Featured Research

Macroeconomic Insights: El Niño and the Inflation Outlook for the Year Ahead

A developing El Niño is becoming an important force in the inflation outlook over the next year. By shifting global rainfall patterns, it can bring drought to some regions and heavy rain to others, with the greatest economic impact often felt through food production....

Macroeconomic Insights: El Niño and the Inflation Outlook for the Year Ahead

A developing El Niño is becoming an important force in the inflation outlook over the next year. By shifting global rainfall patterns, it can bring drought to some regions and heavy rain to others, with the greatest economic impact often felt through food production. The Niño 3.4 sea-surface temperature anomaly has already crossed the El Niño threshold and is expected to strengthen further around the turn of the year.

The effects are likely to fall most heavily on emerging markets, especially those that are major agricultural producers, though the impact will vary by region. Drought across Southeast Asia, Australia and parts of India threatens crops such as rice, wheat, sugar, palm oil, coffee and cocoa. In South America, the picture is more mixed. El Niño can hurt coffee-growing regions in Colombia and northern Brazil, while bringing potentially beneficial rains to the grain belts of Argentina and southern Brazil.

Markets tend to price these risks quickly, often before actual crop shortfalls appear, but the pass-through to retail food prices is slower, typically taking six to sixteen months. The inflation impact is therefore likely to emerge with a lag, building through the year ahead and falling most heavily on food-sensitive emerging markets.

What previous episodes show

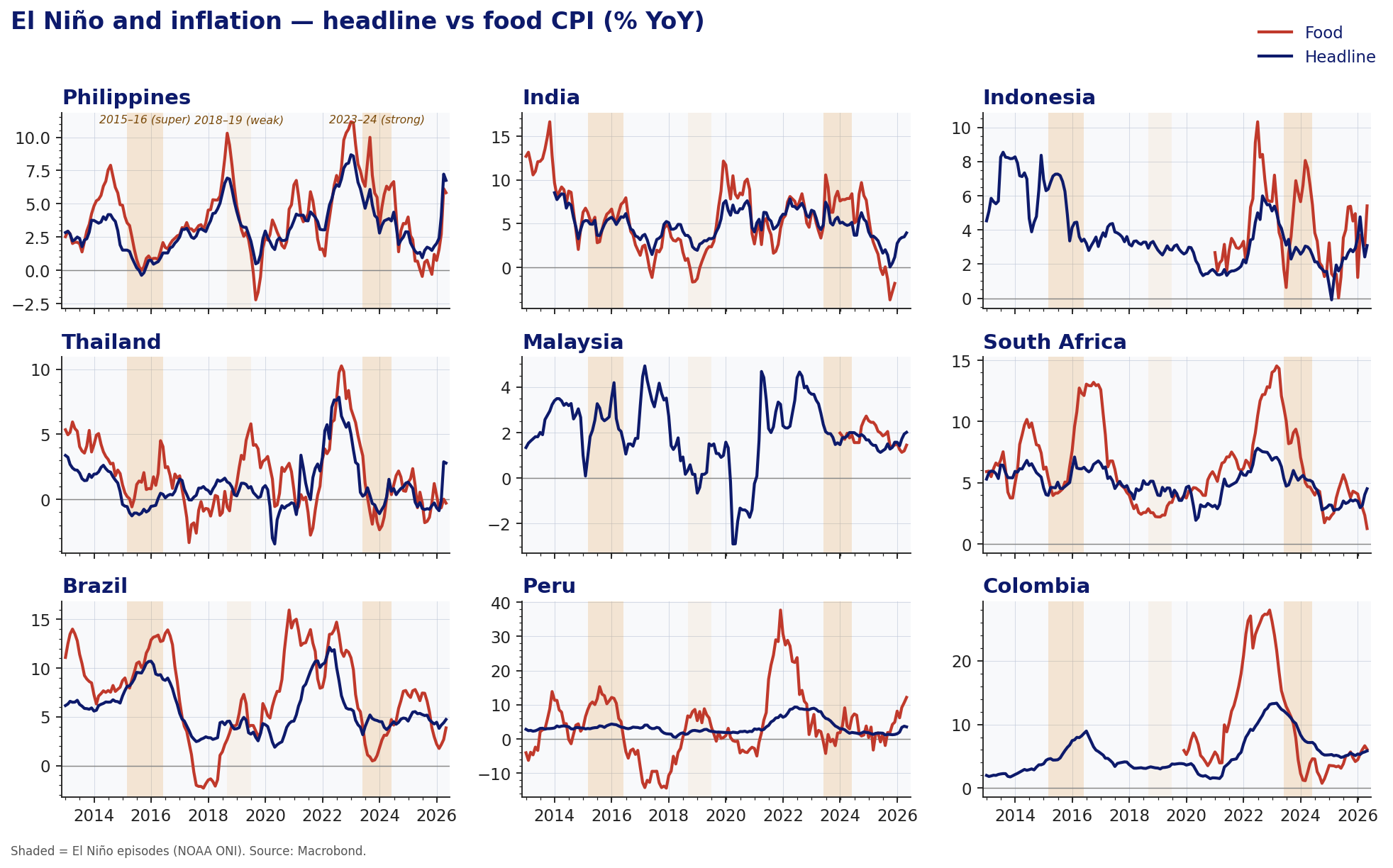

Figure 1 puts the current risk in historical context by comparing headline and food CPI inflation across nine emerging markets around select El Niño episodes. The shaded periods mark the 2015–16 super El Niño, the weaker 2018–19 episode, and the strong 2023–24 event.

