Featured Research

Macroeconomic Insights: Hungary CPI Still Has a Long Way to Go

Turnleaf’s September 2025 headline inflation forecast for Hungary over the next 12 months points to an uptick toward 5% YoY by October 2025, followed by a steady decline into early 2026, with the trend reverting toward 4% YoY over the rest of 2026. With the Orban...

Macroeconomic Insights: Hungary CPI Still Has a Long Way to Go

Turnleaf’s September 2025 headline inflation forecast for Hungary over the next 12 months points to an uptick toward 5% YoY by October 2025, followed by a steady decline into early 2026, with the trend reverting toward 4% YoY over the rest of 2026. With the Orban administration’s campaign against unfair retail pricing still in force for another two months and global energy prices subdued, we attribute this profile primarily to underlying pressures in core subcomponents and base effects.

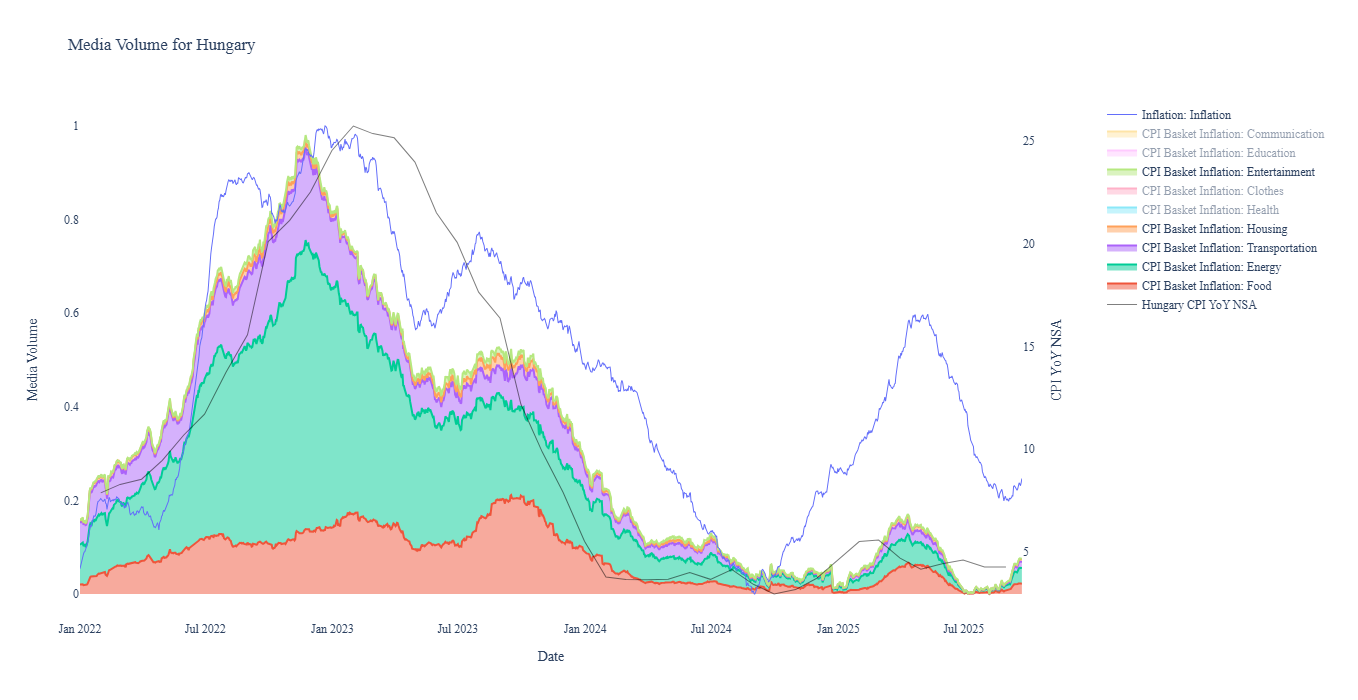

Inflation expectations remain high even with price controls. We see that our CPI Basket Media Volume Aggregate, which measures the total media volume reported relating to words associated with CPI Basket components, and the Inflation Media Volume, which measures the volume of media relating to the word ‘inflation’, is increasing in recent months for Hungary (Figure 1). This suggests that inflation concerns are reemerging as consumers begin to understand that price controls are temporary and that they should be expecting higher prices soon.

