Featured Research

Macroeconomic Insights: El Niño and the Inflation Outlook for the Year Ahead

A developing El Niño is becoming an important force in the inflation outlook over the next year. By shifting global rainfall patterns, it can bring drought to some regions and heavy rain to others, with the greatest economic impact often felt through food production....

Macroeconomic Insights: El Niño and the Inflation Outlook for the Year Ahead

A developing El Niño is becoming an important force in the inflation outlook over the next year. By shifting global rainfall patterns, it can bring drought to some regions and heavy rain to others, with the greatest economic impact often felt through food production. The Niño 3.4 sea-surface temperature anomaly has already crossed the El Niño threshold and is expected to strengthen further around the turn of the year.

The effects are likely to fall most heavily on emerging markets, especially those that are major agricultural producers, though the impact will vary by region. Drought across Southeast Asia, Australia and parts of India threatens crops such as rice, wheat, sugar, palm oil, coffee and cocoa. In South America, the picture is more mixed. El Niño can hurt coffee-growing regions in Colombia and northern Brazil, while bringing potentially beneficial rains to the grain belts of Argentina and southern Brazil.

Markets tend to price these risks quickly, often before actual crop shortfalls appear, but the pass-through to retail food prices is slower, typically taking six to sixteen months. The inflation impact is therefore likely to emerge with a lag, building through the year ahead and falling most heavily on food-sensitive emerging markets.

What previous episodes show

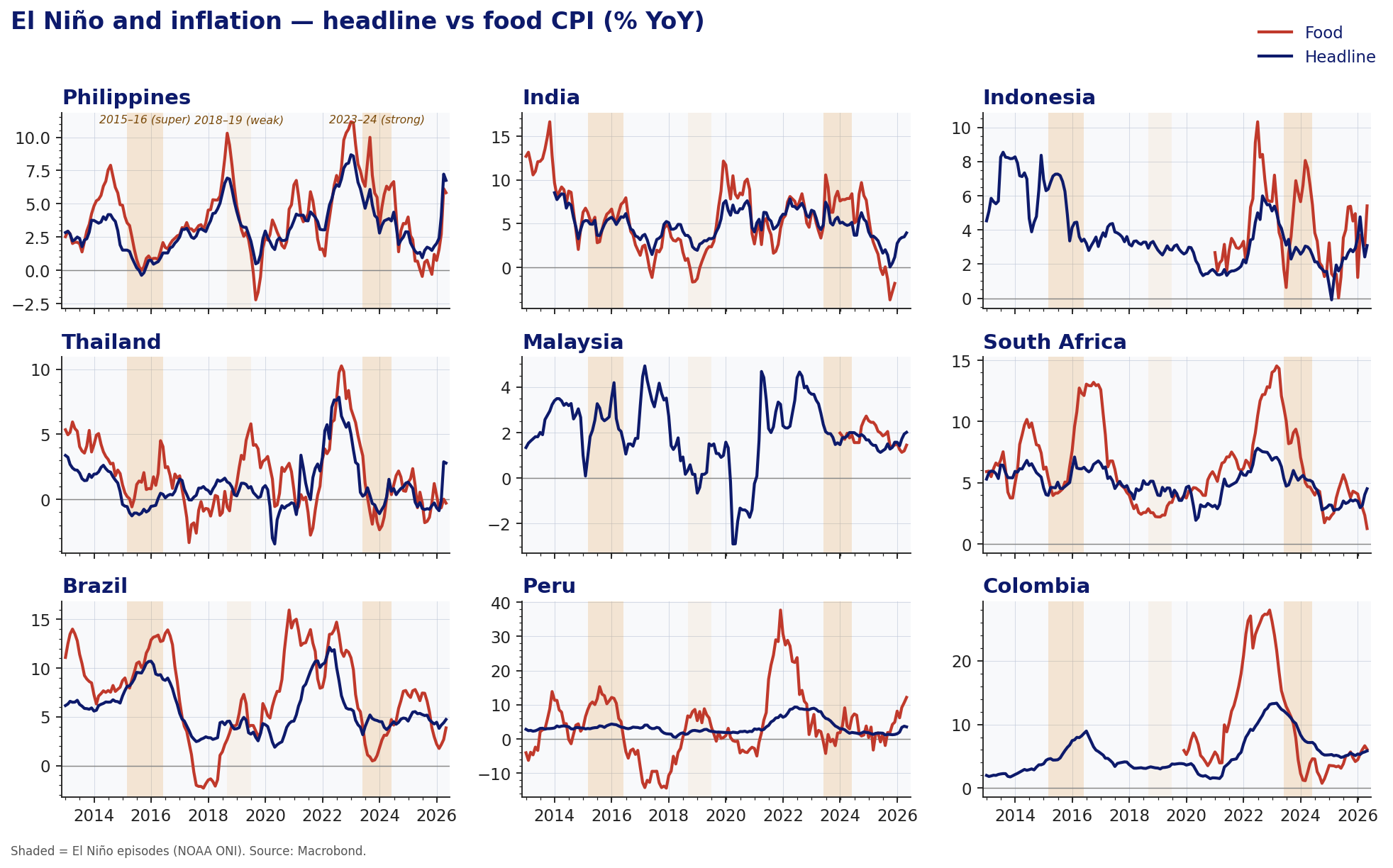

Figure 1 puts the current risk in historical context by comparing headline and food CPI inflation across nine emerging markets around select El Niño episodes. The shaded periods mark the 2015–16 super El Niño, the weaker 2018–19 episode, and the strong 2023–24 event.

