The wireless telephone services component of US CPI has been behaving strangely over the past year. The recent behaviour is really two things stacked on top of a long structural trend.

The first is a methodology change. From the July 2025 CPI, released in August, BLS switched wireless telephone services to an alternative data, hedonic approach, scraping a near universe of carrier and MVNO plan prices, running them through a hedonic regression re-estimated every month, then aggregating with a Törnqvist index. That made the series move more sharply than it used to.

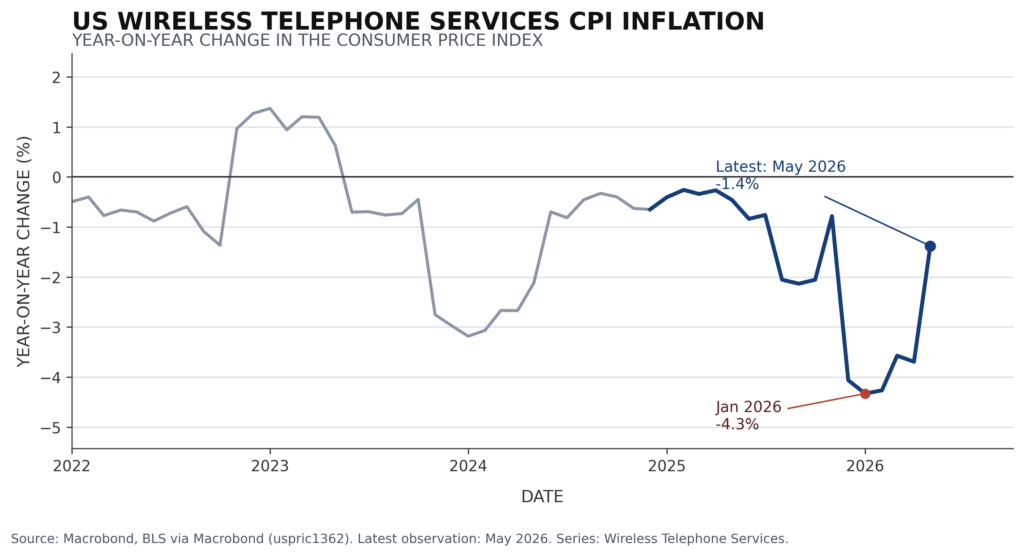

The second is a competitive plan shock followed by spring price hikes. BLS’s wireless telephone services CPI is built from plan level price and characteristics data for MNO and MVNO service plans, so broad changes in available plan pricing can flow through to the index. A late 2025 competitive push on lower priced prepaid and unlimited plans appears to have coincided with a 3.3% seasonally adjusted drop in December, the largest one month decline since March 2017, with the 12 month rate at -4.1%. The 12 month rate then bottomed at about -4.3% in January (Figure 1). In spring 2026, AT&T raised prices on select retired unlimited wireless plans beginning in April, while Verizon’s Unlimited Ultimate 1.0 became unavailable to add after May 7, and industry reporting put the new Unlimited Ultimate price at $5 a month higher. The wireless index then rebounded 2.2% in May, moving the 12 month rate back to -1.4%.

At Turnleaf, we make sure to track carrier announcements for these moves as they happen and apply a forward looking adjustment to our inflation nowcasts when material changes appear.

Figure 1

Underneath both of these developments is a much longer structural story. The index is down around 54% since 1997, and that decline has little to do with what any individual household actually pays each month. The index is quality adjusted, and carriers have spent the past quarter century bundling ever larger amounts of high speed data into plans that cost roughly the same as before. BLS treats that additional data as equivalent to a price cut, so the measured price falls even when the actual bill stays flat.

A few points are worth stressing given how easily a series like this gets misread.

To read the rest of this article, please visit our latest Substack post here.