Figure 1

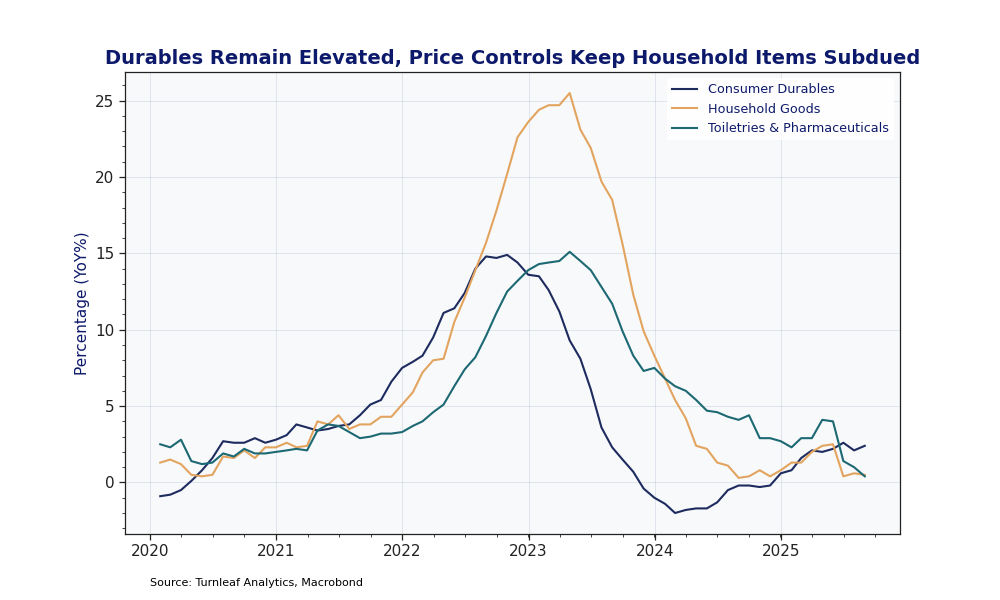

This may explain why, even after the recent forint appreciation, consumer durable goods remain elevated, relative to other categories that are covered by the price controls like household goods and toiletries and pharmaceuticals (Figure 2). We expect this to provide upwards pressure until base effects come into force at the end of the year.

Figure 2

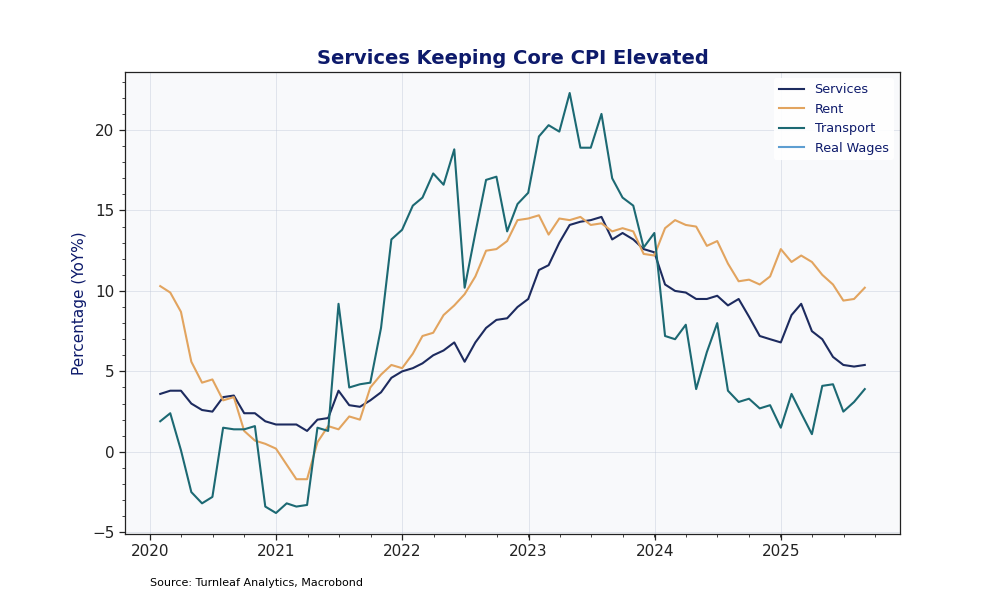

Figure 3

Research Archive

FILS Europe 2024 Takeaways

Paris is home to many things, the Eiffel Tower, the Arc de Triomphe, burgers (ok, I made that one up!). In recent years, Paris' financial community has grown, and indeed, every visit to Paris, there are an ever increasing number of firms who are interested in our...

Don’t look back in hanger steak

I'm currently in the queue for Oasis tickets. Rather than mindlessly watching the counter of people in the queue ahead of me fall (currently 184,984 people), I thought I'd start writing a blog article. Unfortunately, attempting to write a blog whilst hungry is perhaps...

The Olympic spirit for forecasting

The Olympics finally finished, and the Paralympics are about to begin. I managed to go to some of the Olympic football matches in both Lyon (in the photo above) and Nice. The vibe in general was very good, and you could see there was a lot excitement about the...

Eleven years of independence

Regrets become ever more edged with the passing of time. Recalling a time long gone, when perhaps a decision made, was not the decision you should have made, wastes little more than energy. By contrast, reflection on the past, peppered with both good and bad...

The human part of machine learning forecasts

I've seen a few videos showing a robot making a burger (here's one of RoboBurger for example). It seems pretty impressive that a machine can create a fresh burger. However, one thing seems missing in those videos. How do the ingredients get there? That part is kind of...

Takeaways from Eagle Alpha London 2024

Over the years the number of datasets which have come to the market have increased significantly. How do data buyers in the buy and sell side find such data? One way has been to approach individual sources of data, whether it is data vendors or corporates, ie. through...