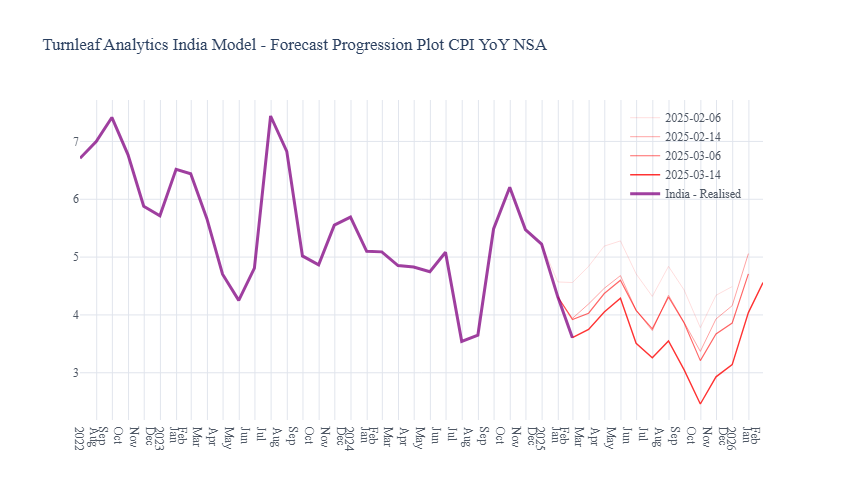

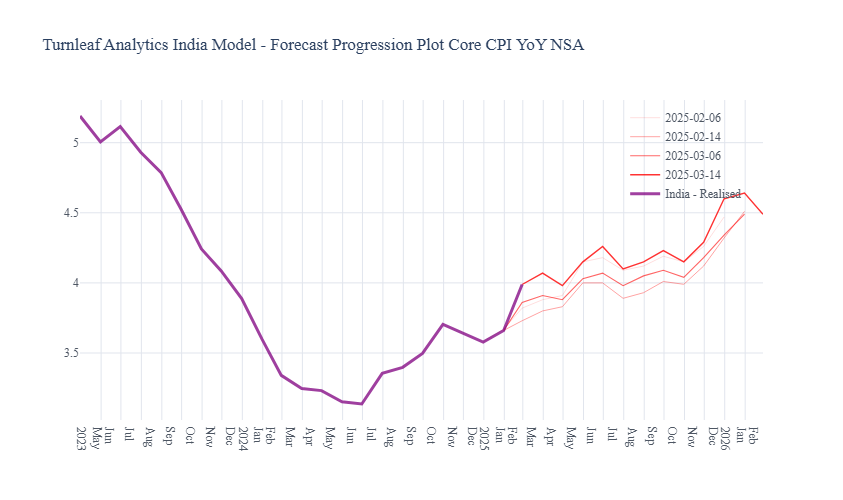

In recent forecasts, Turnleaf has observed an interesting trend in India’s inflation dynamics. While headline inflation has been trending downward, largely driven by a decrease in vegetable prices, core inflation—which excludes food and energy—has been rising (Figure 1). This shift suggests that underlying inflationary pressures may be evolving in ways that go beyond food and energy price movements, prompting a closer look at what this means for India’s broader inflation trajectory.