Figure 1

The main message is that the inflation impact has been uneven but often clearest in food CPI. During 2015–16, food inflation rose sharply in several countries shown, including India, Brazil, Peru and South Africa, while the response was more limited or less persistent in Indonesia, Thailand and Malaysia. In 2023–24, food inflation again picked up notably in markets such as the Philippines, Indonesia, Thailand, South Africa, Peru and Colombia, with headline inflation generally moving less dramatically.

This pattern is consistent with El Niño acting primarily as a food-price shock. The pass-through to headline inflation depends on the size of the food basket, the persistence of the shock, exchange rates, policy responses and whether higher food prices spill over into broader inflation expectations.

How we measure and incorporate it

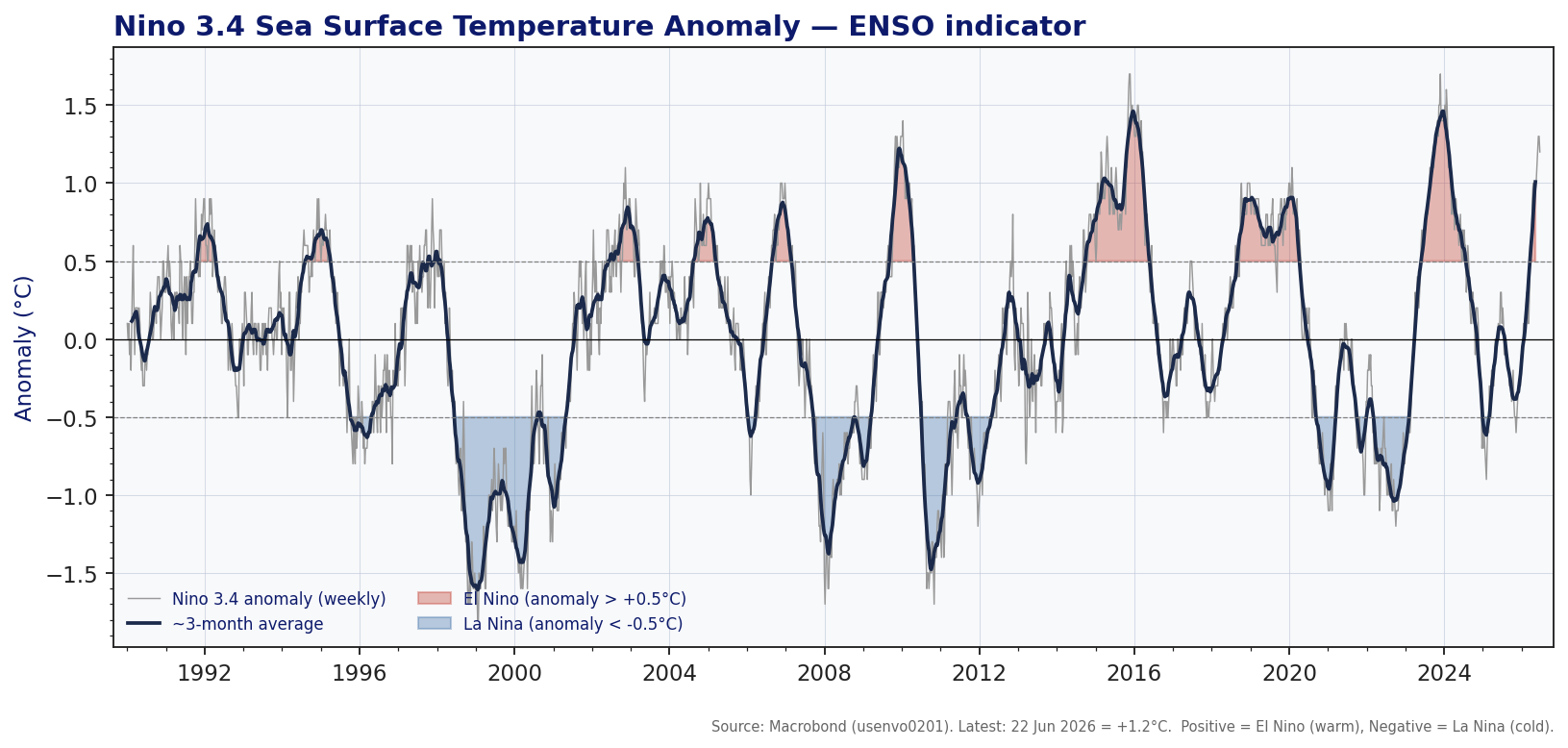

Because many crop, harvest and local supply indicators are released with a lag, and CPI captures the shock only after it reaches consumers, we track the chain as it develops. We anchor on the family of Niño-region sea-surface-temperature anomalies. The Niño 3.4 anomaly in the central Pacific is the broadest and most widely used official ENSO gauge, with readings above +0.5°C signaling El Niño and below -0.5°C signaling La Niña (Figure 2).

