Spain headline CPI YoY jumped sharply to 3.3% YoY in March 2026 from 2.3% in February entirely on the back of energy price reversals linked to the Iran conflict and Strait of Hormuz disruption. The market had priced in an even larger shock with consensus standing at 3.7%YoY for CPI. Core CPI YoY came in line with expectations.

While consensus correctly identified the direction and magnitude of tax-related downside impact on energy, it assumed a more gradual transmission, with most of the impact deferred to April. In practice, INE incorporated part of the March 22 energy tax cuts into the flash estimate through statistical completion of the month—embedding the expected price effects into the unobserved late-March data. As a result, a meaningful share of the tax-driven price decline was already reflected in March CPI despite limited post-policy observations, explaining the gap between consensus 3.7% estimate and the 3.3% print. Adjusting for this timing effect, Turnleaf’s and market’s underlying inflation view remains intact.

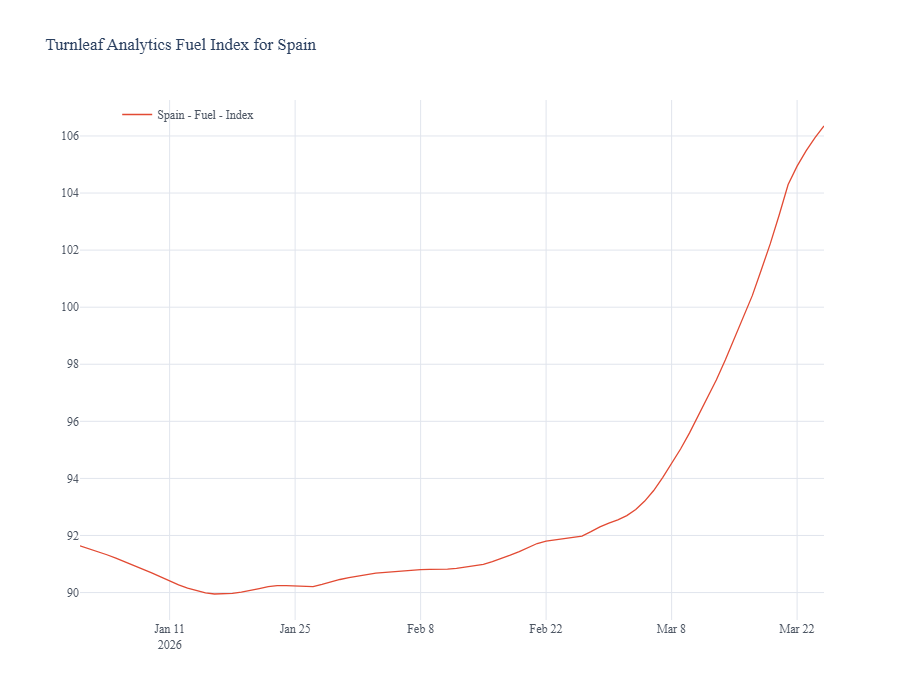

We captured the rise in fuel prices through our proprietary pump-based index, which includes VAT and excise taxes. Despite recent tax cuts—reducing VAT from 21% to 10% and excise duties to EU minimums (≈30c/L impact)—fuel prices still increased, driven by higher oil prices following the Iran conflict. This is consistent with the March flash estimate, which showed a 0.3% rise (Figure 1).

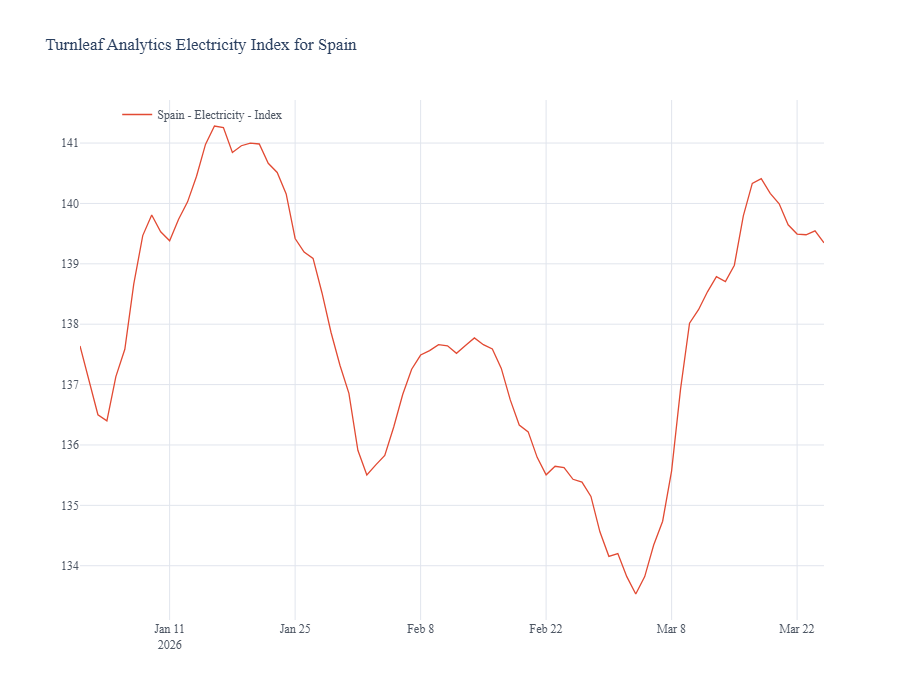

Figure 1 For electricity, Turnleaf’s proprietary PVPC-based index—capturing hourly market-driven price movements but excluding taxes—pointed to a sharp increase in underlying prices from the start of the month (Figure 2). However, the model initially assumed a 21% VAT rate. Late in March 2026, Spain implemented emergency tax cuts, reducing VAT to 10% and the electricity excise to 0.5%, effective immediately. As a result, the observed CPI path diverged from underlying price dynamics, making the timing and pass-through of these tax changes central to explaining the downside surprise in headline inflation.

For electricity, Turnleaf’s proprietary PVPC-based index—capturing hourly market-driven price movements but excluding taxes—pointed to a sharp increase in underlying prices from the start of the month (Figure 2). However, the model initially assumed a 21% VAT rate. Late in March 2026, Spain implemented emergency tax cuts, reducing VAT to 10% and the electricity excise to 0.5%, effective immediately. As a result, the observed CPI path diverged from underlying price dynamics, making the timing and pass-through of these tax changes central to explaining the downside surprise in headline inflation.

Figure 2

A key caveat is the pass-through from Brent crude oil and TTF natural gas into Spanish CPI.

To read the rest of the analysis and gain access to correlation heatmaps between Brent/TTF and inflation subcomponents, visit our latest Substack post here.