Figure 1

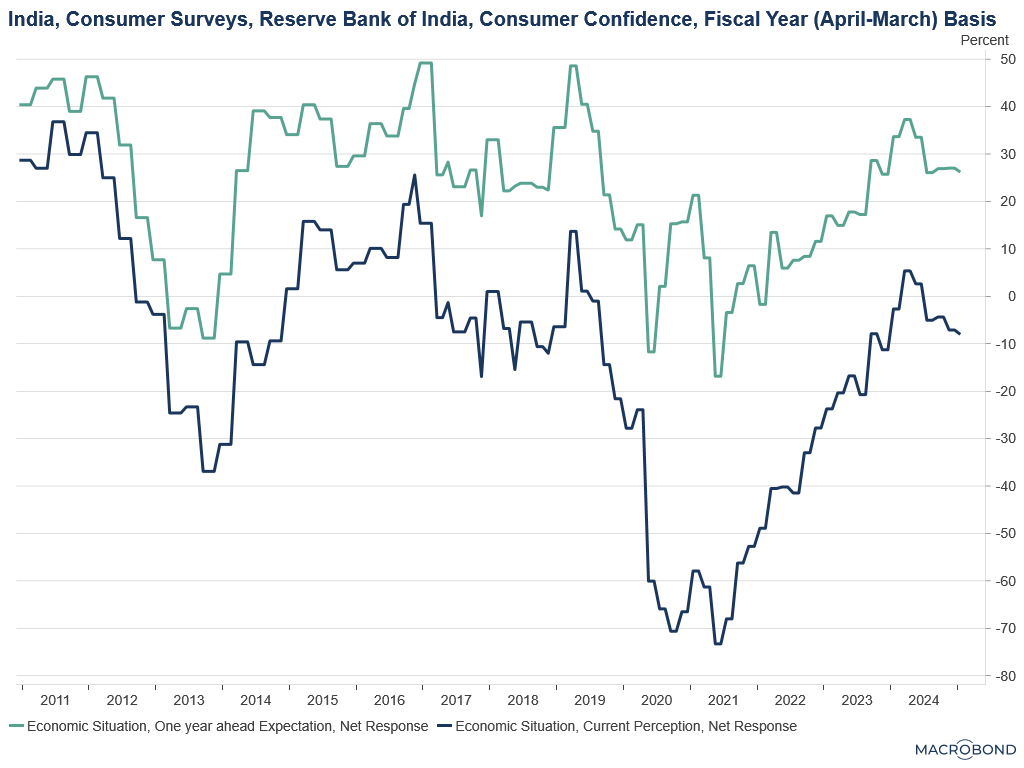

Headline inflation is highly sensitive to food prices, which make up 45% of the consumer basket, potentially masking deeper, persistent inflationary pressures in India’s agrarian economy. Despite the cooling effect of lower food prices on headline inflation, consumer sentiment remains frail, with perceptions of the economic situation worsening and optimism about the future remaining stagnant, driven largely by global uncertainties (Figure 2).

Headline inflation is highly sensitive to food prices, which make up 45% of the consumer basket, potentially masking deeper, persistent inflationary pressures in India’s agrarian economy. Despite the cooling effect of lower food prices on headline inflation, consumer sentiment remains frail, with perceptions of the economic situation worsening and optimism about the future remaining stagnant, driven largely by global uncertainties (Figure 2).

Figure 2

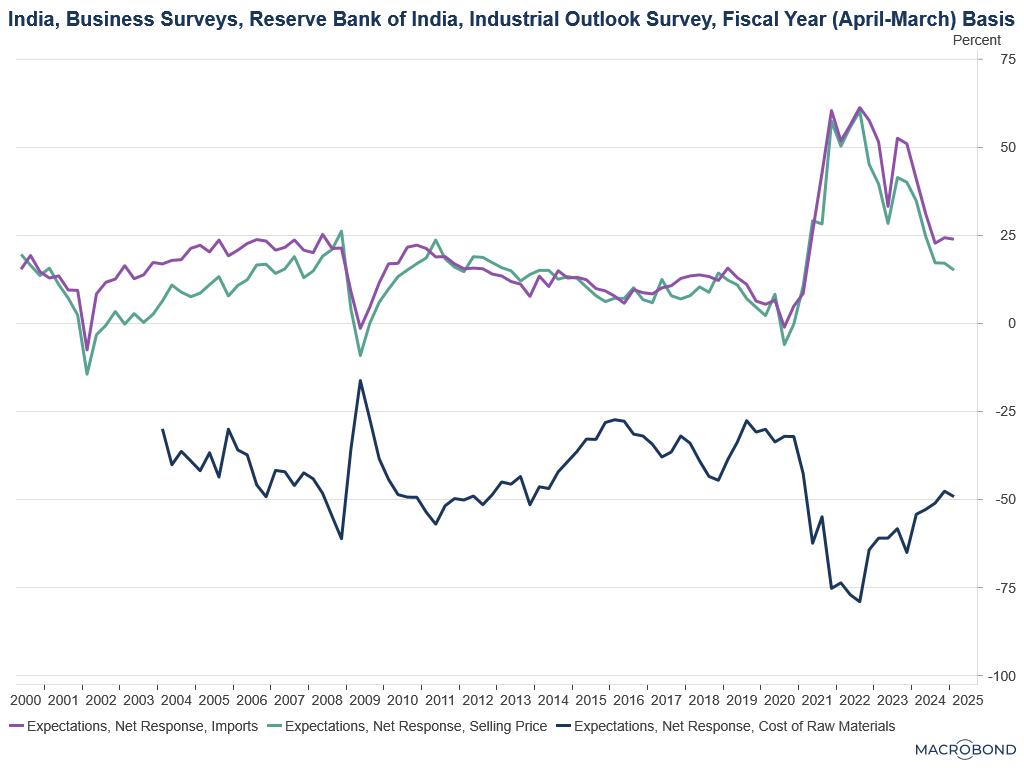

Meanwhile, manufacturers’ expectations for rising imports and selling prices have been declining, while their outlook for lower raw material costs is also waning (Figure 3).

Meanwhile, manufacturers’ expectations for rising imports and selling prices have been declining, while their outlook for lower raw material costs is also waning (Figure 3).

Together, this signals two important trends: first, firms can no longer offset weak consumer demand with cheaper inputs, and second, they have limited ability to raise prices due to subdued demand.

