Turnleaf reads the current inflation data as a test of duration. Fuel prices have lifted headline CPI, while core has stayed contained because energy prices have not remained elevated long enough to force broad repricing across non-energy goods and services. Current pricing assumes the conflict ends before inventories, reserve releases, tax cuts, and price caps lose their ability to absorb the shock.

The inflation component panels frame the shock through that lens. Fuel prices have turned higher across several regions since the Iran shock marker, but headline and core have not moved in a uniform way. In the net oil-importing or fuel-exposed economies of Asia-Pacific, the renewed fuel impulse appears alongside more visible headline re-acceleration. Developed Europe shows a more uneven response because tax wedges, retail interventions, and regulated prices dampen the first pass-through. Emerging EMEA looks relatively benign in some headline and core series, although the fuel lines and policy setting suggest suppressed pressure rather than full insulation. Latin America remains more insulated among the larger energy and commodity-producing economies, while Chile and Peru look closer to the oil-importer cases. The United States occupies an intermediate position, with fuel inflation rising and headline following, while producer income, restrictive policy, and earlier goods disinflation have so far limited the move into core.

The comparison with 2022 helps frame the timing. In the earlier shock, fuel moved first, headline followed, and core adjusted later as energy costs interacted with reopening demand and tight labor markets. The 2026 setting is less straightforward. Core inflation has already fallen from its peak, monetary policy remains restrictive, and markets have more reason to assume that firms cannot pass through every cost increase. That backdrop makes the current shock more dependent on persistence than on the initial fuel spike alone.

Market pricing appears consistent with an assumption that the conflict will end before the shock crosses that persistence threshold. Under that view, fuel can lift headline inflation for a period without remaining high enough to reset freight contracts, airfares, food production costs, petrochemical inputs, packaging costs, utilities, and other prices inside core. Turnleaf’s disagreement concerns the durability of the shock and the buffers absorbing it. The first-round fuel move is already visible. The open question is whether those buffers last long enough to prevent broader repricing across non-energy goods and services inside core.

Asia-Pacific shows the strongest net oil-importer and fuel-exposure pressure, with renewed headline acceleration in several economies near the Iran shock marker. In country labels throughout the figures, [R] identifies documented reserve releases.

Figure 1

Developed Europe shows a more uneven fuel impulse because tax wedges, retail interventions, and regulated prices dampen the first move.

Figure 2

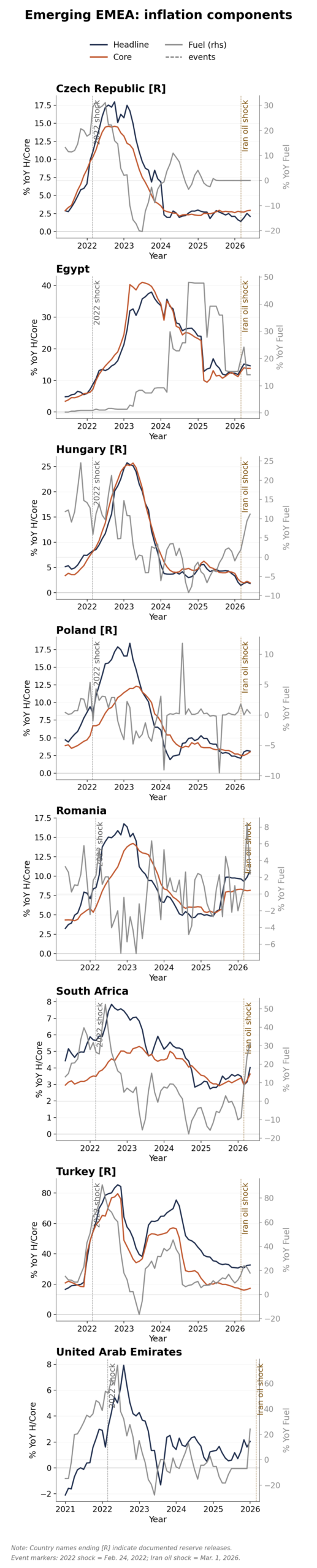

Emerging EMEA shows headline and core prints that look benign in some countries, but the fuel lines suggest that policy and pricing arrangements have suppressed part of the shock.