Figure 1

The main message is that the inflation impact has been uneven but often clearest in food CPI. During 2015–16, food inflation rose sharply in several countries shown, including India, Brazil, Peru and South Africa, while the response was more limited or less persistent in Indonesia, Thailand and Malaysia. In 2023–24, food inflation again picked up notably in markets such as the Philippines, Indonesia, Thailand, South Africa, Peru and Colombia, with headline inflation generally moving less dramatically.

This pattern is consistent with El Niño acting primarily as a food-price shock. The pass-through to headline inflation depends on the size of the food basket, the persistence of the shock, exchange rates, policy responses and whether higher food prices spill over into broader inflation expectations.

How we measure and incorporate it

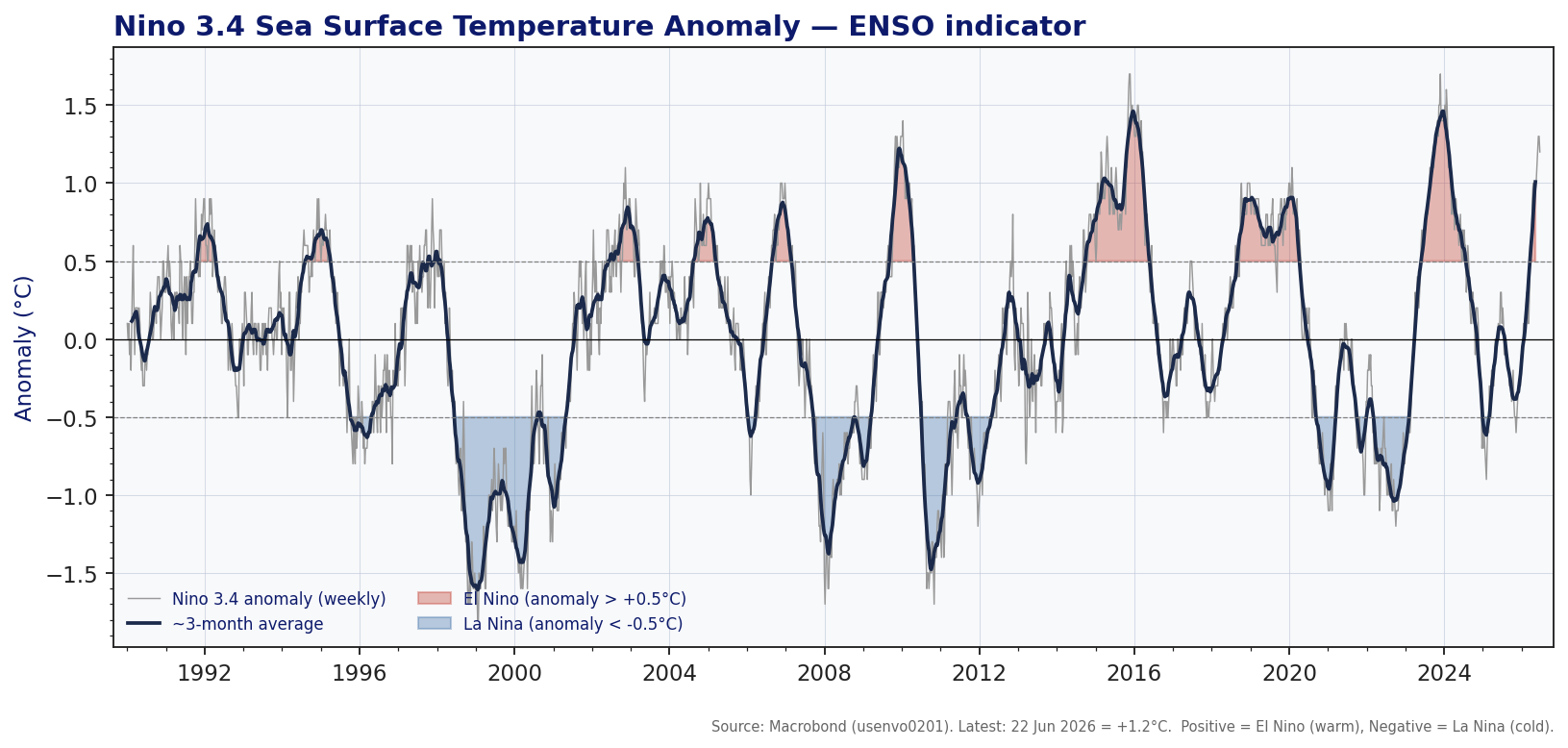

Because many crop, harvest and local supply indicators are released with a lag, and CPI captures the shock only after it reaches consumers, we track the chain as it develops. We anchor on the family of Niño-region sea-surface-temperature anomalies. The Niño 3.4 anomaly in the central Pacific is the broadest and most widely used official ENSO gauge, with readings above +0.5°C signaling El Niño and below -0.5°C signaling La Niña (Figure 2).