Figure 3

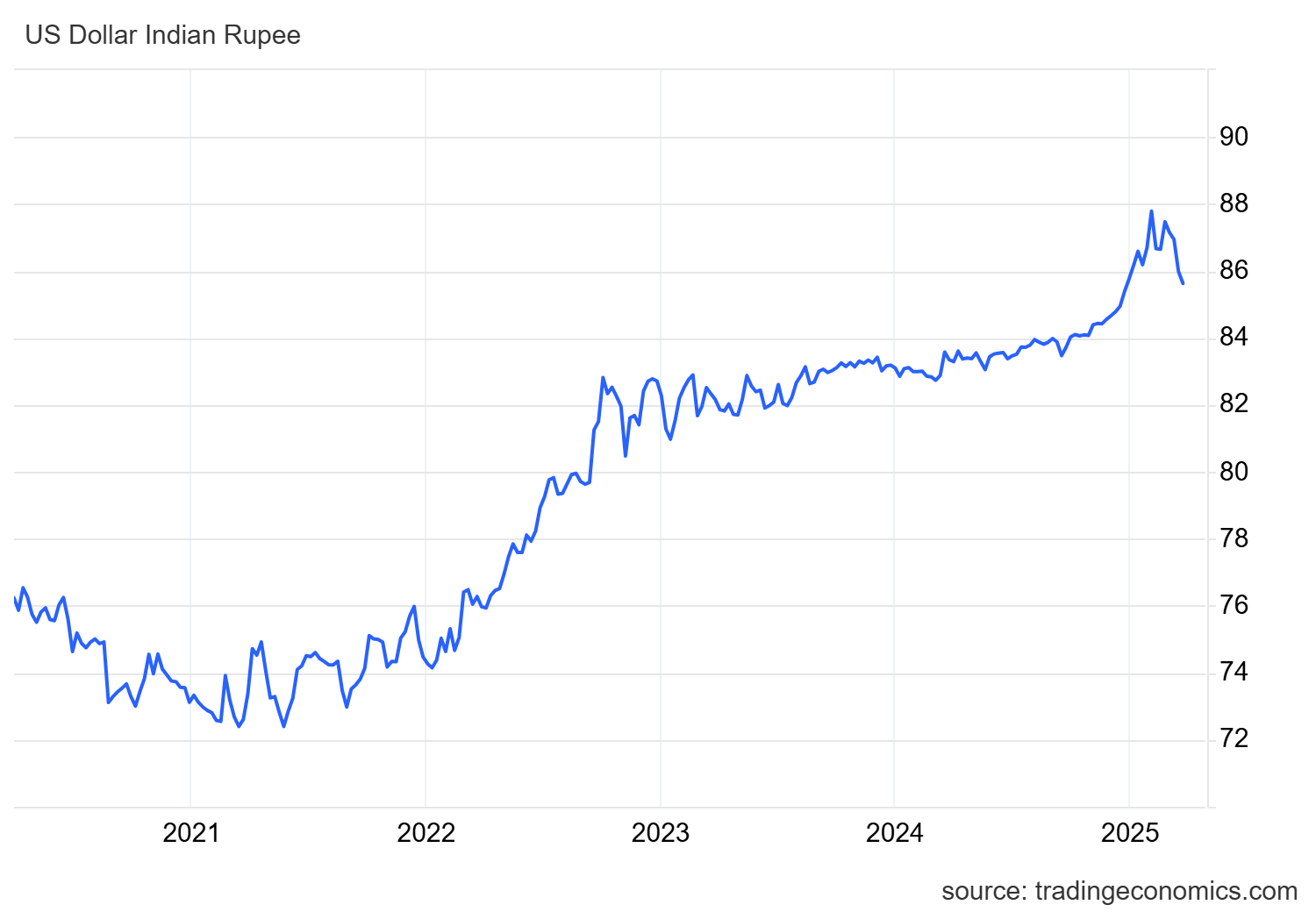

In 2024, low energy prices provided temporary relief to manufacturers, easing cost pressures. However, as energy prices return to more normal levels, manufacturing costs are expected to rise again. Additionally, the Indian rupee has depreciated by 2.65% against the dollar over the past year (Figure 4), with further declines likely given global uncertainty. This depreciation raises the cost of imports, particularly for critical industrial inputs like machinery, electronics, steel, and crude oil, which in turn increases manufacturing costs and puts upward pressure on core inflation.

In 2024, low energy prices provided temporary relief to manufacturers, easing cost pressures. However, as energy prices return to more normal levels, manufacturing costs are expected to rise again. Additionally, the Indian rupee has depreciated by 2.65% against the dollar over the past year (Figure 4), with further declines likely given global uncertainty. This depreciation raises the cost of imports, particularly for critical industrial inputs like machinery, electronics, steel, and crude oil, which in turn increases manufacturing costs and puts upward pressure on core inflation.

Figure 4

Given these trends, any resurgence in demand, especially if food prices continue to fall—could lead firms to increase the pass-through to consumer prices, pushing core inflation higher. If that happens, it could spill over into headline inflation, depending on how much firms raise prices and how food inflation evolves. If consumer demand and industrial production continue to shrink, firms may be forced to pass on rising costs regardless of the economic situation, risking stagflation and threatening India’s economic stability.

Given these trends, any resurgence in demand, especially if food prices continue to fall—could lead firms to increase the pass-through to consumer prices, pushing core inflation higher. If that happens, it could spill over into headline inflation, depending on how much firms raise prices and how food inflation evolves. If consumer demand and industrial production continue to shrink, firms may be forced to pass on rising costs regardless of the economic situation, risking stagflation and threatening India’s economic stability.

Turnleaf will regularly update its forecasts based on new data influenced by external factors, such as global trade dynamics, commodity markets, and currency fluctuations.