 4.64% in June with energy and fuel inflation running at 7.71%.

Mexico has moved in the opposite direction, with headline inflation falling to 3.37% YoY in June from 3.94% in May despite having entered the shock with the highest rate of the three economies, peaking at 4.59% in March. Mexico has largely absorbed the oil shock through weekly adjustments to fuel subsidies and administered price agreements, while underlying core inflation has remained broadly stable.

A Common Shock, Three Outcomes

Central banks and statistical agencies in Chile and Brazil have linked the recent rise in inflation to the energy and production-cost effects of the Middle East conflict. Banco Central de Chile notes that inflation excluding food and energy remains close to its 3% target, while Brazil’s statistical agency, IBGE, attributes higher energy and fuel inflation to the closure of the Strait of Hormuz. Differences in monetary policy do not fully explain Mexico’s divergence from these peers. Banco de México held its policy rate at 7% in February, cut it to 6.75%, and ended its easing cycle in May. Despite this less restrictive stance relative to Brazil, Mexican headline inflation has continued to fall while inflation in Chile and Brazil has risen.

Where the Recent Disinflation Sits

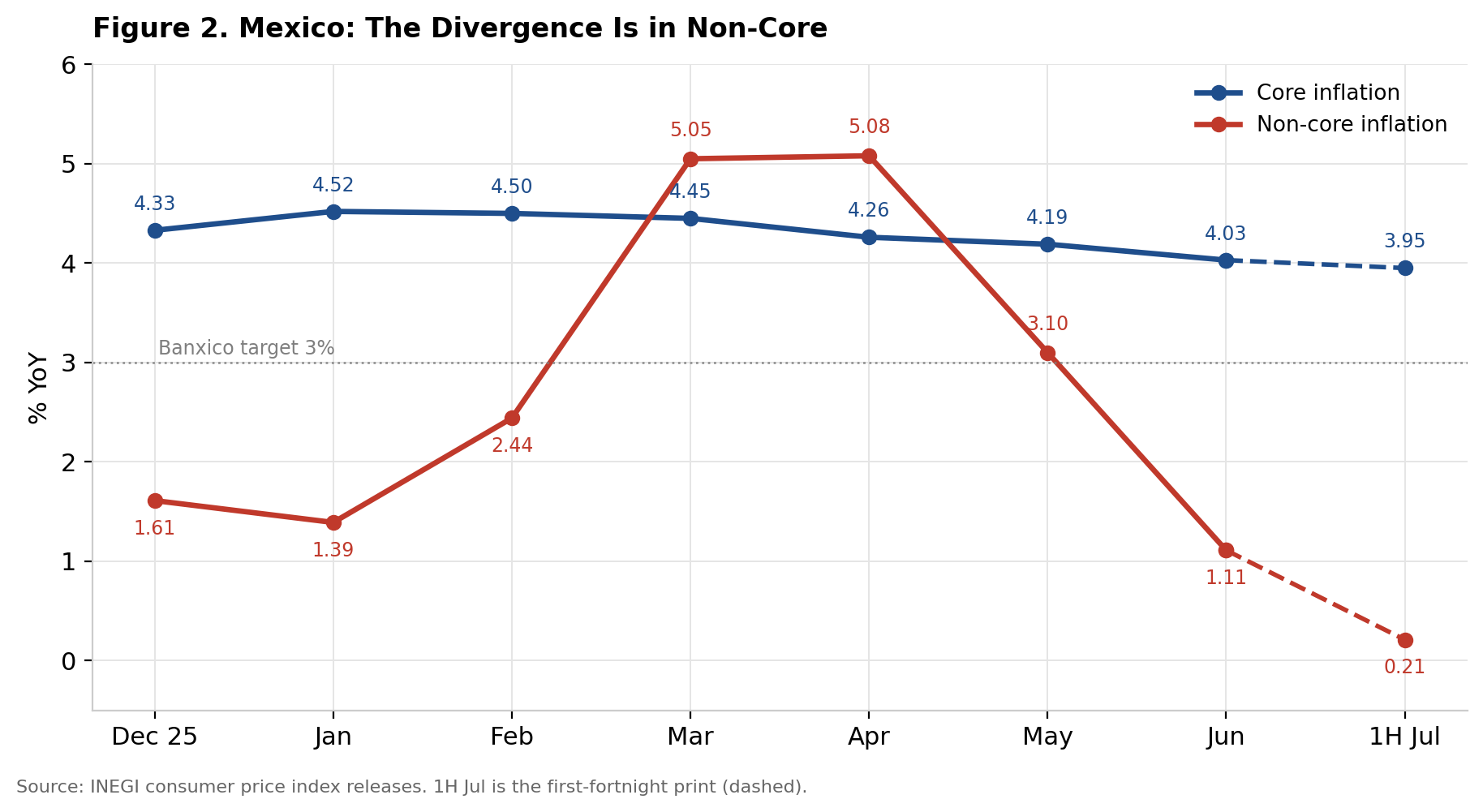

The composition of Mexico’s June inflation print shows that the divergence is concentrated in non-core components. Core inflation stood at 4.03%YoY, compared with just 1.11% for non-core inflation. While core inflation has eased only gradually from 4.52% in January, non-core inflation has fallen sharply from 5.08% in April to close to 1% in June. Fruit and vegetable prices declined 8.99%MoM as crop conditions normalised and government agreements with producers took effect. At the same time, energy prices and government-authorised tariffs rose by only 0.08% despite the oil shock, following a 1.67% decline in May driven by seasonal electricity tariff reductions. Mexico’s headline disinflation has therefore not come from a broad easing in underlying price pressures. It has been driven mainly by volatile and administered components, particularly food, energy and regulated tariffs.

