Gold jewelry remains a common wedding gift in Turkey, reflecting a cultural practice where households preserve wealth through physical gold rather than financial assets. This preference, formed through decades of high inflation and currency instability, has accumulated into a substantial economic force. Turkish households now hold approximately $500 billion in physical gold outside the banking system, according to central bank estimates as of October 2025. This represents more than a $100 billion wealth effect gain over the past year as gold prices surged.

Turnleaf tracks this phenomenon closely because household gold holdings directly affect how monetary policy influences consumer behavior. When gold prices rise, households become wealthier and can sustain consumption even when the central bank keeps interest rates high to cool demand. Turnleaf’s inflation models incorporate gold price movements as a key driver of household wealth effects, which helps explain why Turkey requires longer periods of restrictive policy to achieve disinflation.

Despite this structural constraint, Turkey’s disinflation accelerated through 2025. Annual inflation fell to 30.89% in December from 44% in May 2024. Turnleaf expects inflation to reach the mid-20s by year-end 2026, overshooting the central bank’s 16% interim target (Figure 1 – visit Turnleaf’s Substack to view the latest forecast). The gap between Turnleaf’s forecast and the official target reflects persistent services inflation and the gold wealth channel limiting how quickly demand cools.

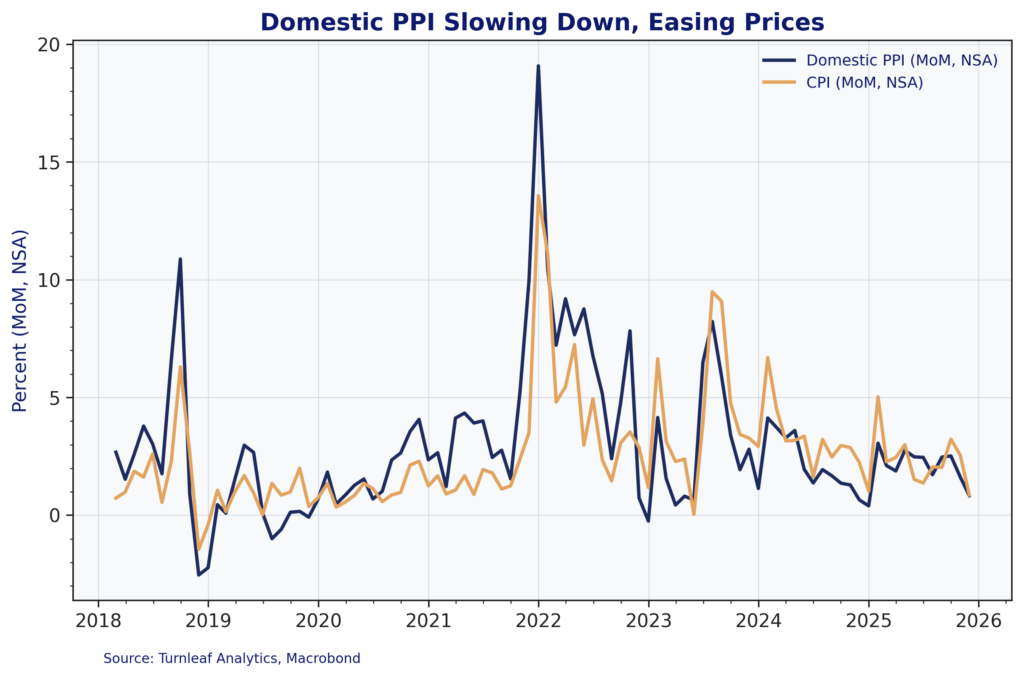

Policy rate increases have transmitted more effectively to goods prices than services prices. Domestic producer prices decelerated as weaker demand forced firms to choose between maintaining prices and losing volume, which drives most of the headline improvement (Figure 2). This channel works as expected with manufacturing firms facing hard demand constraints and adjusting prices accordingly.

Figure 2

However, producer prices respond quickly to currency depreciation and energy costs, creating vulnerability to external shocks. Lower US and Eurozone inflation has reduced imported cost pressure, providing temporary relief. Turnleaf monitors external inflation developments closely because Turkey’s import dependence means foreign price pressures can quickly reverse domestic disinflation progress.

