Over the past three weeks, the escalation of conflict in the Middle East has coincided with a clear increase in Brent crude prices, reinforcing the expectation of near-term upward pressure on CPI through the energy channel. However, focusing solely on oil overlooks other critical transmission mechanisms linked to the region’s role in global commodity flows.

In particular, the Strait of Hormuz is a key transit route not only for crude oil but also for industrial inputs such as urea, which is essential for fertilizer production. These inputs play a non-trivial role in agricultural cost structures and, by extension, food price dynamics.

While energy price shocks typically transmit rapidly into headline inflation via transport and fuel costs, the pass-through into food prices is more gradual and operates through indirect channels. These include input costs (fertilizers), production cycles in agriculture, and distribution costs, all of which introduce meaningful lags.

Consistent with this, there is limited evidence so far of an immediate response in proprietary food price indices (e.g., the Eurozone). This likely reflects short-term frictions such as existing inventories, pre-contracted pricing, and the seasonal nature of agricultural production, rather than an absence of underlying pressure.

Given the persistence and uncertainty of the current shock, it is therefore necessary to distinguish between immediate and lagged transmission channels. Specifically, the relevant pathways include:

- Brent crude → fuel and transport costs → headline CPI (short horizon)

- Brent crude → production and distribution costs → food prices → CPI (medium horizon)