Figure 3

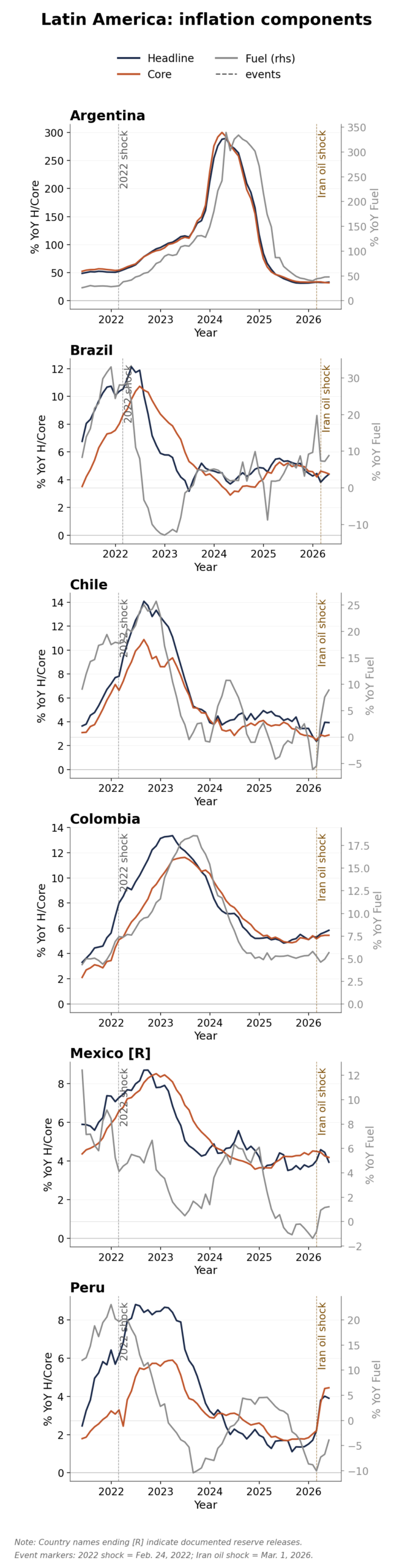

Latin America remains more insulated among the larger energy and commodity-producing economies, while Chile and Peru look closer to the oil-importer cases.

