The Strait of Hormuz closure is best understood as an inflation shock transmitted through energy logistics. The relevant issue is that usable supply has become harder to move and more expensive to deliver. Prices are set by accessible supply, and the closure has materially reduced the volume of crude and refined product reaching end markets.

Inventories are absorbing the first stage of the disruption. Commercial stocks and strategic reserves can keep the system operating while Gulf flows are constrained, but as buffers are drawn down the market becomes more sensitive to each additional delay or outage. The cost of keeping aviation operating rises even before any visible supply shortage materializes.

Airlines do not wait for supply constraints to materialize before adjusting pricing behavior. Cheap fare buckets are removed first, average fares rise second, and capacity is cut last. A market can appear operationally normal while already becoming inflationary.

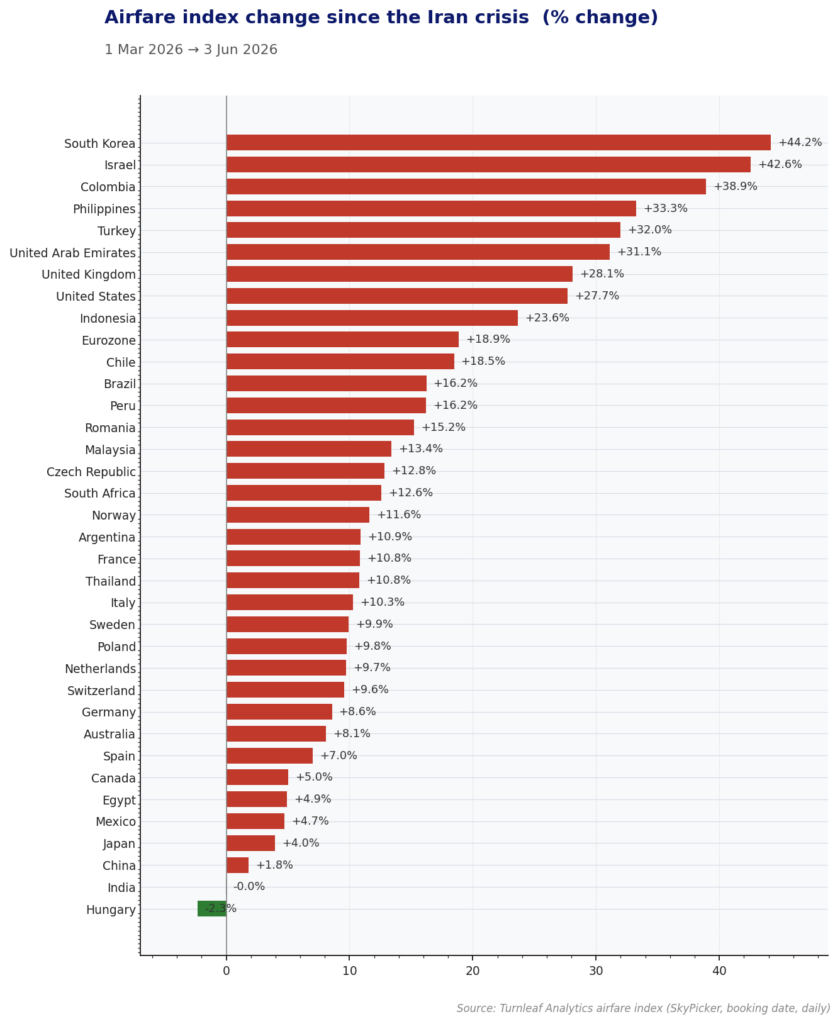

Turnleaf’s airfare indices measure the change in fares before and after the Strait closure (Figure 1). Since March 1, South Korea is up 44.2%, Israel 42.6%, and Colombia 38.9%, with most other markets in the sample showing increases in the range of 10 to 28%. Hungary is the only market to show a decline, at -2.3%.

Figure 1

The distribution is not a proximity ranking. South Korea and Colombia rank among the most affected markets despite their distance from the Gulf, with exposure running through imported energy dependence and dollar-priced fuel procurement. The muted readings at the bottom — Japan at +4.0%, China at +1.8%, India flat — likely reflect larger domestic reserve buffers absorbing the shock rather than low structural exposure.

The key signal to monitor is whether pressure broadens beyond long-haul markets into short-haul and domestic routes. We will continue to update the index daily and flag any evidence of acceleration.