Services Inflation Persistent

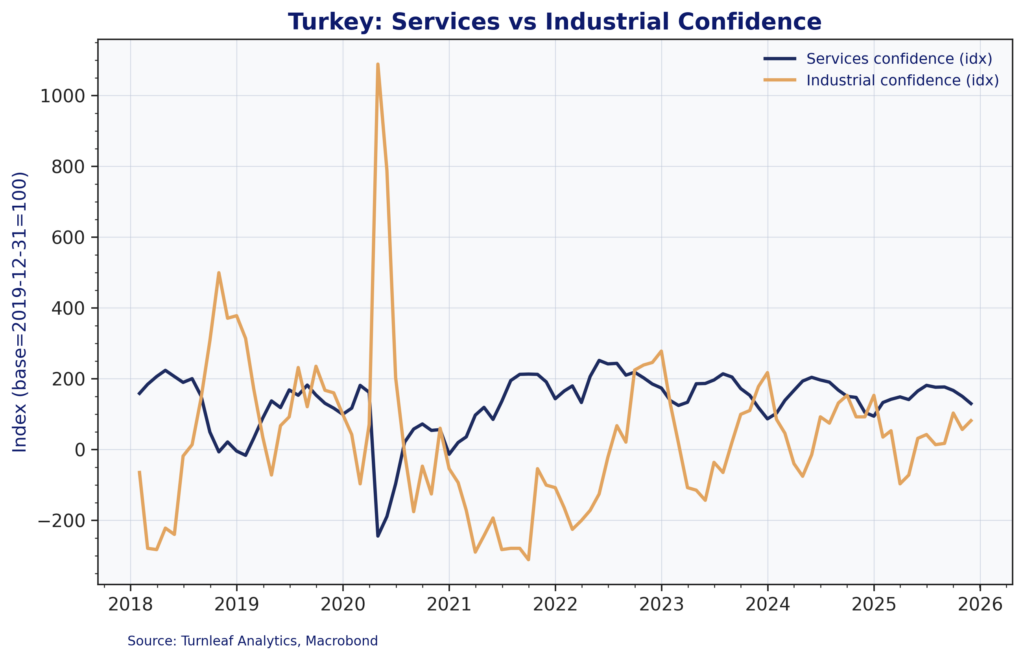

The divergence between goods and services inflation follows the pattern Turnleaf’s models predict. Services sectors are labour-intensive and set wages based on past inflation rather than forward-looking targets, creating inertia in their price adjustments. While industrial confidence has fallen alongside goods price pressures, services confidence remains elevated (Figure 3). Construction, hospitality, and similar sectors retain pricing power tied to historical wage settlements.

This backward-looking wage formation slows services disinflation substantially. The 27% minimum wage increase for 2026, though consistent with projected inflation, locks in high nominal labour costs for the year ahead. Turnleaf’s model has flagged upward pressure from labour-intensive industries, particularly construction, where pricing typically lags the broader disinflation trend by six to nine months. Services prices will therefore decline more gradually than goods prices even as overall demand conditions weaken.

Figure 3

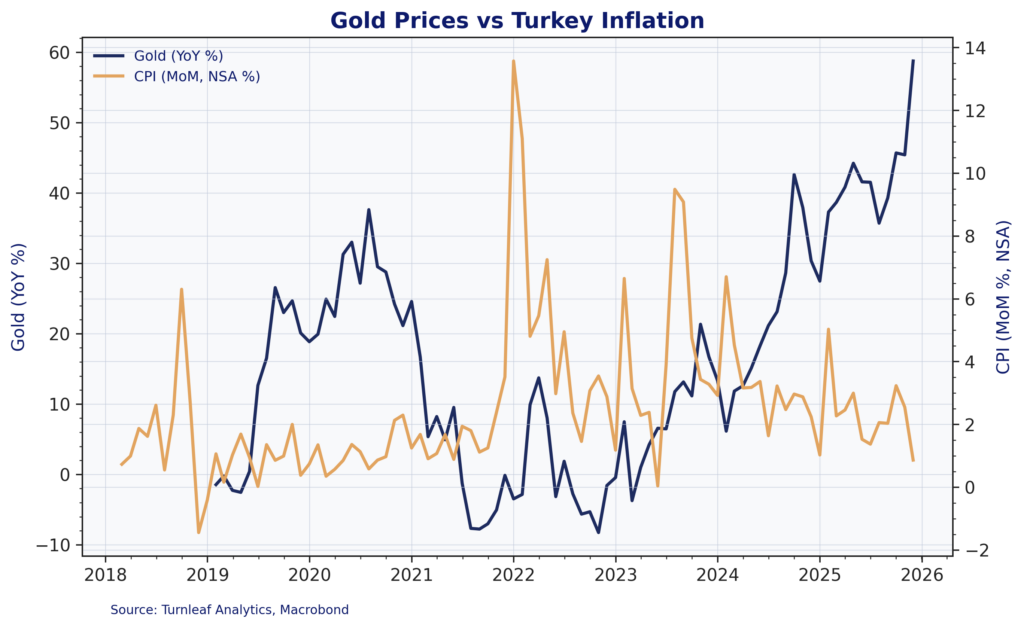

Gold Prices and Household Demand

The scale of household gold holdings fundamentally shapes monetary policy transmission in Turkey. Turnleaf’s consumption models incorporate gold price changes as a direct input to household wealth, which has proven essential for accurate inflation forecasting. Higher gold prices increase household net worth and provide liquidity when credit tightens (Figure 4). Households can maintain consumption by drawing on gold wealth rather than cutting spending when borrowing costs rise.

