Featured Research

Macroeconomic Insights: Trump’s Tariff War – The Sequel

On Feb 20, 2026, the Supreme Court ruled 6–3 (Learning Resources, Inc. v. Trump) that the International Emergency Economic Powers Act (IEEPA) does not authorize the U.S. President to impose tariffs, a power the Constitution assigns to Congress. Between our Feb 20,...

Macroeconomic Insights: Trump’s Tariff War – The Sequel

On Feb 20, 2026, the Supreme Court ruled 6–3 (Learning Resources, Inc. v. Trump) that the International Emergency Economic Powers Act (IEEPA) does not authorize the U.S. President to impose tariffs, a power the Constitution assigns to Congress. Between our Feb 20, 2026 nowcast for the US and our Feb 23, 2026 nowcast, we see a moderate increase at the tail of the 12-month forecast curve (Figure 1).

Figure 1 – visit our Substack to see the latest forecast, here

Within hours of the ruling, Trump signed a proclamation invoking Section 122 of the Trade Act of 1974, a statute never previously used for tariffs, imposing a 10% global surcharge effective today, February 24, 2026. On February 21, Trump announced via Truth Social his intention to raise this to the statutory ceiling of 15%, though no formal proclamation had been issued as of the time of writing (White House Fact Sheet). Unlike IEEPA, Section 122 tariffs are capped at 15% and expire after 150 days (July 24, 2026) unless Congress votes to extend them. Markets are treating the 15% as the operative rate pending CBP enforcement guidance, and our table below reflects that assumption. Given the administration’s prior use of multiple statutory pathways, further action under Sections 232 or 301 remains a high-probability scenario once the 150-day window expires.

Refunds as Fiscal Offset

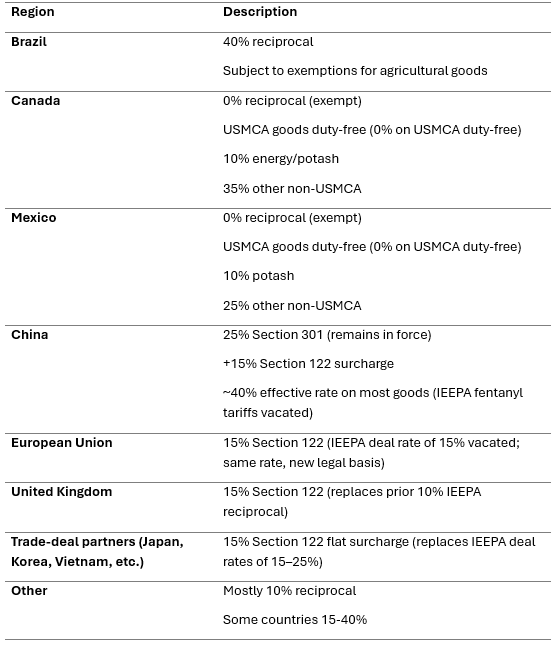

Other countries who have already made deals with Trump are likely to resist any global tariff that exceeds their established amounts. As the table below illustrates, several partners (EU, UK, trade-deal countries) now face a higher effective rate under the flat 15% Section 122 surcharge than under their prior IEEPA deals, while others (notably China) see a net reduction as the stacked IEEPA fentanyl tariffs are vacated. IEEPA refunds also pose a significant fiscal challenge (Figure 2).

Figure 2: Current Tariff Policy as of February 18, 2026 (Source: Yale Budget Lab; Global Trade Alert) – Broad Tariffs under IEEPA Authority (REPEALED)

U.S. Customs and Border Protection collected approximately $133–$142 billion in IEEPA duties through year-end 2025, with the Penn Wharton Budget Model projecting up to $175 billion in total refund liability. These refunds flow to importers rather than consumers, functioning as a form of backdoor fiscal stimulus that partially offsets the inflationary drag from remaining tariffs, though the timing is highly uncertain, with TD Securities estimating a 12–18 month disbursement window. On net, the Yale Budget Lab estimates a short-run consumer price increase of ~0.6% under full pass-through, roughly $600–$800 per household, approximately half the impact had IEEPA tariffs remained in force. This is consistent with our view that the inflation impulse from the tariff transition will be modest and gradual, concentrated in metals, electronics, and motor vehicles where Section 232 tariffs continue to bite.

Implications for Inflation and the Fed

The temporary and legally constrained nature of Section 122 tariffs reduces the risk of a sustained inflation shock, allowing monetary policy to remain focused on underlying disinflation trends. Chairman Powell’s last day is set to be May 15, 2026, when he is replaced by Kevin Warsh, a former Fed Governor (2006–2011) nominated by Trump on January 30, 2026, who is expected to cut interest rates at a faster pace than his predecessor. Though interest rates remain on hold for now, markets are pricing in 2–3 cuts in 2026 under the Warsh-led Fed, a trajectory that, if realized, would provide some offset to any tariff-driven cost pressures visible in H2 CPI prints.

