Late last Friday, the U.S. administration announced exemptions for phones, computers, and chips from Trump’s tariffs after imposing a 145% tariff against China – a large exporter of electronics – a few days ago. It is becoming increasingly clear that the upward price pressure linked to tariff announcements stems less from the tariffs themselves and more from the uncertainty surrounding their permanence. Accordingly, Turnleaf has placed greater emphasis on data that reflects broad economic uncertainty through sentiment survey indicators and high-frequency logistics data that track real-time economic activity. Together, our models have responded by pushing our inflation curve upwards as uncertainty intensifies.

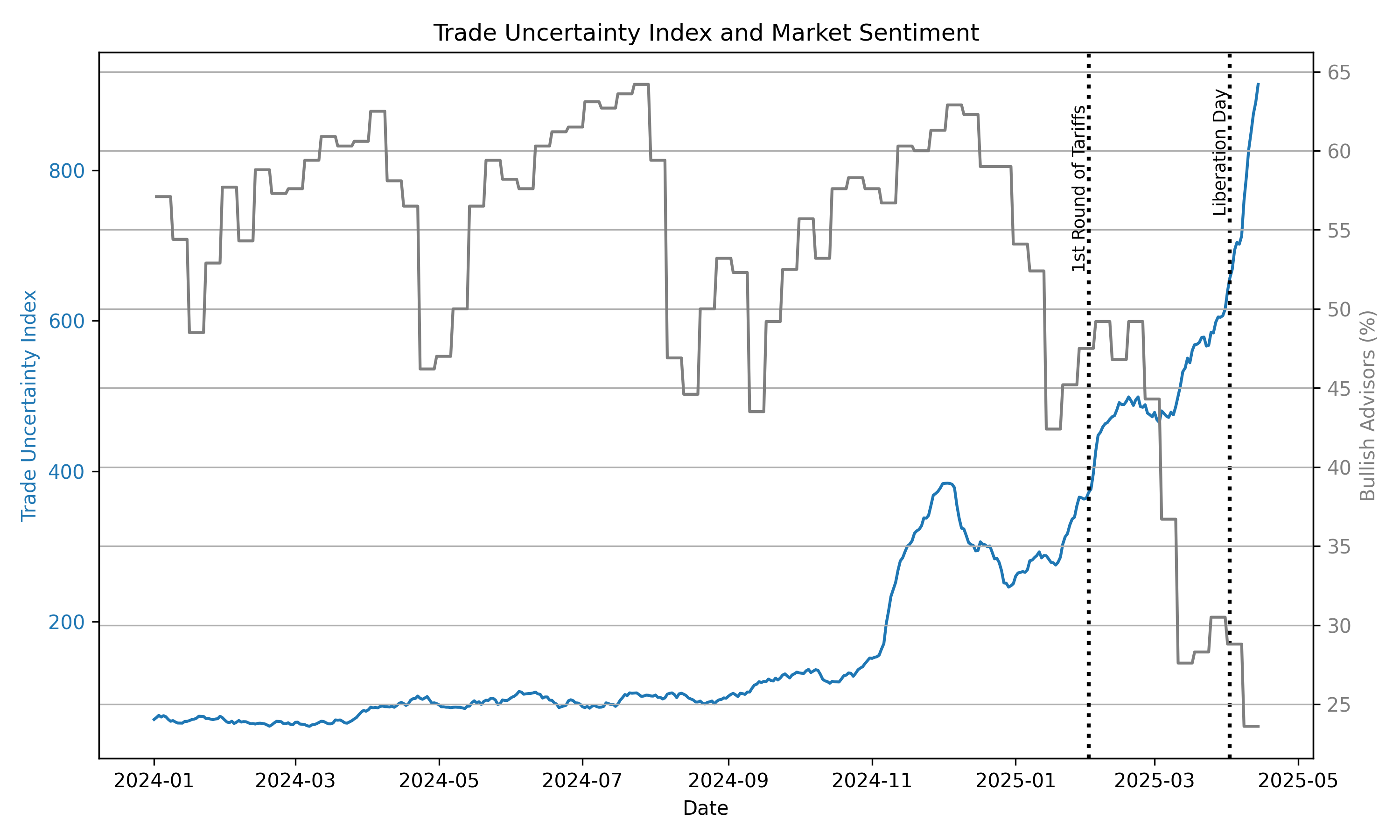

The lack of policy commitment by the U.S. makes it difficult to price in expectations for growth. Last week, markets reacted sharply to sweeping tariff announcements—measures that would have drastically reduced future earnings—only to see those actions reversed days later, with China remaining an exception. Recently, our model has picked up market bullishness as a signal for inflation, which has been inversely related to trade policy uncertainty: the greater the uncertainty, the less bullish the markets (Figure 1). Traders are increasingly responding to this uncertainty with weaker expectations for real economic performance in the coming months as cost pressures rise.

