Over the past several months, Turnleaf has examined the inflationary impact of the Iran conflict across fuel, food and airline prices, as well as the intermediary inputs that compound price increases. We have seen these dynamics play clearly into our nowcasting models, but a hidden cost is now emerging. The UK offers a clear case study of a broader global pattern, in which a more persistent risk is building in core goods through freight, agricultural inputs and non-food raw materials.

The shock works through slower-moving business costs that persist across inventory cycles, procurement decisions and supplier contract negotiations before they are fully reflected in shelf prices. This lag makes the effect harder to observe in real time, while increasing its relevance for the inflation outlook.

In the UK, our models are already flagging rising pressure across non food agricultural commodity indices, industrial raw material inputs, textile fibres and the BRC non food shop price index. The figures below trace the transmission path from agricultural and freight costs into broader non food input pressure. Retail pass through remains limited so far, but the next stage is the repricing period, when firms decide how much of these higher costs to pass on to consumers.

Two mechanisms are driving the UK case

Shipping is the most immediate channel. The Gulf is a critical route for oil, LNG, fertiliser and chemical exports, and any disruption to normal traffic raises costs by forcing vessels onto longer routes, increasing insurance premiums and delaying delivery times. Freight rates have already risen sharply, adding both cost and delay to the supply chains that feed UK core goods production and retail distribution.

The second is broader pressure across non-food inputs. Higher energy and freight costs raise the delivered price of raw materials used in everyday manufactured goods. Cotton, textile fibres, wood pulp, rubber-related inputs and plant oils sit outside the energy basket, but they remain exposed to the same conflict-driven disruption through fertiliser, petrochemicals, shipping and dollar-denominated trade.

A related channel runs through agricultural chemicals. Pesticides are petrochemical derivatives, so an energy shock raises farm-level production costs beyond fertiliser alone. When fertiliser, pesticides and freight all rise together, the pressure can move beyond agriculture and feed into the cost of UK non-food manufactured goods.

The data is already moving

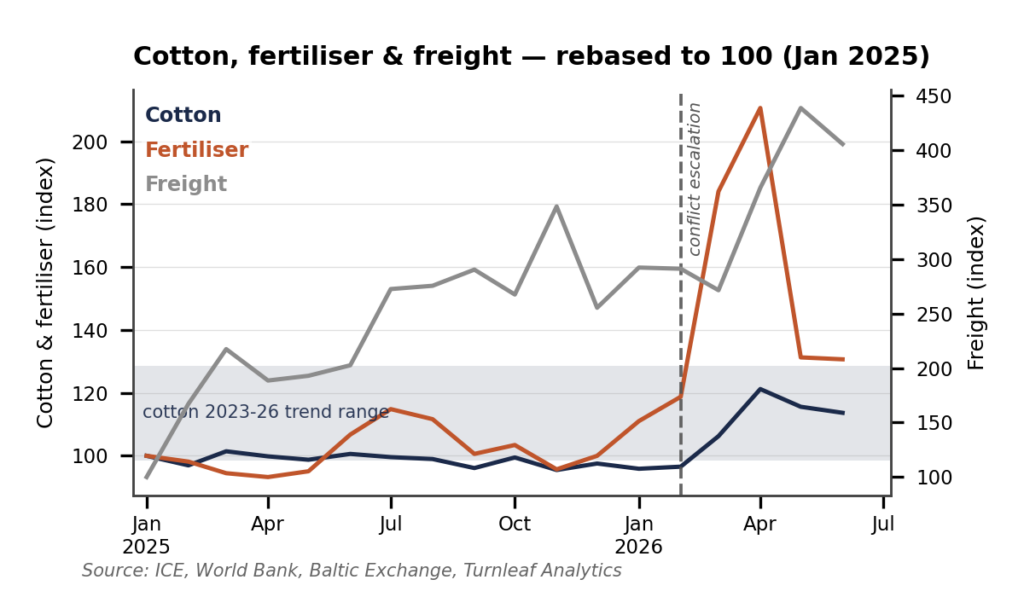

Figure 1 helps describe the agricultural input channel. Cotton moved towards the upper limit of its 2023 to 2026 trend range after the conflict escalation, while fertiliser spiked sharply and freight remained elevated on the right hand axis. Figure 1 shows that the main upstream costs behind textile production are rising together, strengthening the case that core goods inflation pressure are beginning to develop.

Figure 1

Figure 1. Cotton, fertiliser and freight indices, rebased to 100 in January 2025.

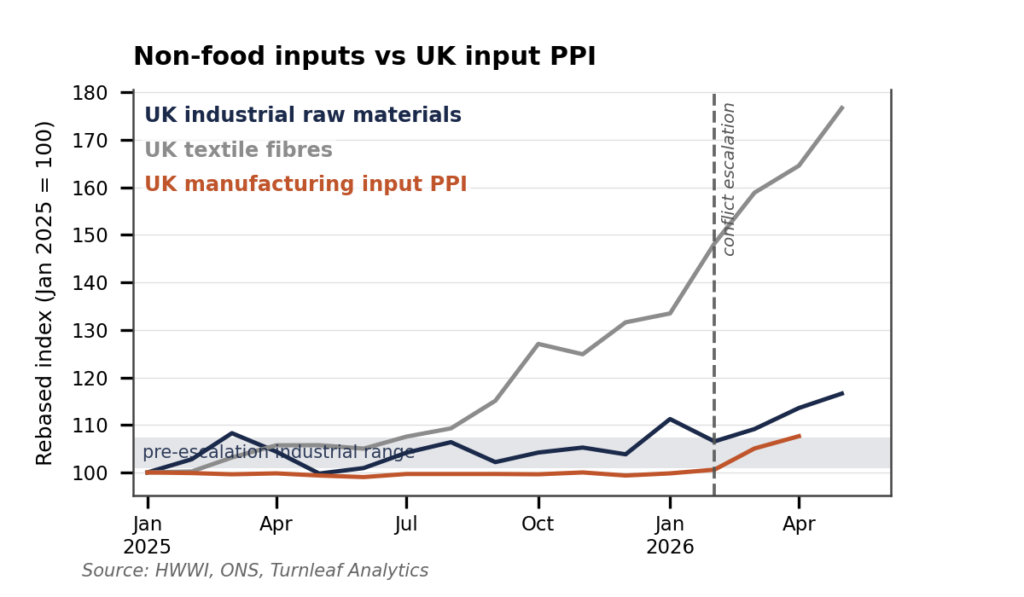

Figure 2 conveys a similar dynamic. UK textile fibres rose steeply through the post-escalation period, while UK industrial raw materials remained above the pre-escalation industrial range. UK manufacturing input PPI has only started to edge higher. That lag suggests upstream input pressure is more advanced than the official manufacturing-cost aggregate currently shows.

Figure 2

Figure 2. Non-food input indicators versus UK manufacturing input PPI, rebased to January 2025.

Figure 3 is the retail cross-check. Freight costs, measured by the Baltic Dry Index, rose sharply after the escalation, but the BRC non-food shop-price index has not yet followed in a one-for-one way. This is why the chart is labelled as limited pass-through. Retail prices have not fully absorbed the freight shock yet, which is consistent with retailers still using inventory, hedges and margins to delay shelf-price increases.

To read the rest, visit our latest Substack post, here.