A Weekly Excise Subsidy

The main instrument absorbing the shock is the fiscal stimulus applied to the Special Tax on Production and Services, or IEPS, on motor fuels. Under this mechanism, the Secretaría de Hacienda y Crédito Público publishes a weekly agreement in the Diario Oficial de la Federación specifying the share of the fixed per-liter excise tax absorbed by the federal government. The measure functions as a contingent shock-absorption tool rather than a permanent subsidy. It was withdrawn on April 12, 2025, and remained at zero for 48 consecutive weeks through nearly a year of normal price fluctuations. It was reinstated on March 13, 2026, within days of the closure of the Strait of Hormuz, and has since been adjusted weekly in response to movements in international crude prices. Because the comparison period contained no subsidy, each YoY reading from March onward compares subsidized fuel prices with an unsubsidized base. The resulting downward wedge in fuel inflation will therefore persist for as long as the stimulus remains in place.

Sizing the Wedge

To read the rest of this analysis, visit our latest Substack post, here.

Research Archive

Neudata London March 2026

A decade ago, I liked burgers, and a decade on, well, I still like burgers. However, one thing that has changed greatly has been the alternative data market. What was once an...

Macroeconomic Insights: Spain CPI Downside Surprise and Energy Tax Cuts

Spain headline CPI YoY jumped sharply to 3.3% YoY in March 2026 from 2.3% in February entirely on the back of energy price reversals linked to the Iran conflict and Strait of...

Macroeconomic Insights: Asia-Pacific Tries to Contain the Oil Shock

Across the Asia-Pacific, policymakers are throwing subsidies, tax cuts, reserve releases, and pricing controls at rising fuel costs in an attempt to delay or smooth an external...

It’s five to eleven

Whenever I travel somewhere, I like to read books about the place I'm visiting. It helps in way to provide some context for me. Over the years I've been to Portugal many times,...

Macroeconomic Insights: LATAM Fights an Oil Shock

In an earlier post, we explored the lagged correlations between Brent crude oil price changes and CPI (Figure 1). Here, we see that for many LATAM countries pass-through is...

Macroeconomic Insights: Airfares Take Off as Iran Conflict Continues

The war in Iran has persisted far longer than anticipated, driving sustained increases in global commodity prices. These pressures are now filtering into downstream products...

Macroeconomics Insights: Oil Prices Up, Will Food Prices Follow?

Over the past three weeks, the escalation of conflict in the Middle East has coincided with a clear increase in Brent crude prices, reinforcing the expectation of near-term...

Macroeconomic Insights: Iran’s Oil Shock Fuels Inflation

It’s been more than 2 weeks since the US-Israel joint combat mission against Iran began and the conflict doesn’t look like its going to end any time soon. Iran is doing...

Macroeconomic Insights: Energy Price Pass-Through to Inflation

Brent crude has surged from ~$70 to above $100 following the US-Israeli strikes on Iran and the near-closure of the Strait of Hormuz (Figure 1). Dutch TTF natural gas has jumped...

Macroeconomic Insights: Strait of Hormuz and the Inflation Shock Markets Are Repricing

The US-Israel strike on Iran has pushed Middle East risk back to the center of global pricing. Crude has firmed into the low 70s while European gas prices spiked, and gold has...

Macroeconomic Insights: Trump’s Tariff War – The Sequel

On Feb 20, 2026, the Supreme Court ruled 6–3 (Learning Resources, Inc. v. Trump) that the International Emergency Economic Powers Act (IEEPA) does not authorize the U.S....

Macroeconomic Insights: Gold’s New Inflation Playbook

Gold has stopped trading as a clean derivative of US real yields and now reflects a broader external pricing regime. Since 2022, the real-yield anchor has weakened, gold has...

TradeTech FX USA 2026

Over recent years, the finance community in Miami has grown, given that a number of hedge funds have opened up large offices there. Every February, the FX community from New...

Macroeconomic Insights: India CPI – Basket Reweighting Explained

India's National Statistical Office launched a new Consumer Price Index series on February 12, 2026, shifting the base year from 2012 to 2024 and overhauling the basket...

Macroeconomic Insights: UK CPI — Assessing the Renters’ Rights Act 2025

Executive Summary The Renters' Rights Act received Royal Assent on 27 October 2025. Council investigatory powers commenced on 27 December 2025, and the main rent-setting...