Figure 4

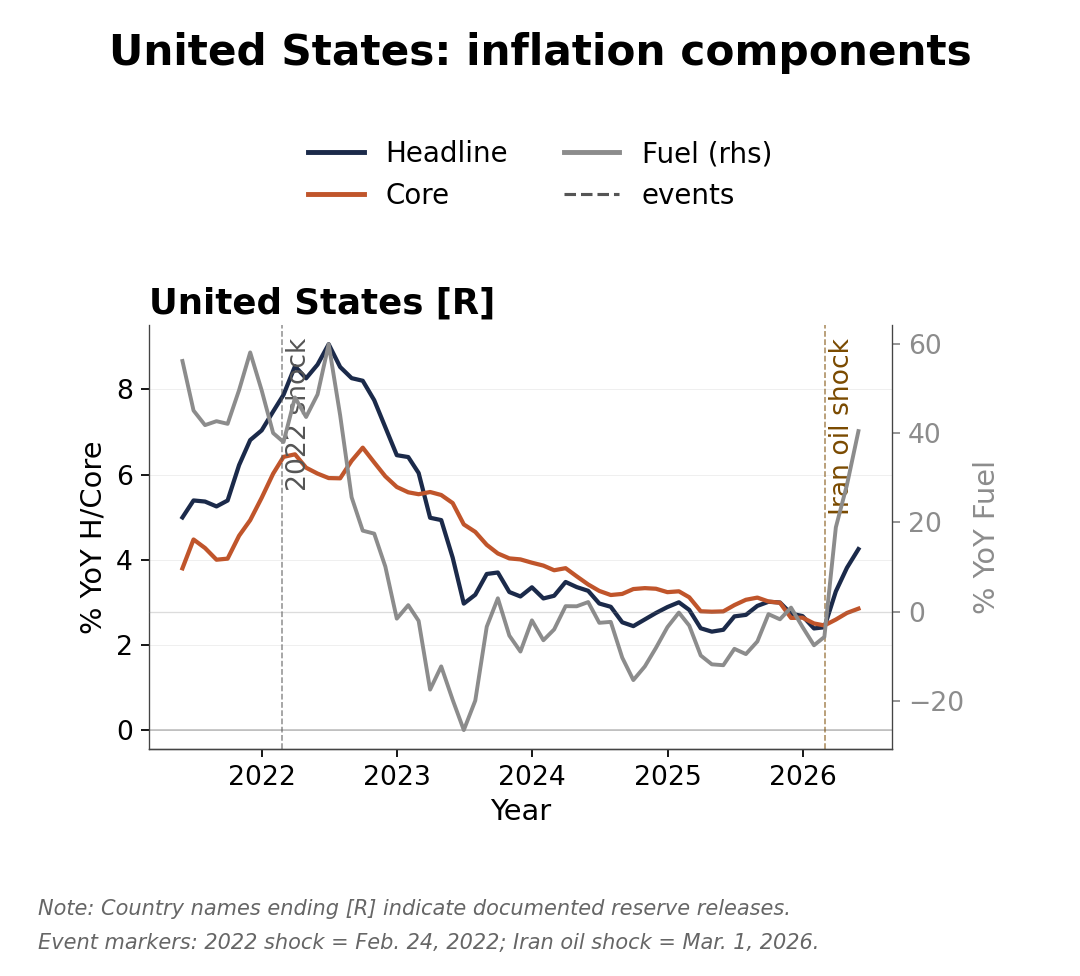

The United States occupies an intermediate position between the net oil-importing or fuel-exposed cases and the producer economies. Fuel inflation has increased and headline inflation has followed, while core inflation has remained comparatively contained. Producer income, restrictive monetary policy, and earlier goods disinflation have slowed the transmission into core. The U.S. figure therefore speaks less to immediate pass-through than to timing. It shows a first-round fuel shock whose broader core effects remain contingent on the duration of the conflict and the erosion of inventories, fiscal buffers, and pricing restraint.

Figure 6

Reading the fuel panel

The fuel-tax panels explain why headline inflation has remained relatively benign in several countries despite the common oil shock. A higher crude price reaches CPI only after passing through the pump-price system, where tax policy, subsidies, and retail caps determine how much of the global product-price move households actually pay. The labels in each panel report the CPI weight of petrol or diesel and the latest contribution to headline inflation, so they show both the retail price move and the share of the consumption basket exposed to that move.

The 2026 drop in fuel-tax shares shows the policy buffer most clearly. In developed Europe, petrol and diesel fuel-tax shares fall sharply in Spain, Germany, Italy, France, Sweden, and the euro area aggregate, with the series capturing excise and VAT or sales tax effects where applicable. Those cuts reduce product-cost pass-through at the pump, which helps explain why headline inflation has not moved as much as the crude shock alone would imply. Spain gives the clearest example. Petrol carries a 2.28 percent CPI weight but adds only 0.03 percentage points to headline inflation, while diesel carries a 2.44 percent weight and adds 0.32 percentage points. Petrol looks contained because policy has absorbed much of the shock. Diesel still matters because it feeds freight, farming, construction, and distribution.

To read the rest, visit our latest Substack post, here.