Figure 1

As a result of the tariffs, consumers are likely to face heightened cost pressures in categories such as clothing, food, motor vehicles, and electronics—goods heavily imported from tariff-affected countries. Media attention around shifting policy has triggered a surge in durable goods purchases ahead of tariff implementation, pushing inflation expectations higher.

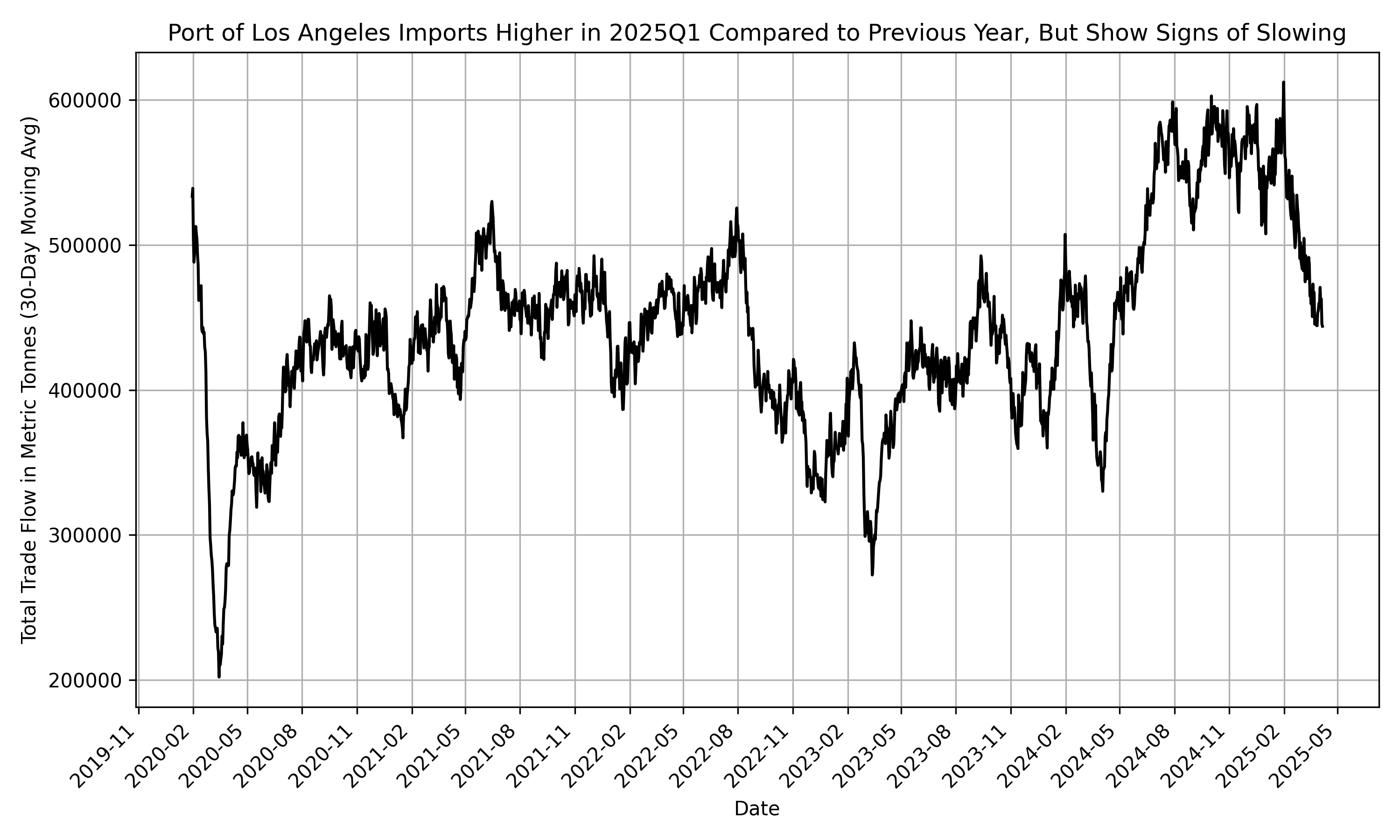

In 2025Q1, the Port of Los Angeles—which handles a significant share of Far East imports like clothing—saw a year-over-year increase in cargo volume, suggesting a rush to front-load inventories ahead of tariffs (Figure 2). However, that trend appears to be slowing as the cost burden of Chinese tariffs weighs on import demand. As that demand weakens, logistics-based indicators including shipping costs, port volumes, and rail and trucking cargo reflected in our model are expected to continue to maintain upward pressure on inflation. These signals will be crucial to monitor as we move through the 90-day tariff reprieve.