Figure 4

Reserves, Liquidity, and Financial Conditions

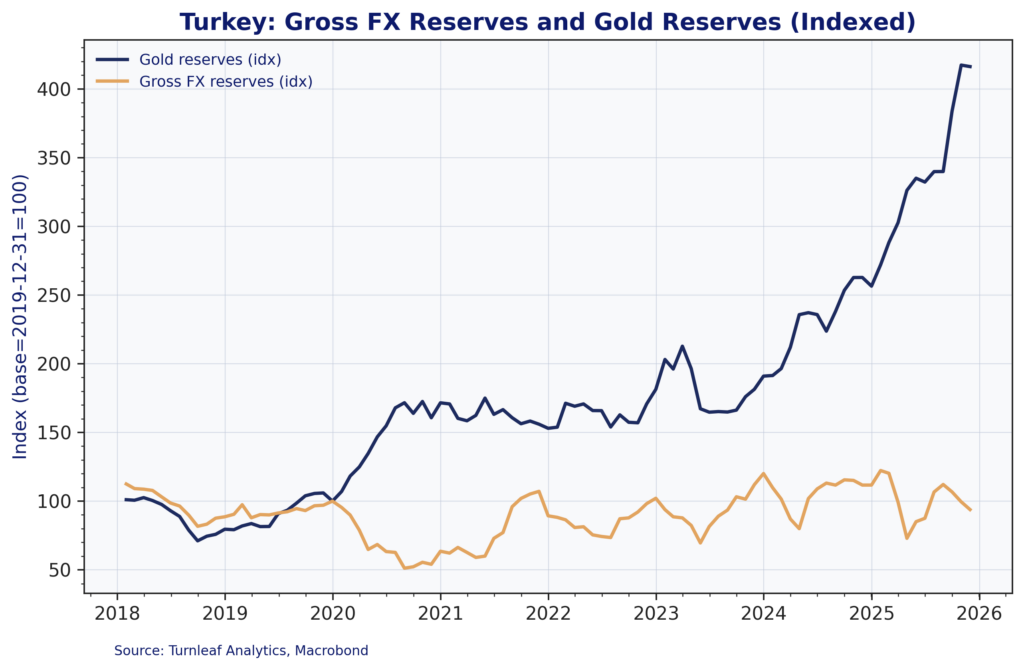

The central bank’s reserve position improved substantially through 2025. Rising gold prices alone added $30 billion to this total, lifting reserve buffers without requiring equivalent foreign exchange accumulation (Figure 5).

Figure 5

While stronger reserves support exchange-rate stability, the composition creates a dual dynamic that Turnleaf monitors closely. The same gold appreciation that improves the central bank’s balance sheet also strengthens household balance sheets, sustaining domestic demand. Financial conditions tightened without corresponding demand contraction. Consumer credit continued growing in some segments despite restrictive monetary policy, reflecting households’ ability to maintain consumption through gold-backed liquidity.

The successful unwinding of the KKM deposit protection scheme without triggering dollarization demonstrates improved policy credibility. High nominal interest rates on lira deposits reinforced this stability by sustaining lira savings. This allowed policymakers to cut the policy rate by 950 basis points since June to 38% without destabilizing the currency. But this flexibility depends on continued control of cost pressures and inflation expectations, neither of which is guaranteed given structural rigidities in services pricing and wealth effects sustaining demand.

Turnleaf’s Assessment

Turkey’s disinflation has progressed further than most observers anticipated, driven by sustained tight policy, favourable external conditions, and stronger reserves. Turnleaf’s forecast for mid-20s inflation by end-2026 reflects both this progress and the remaining structural constraints. Services inflation will decline more slowly than goods inflation due to backward-looking wage indexation. The gold wealth channel will continue buffering household consumption against monetary tightening, particularly if gold prices remain elevated or rise further.

Administrative price adjustments in utilities and regulated items add volatility to monthly readings but do not fundamentally alter the disinflation path. The larger risks come from deviations from fiscal discipline, renewed external market stress, unanchored inflation expectations, or currency volatility — any of which could interrupt progress toward the central bank’s medium-term price stability goal.