The table above shows that the shift to a flat 15% Section 122 surcharge produces mixed outcomes across partners. The effective tariff rate rises to approximately 13.7% (Yale Budget Lab, Feb. 21, 2026, a moderate increase from the initial 10% rate but well below the pre-SCOTUS level of 16.0%. Firms largely absorbed import costs through 2025 pending legal clarity, delaying pass-through to consumer prices. Any residual price pressures are likely to emerge gradually over the next few months, with delays possible depending on how Congress acts at the 150-day mark. We will continue to monitor high-frequency port data, PMI import price subcomponents, and survey data to gauge upside risk on inflation.

What’s Next?

The tariff transition does not materially change the macro outlook. The SCOTUS ruling removes tail risk from an uncapped IEEPA regime, while the Section 122 replacement is time-limited, legally constrained, and partially offset by the fiscal stimulus of IEEPA refunds. The inflation impulse remains modest and manageable. The more consequential variable is whether Congress extends Section 122 past July 24 or the administration deploys Sections 232 and 301 at scale, either of which would warrant an upward revision to our CPI forecasts.

Research Archive

Macroeconomic Insights: France’s Inflation Outlook Amid Fiscal and Economic Pressures

France’s inflation remains near the European Central Bank’s (ECB) 2% target despite significant fiscal spending during the pandemic and in response to the war in Ukraine....

Flash Inflation Outlook: South Korea Inflation Amid Political Instability

South Korea’s brief declaration and subsequent revocation of martial law by President Yoon has damaged investor confidence, further weakening the won and placing pressure on the...

November 2024 Global Inflation Call: Transcript

Global Inflation Amid Trade Uncertainties Good afternoon and welcome to Turnleaf’s global inflation call. For the past month, global inflation expectations have been shaped by...

Takeaways from QuantMinds 2024 in London

Over the past years, the quant industry has changed substantially. My first visit to Global Derivatives was just over a decade ago. At the time, perhaps unsurprisingly, the...

Macroeconomic Insights – Poland’s Fight with External and Domestic Demand

As Poland navigates a complex economic landscape, its rapid growth, fueled by competitive wages and strong manufacturing, faces challenges from both domestic and external...

Takeaways from Web Summit 2024

Think of Lisbon and no doubt it’ll conjure images of explorers setting sail in centuries past across the ocean, the hills that climb across the city, pastel de nata and salted...

Macroeconomic Insights: UK Autumn 2024 Budget and Global Trade Pressures Add to Inflation Challenges

The UK government's Autumn Budget for 2024, introduced on October 30, is designed to enhance public services through increased capital investments, funded by higher taxes along...

Macroeconomic Insights: U.S. Inflation Outlook Under Another Trump Presidency

As U.S. economic conditions continue to evolve, Turnleaf will actively monitor inflation trends and publish regular updates to keep you informed. Our focus remains on leading...

Macroeconomic Insights: Turkey’s Two-Front Fight with Inflation and the Lira

Turkey’s central bank has adopted a stringent monetary policy to combat inflation, a stark departure from previous unorthodox strategies. With borrowing costs now at a benchmark...

Inflation Outlook for Canada in October 2024- Producer Optimism, Consumer Pains

Canada’s inflation outlook is shaped by a complex mix of declining energy costs, rising food prices, and evolving trade dynamics. At Turnleaf Analytics, we’re closely tracking...

How Bad is Too Bad? Japan’s Reckoning with Inflation and New Leadership

Japan’s battle with inflation has become a key issue, reshaping public sentiment and influencing recent election results. With the Liberal Democratic Party (LDP)–Komeito...

Turnleaf’s Inflation Outlook for Brazil: Rising Costs Amid Currency Pressures

Turnleaf’s Brazil’ inflation outlook for the next 12 months has undergone an upward revision, driven by several significant factors. While shipping costs have eased, inflationary...

Turnleaf’s October 2024 Economic Forecast: Deflationary Pressures Persist in China

Turnleaf Analytics’ forecast for YoY NSA CPI published in October 2024 suggests an inflation trajectory expected to remain well below 2% over the coming 12 months. Specifically,...

FILS Europe 2024 Takeaways

Paris is home to many things, the Eiffel Tower, the Arc de Triomphe, burgers (ok, I made that one up!). In recent years, Paris' financial community has grown, and indeed, every...

Don’t look back in hanger steak

I'm currently in the queue for Oasis tickets. Rather than mindlessly watching the counter of people in the queue ahead of me fall (currently 184,984 people), I thought I'd start...