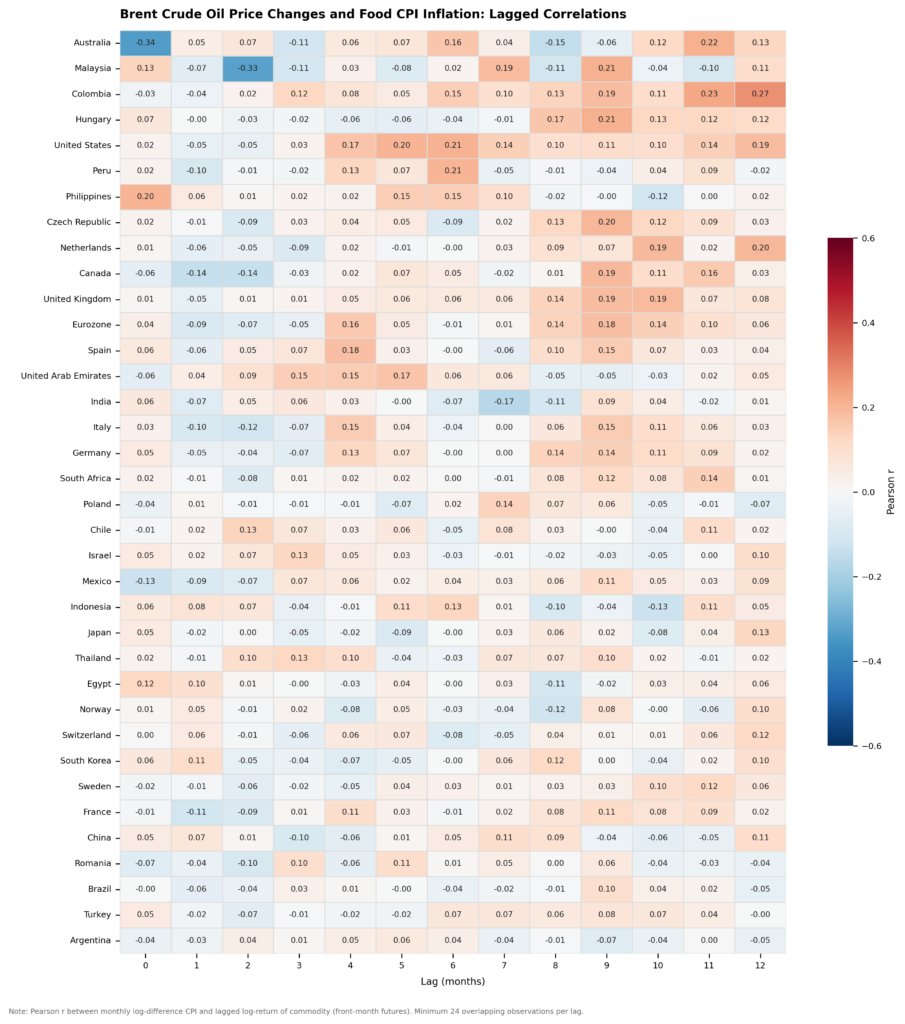

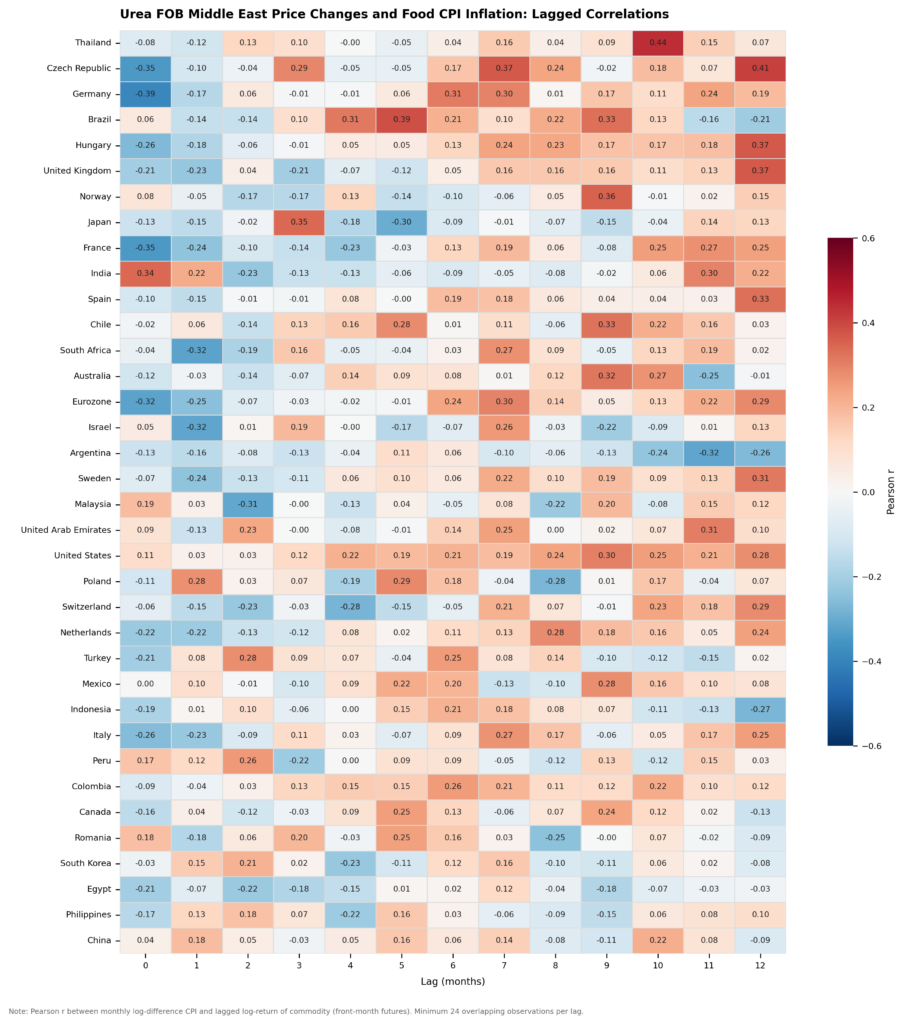

The heatmaps below show lagged correlations between changes in Brent crude and urea prices and food CPI inflation over a 0–12 month horizon. These are intended to characterize timing and relative strength of pass-through rather than establish causality.

For Brent crude (Figure 1), correlations are weak at short lags but strengthen at longer horizons, with a broad clustering in the 9–12 month range. This is consistent with a delayed transmission into food prices via transport, processing, and distribution costs. While the magnitudes are moderate, the consistency across countries points to a common lag structure.

Figure 1

Urea (Figure 2) shows a more direct but less uniform pattern. Correlations are generally stronger and emerge earlier, typically in the 4–7 month range, consistent with fertilizer application and crop cycles. The dispersion across countries reflects differences in fertilizer dependence and agricultural structure.

Figure 2

Negative correlations at short lags in several economies likely reflect temporary offsetting factors—such as favorable harvests or inventory adjustments—rather than true inverse relationships. The shift toward positive correlations at longer lags underscores the importance of delayed cost pass-through.

Taken together, the evidence points to a layered transmission process: energy effects dominate in the near term, while fertilizer-related pressures emerge later and with greater heterogeneity. This suggests that the current oil shock is unlikely to drive immediate food inflation but may exert upward pressure over a 6–12 month horizon, with fertilizer dynamics representing an additional, independent risk channel.

Looking ahead, the key risk is not the immediate CPI response, but the potential for a second-round effect as higher input costs gradually feed through into food prices. If elevated energy and fertilizer prices persist, the combination could lead to a more sustained and broad-based inflation impulse than currently reflected in near-term data.