Figure 2

We complement it with region-specific anomalies tied to individual economies, using Niño indices where they have stronger historical links to local weather and food-price outcomes, including Niño 1+2 for coastal South America and Niño 4 for parts of Southeast Asia. Alongside these we track a granular set of satellite-observed variables tracked country by country including precipitation rate, snow depth, soil moisture content, sea surface temperature, sea surface wind speed, column water vapour and cloud liquid water. Availability varies with geography, so the input set is tailored to each country. We then add the conventional building blocks of food inflation, such as crop and harvest statistics and global food-price benchmarks. On top of these we layer high-frequency alternative data that reveals pressure before it reaches the consumer, such as freight activity, fertiliser and futures prices, and scraped retail prices from local supermarkets.

Overall, we expect El Niño to add upward pressure first to food inflation over the coming year. The headline effect should be strongest in emerging markets with large food baskets, weaker currency buffers and higher sensitivity to food-price shocks, and more muted across advanced economies unless the shock persists or feeds into broader inflation expectations.

Research Archive

Learning from running financial models live

Let's say you are the world's best burger chef (we all have ambitions, right). You'd be serving up all manner of burgers for your customers. It would be odd though, wouldn't it,...

Macroeconomics Insights – Beyond Tariffs: How Uncertainty is Steering U.S. Inflation Expectations

When we forecast inflation, our goal is to account for as much explainable variation as possible, using available data and reasonable assumptions about how prices evolve....

Macroeconomic Insights: Tariffs, Manufacturing, and Mexico Inflation

This article marks the start of Turnleaf’s series on how U.S. tariffs shape inflation dynamics across Latin America (LATAM). Among the economies we monitor—Colombia, Brazil,...

Macroeconomic Insights: How U.S. Tariffs and Eurozone Weakness Are Shaping Chinese Inflation

The trajectory of Chinese inflation will largely depend on its sensitivity to U.S. tariffs and its ability to sustain domestic GDP growth through external demand, particularly...

Macroeconomic Insights: Prices to Increase in February 2025 as Canada’s Tax Holiday Takes a Holiday

Between mid-December 2024 and mid-February 2025, the Canadian government implemented a GST/HST tax holiday, exempting beverages, restaurants, children’s clothing and footwear,...

Macroeconomic Insights: Fueling the Inflation Fire – Turnleaf’s Turkish Inflation Curve Shifts Upwards

Turnleaf’s latest data has pushed Turkey’s inflation outlook higher than consensus forecasts. There are multiple reasons for this which we will explain in this note. One of the...

Macroeconomic Insights: Assessing the Inflationary Impact of U.S. Steel & Aluminum Tariffs

The newly announced 25% tariff on U.S. steel and aluminum imports introduces cost pressures across global supply chains. However, the key question is not just how markets react,...

Emerging Markets: January 2025 Colombia and Hungary CPI YoY Forecast Review

2025 Colombia CPI YoY Above Consensus Due to Global Inflation Pressures Turnleaf’s CPI YoY model projects Colombia inflation well above consensus 12 months out, as it more...

Emerging Markets: January 2025 India CPI YoY Forecast Review

In our January 2025 YoY CPI forecast, we projected inflation at 4.57%, slightly above the realized 4.3%, yet outperforming consensus (4.71%)—even with our estimate released a...

Macroeconomic Insights: 2025 Eurozone Inflation Outlook – 4 Key Charts to Watch

Turnleaf is forecasting 2–2.5% headline inflation for the Eurozone in 2025, while core inflation is expected to decline through the end of the year towards 2% as momentum in wage...

DeepSeek, objectives and constraints

When a new burger joint opens up, there's often a buzz. Everyone (well, at least me) wants to try the new burger. Is it as good as it looks on Instagram? Or is it just style over...

Hundreds of quant papers from #QuantLinkADay in 2024

I tweet a lot (from @saeedamenfx and at BlueSky at @saeedamenfx.bsky.social)! In amongst, the tweets about burgers, I tweet out a quant paper or link every day under the hashtag...

What we’ve learnt from reading thousands of Fed communications

We recently had the last FOMC decision of 2024. Market l participants reacted to the hawkish tone including Powell’s comments that the Fed’s year-end inflation projection has...

Flash Inflation Outlook: The Cost of Stability, Poland’s Extended Energy Caps

The Polish government’s decision to extend the cap on electricity prices at 500 PLN/MWh is a critical measure to limit inflationary pressures on households. To understand its...

Macroeconomic Insights: A Pinch of Real Rates, a Dash of Slack: Turnleaf’s 2025 U.S. Inflation Recipe

At Turnleaf Analytics, leveraging our machine learning models, we project U.S. inflation to stabilize between 2–3% through 2025, shaped by the interplay of import inflation,...