Figure 2

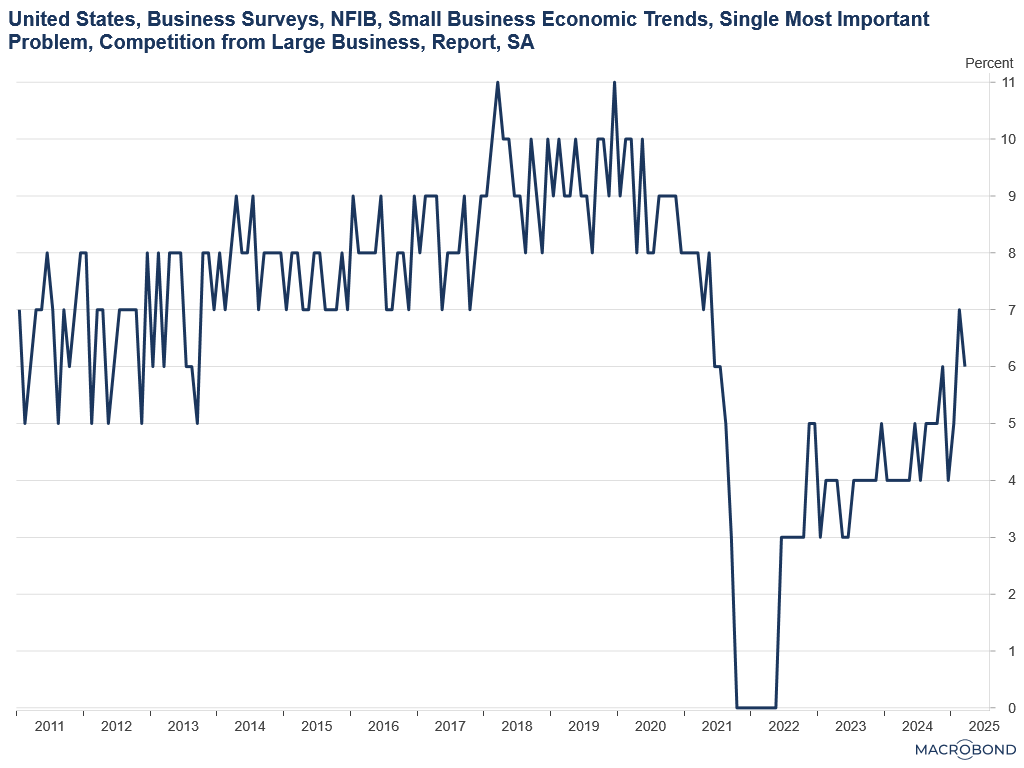

While many firms have front-loaded inventory, the slowdown in import demand indicates a broader pullback. Small firms and consumers are expected to bear the brunt of tariff impacts. According to the National Federation of Independent Business (NFIB), the share of respondents that believe the biggest threat to small firms is larger competitors is growing (Figure 3). These larger firms are better equipped to absorb tariff costs through scale, inventory flexibility, and partial cost absorption. Small businesses, by contrast, have fewer options and are more likely to pass those costs on to consumers, contributing to further inflation. These business sentiment indicators will be crucial in capturing how the tariff burden will be distributed in the coming months.

Figure 3

Turnleaf continues to emphasize a data-driven approach, prioritizing sentiment indicators that track business and consumer behavior, and high-frequency metrics that measure the economy’s real-time response to shifting conditions. As uncertainty lingers, our daily models are signaling growing inflationary pressure at the tail end of the curve. Consumers are already reflecting this uncertainty with elevated one-year inflation expectations, creating conditions that could lead to stagflation—marked by postponed corporate investment and rapid price increases. While Brent crude remains a relevant input, we find that volatility across markets more broadly reflects deepening global uncertainty, adding further pressure to inflation expectations.