Figure 2

We complement it with region-specific anomalies tied to individual economies, using Niño indices where they have stronger historical links to local weather and food-price outcomes, including Niño 1+2 for coastal South America and Niño 4 for parts of Southeast Asia. Alongside these we track a granular set of satellite-observed variables tracked country by country including precipitation rate, snow depth, soil moisture content, sea surface temperature, sea surface wind speed, column water vapour and cloud liquid water. Availability varies with geography, so the input set is tailored to each country. We then add the conventional building blocks of food inflation, such as crop and harvest statistics and global food-price benchmarks. On top of these we layer high-frequency alternative data that reveals pressure before it reaches the consumer, such as freight activity, fertiliser and futures prices, and scraped retail prices from local supermarkets.

Overall, we expect El Niño to add upward pressure first to food inflation over the coming year. The headline effect should be strongest in emerging markets with large food baskets, weaker currency buffers and higher sensitivity to food-price shocks, and more muted across advanced economies unless the shock persists or feeds into broader inflation expectations.

Research Archive

Macroeconomic Insights: Hungary CPI – Food Prices on the Rise

At the end of May 2025, the Orban government decided to extend the profit margin cap on 30 essential food items through August 2025, in line with previous guidance stating the...

Macroeconomic Insights: Vegetable Prices Push India Inflation Downwards

In 2024, volatile vegetable prices repeatedly triggered in-market releases from India’s Price Stabilisation Fund (PSF). PSF, launched in 2014–15, was designed to curb extreme...

Macroeconomic Insights: Israel CPI – The Cost of War

Over the past 24 hours, Israel’s strike on Iran has markedly increased upside risks to inflation in the country. Just as tariffs introduce additional costs to consumers,...

Macroeconomic Insights: Spain CPI – Is it Time to Buy a House?

Since the start of the year, housing market indicators have increasingly correlated with rising inflation pressures. Interestingly, Spain classifies mortgages as financial...

Macroeconomic Insights: United States – A Bad Economy in a Good Economy

Our United States CPI YoY, NSA model continues to flag two quiet but disinflationary forces: a moderate rise in unemployment and trends in disability-program flows. To qualify...

Neudata New York conference 2025

When you're in New York, there are several things you have to have, a burger (preferably from Minetta Tavern), a cookie (preferably from Levain bakery on the Upper East Side) and...

Macroeconomic Insights: Trump Announces a Trade Deal With China. Will U.S. Inflation Go Down Now?

There’s just something about being in Geneva that makes you want to reduce tariffs on all Chinese goods from 145% to 30%. Recently, the U.S. and China reached an agreement to...

Trip notes from USA

Over the past week and half I’ve been travelling in America, starting with Chicago, then Omaha and finally New York. I’ve met many clients and attended various financial events,...

Macroeconomics Insights: Eurozone Inflation and The Price of Fun

On April 28, 2025, at approximately noon, I couldn’t send a message to a colleague. I thought there must have been a problem with my WIFI, until I realized that none of the...

Macroeconomic Insights: China Inflation & The Uncertainty Pandemic

Based on recent weekly forecasts, Turnleaf is projecting deflation of -0.09%YoY in April 2025 as export growth is expected to contract and China begins to reorganize its economy...

Berkshire Hathaway meeting 2025

Go to a fancy London steakhouse, and there will be a chance that you will get served steak from Nebraska. I’ve been to Nebraska many times over the years, and if there’s one...

Macroeconomic Insights: April 2025 Brings Lower Inflation in Hungary and Cheaper Chicken Wings

On March 17, 2025, Prime Minister Viktor Orbán’s government introduced a profit-margin cap across thirty essential goods, beefing up oversight to prevent cross-pricing strategies...

Macroeconomic Insights: Inflation Outlook Israel April 2025 – Key Drivers and Upside Risks

In our April 2025 inflation preview, we project headline CPI will undershoot consensus, underpinned by subdued Brent‐crude volatility, cheaper USD imports due to dollar weakness,...

Macroeconomic Insights: Measuring Inflation in Argentina Through Alternative Data

Just as Turnleaf has been applying alternative data to forecast inflation amid trade policy uncertainty, understanding Argentine inflation requires moving beyond conventional...

Macroeconomic Insights: Tariff Reprieves and Market Uncertainty — Implications for Inflation and Growth

Late last Friday, the U.S. administration announced exemptions for phones, computers, and chips from Trump's tariffs after imposing a 145% tariff against China – a large exporter...