Consumers are waiting for something bad to happen. Industrial weakness and worries about the government dominate the story, and French households are preparing for the worst. As discussed in earlier posts, unemployment concerns are pushing precautionary saving higher and discretionary spending lower. That shift has kept inflation close to 1% YoY, with the balance of risks pointing toward further disinflation. Setting aside cyclical dynamics, Turnleaf’s models are emphasizing consumer behavior. French households are engaging with the economy differently and pulling back from the sectors that used to carry growth.

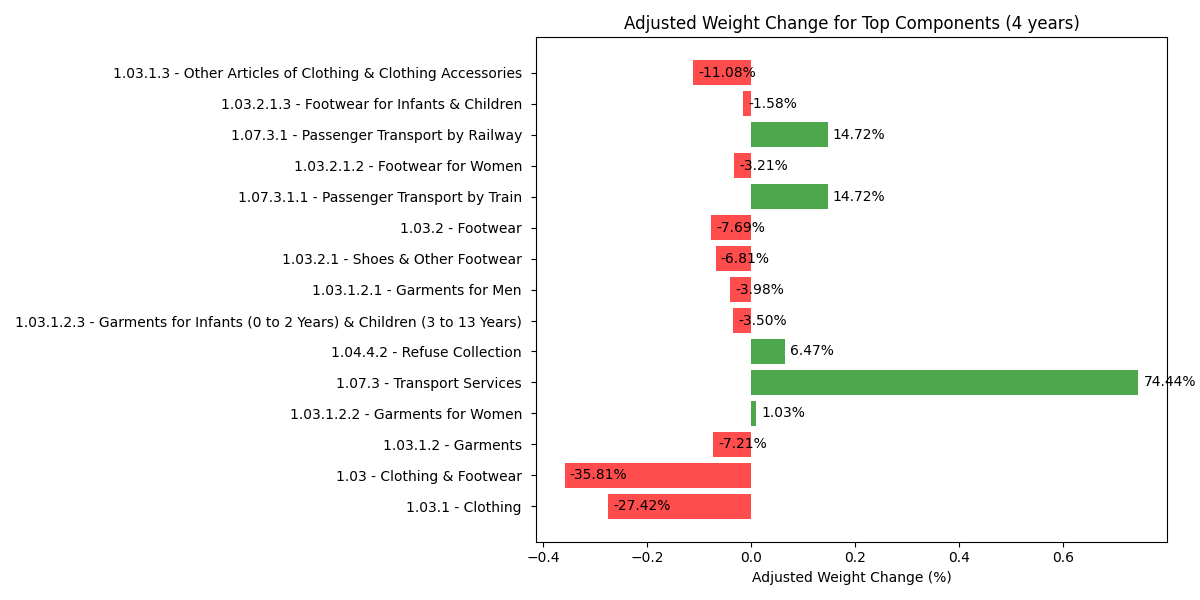

Spending has tilted away from goods like clothing and footwear and toward services like transport. Rail and other mobility services now carry higher CPI weights, reflecting post-pandemic travel normalization, strong tourism, policy support for rail, and wage costs feeding into fares (Figure 1). With goods disinflation carrying less weight, services increasingly set the tone for the headline print, especially given higher services inflation in September 2025 (2.4%YoY vs 2.1%YoY in August 2025).

Figure 1

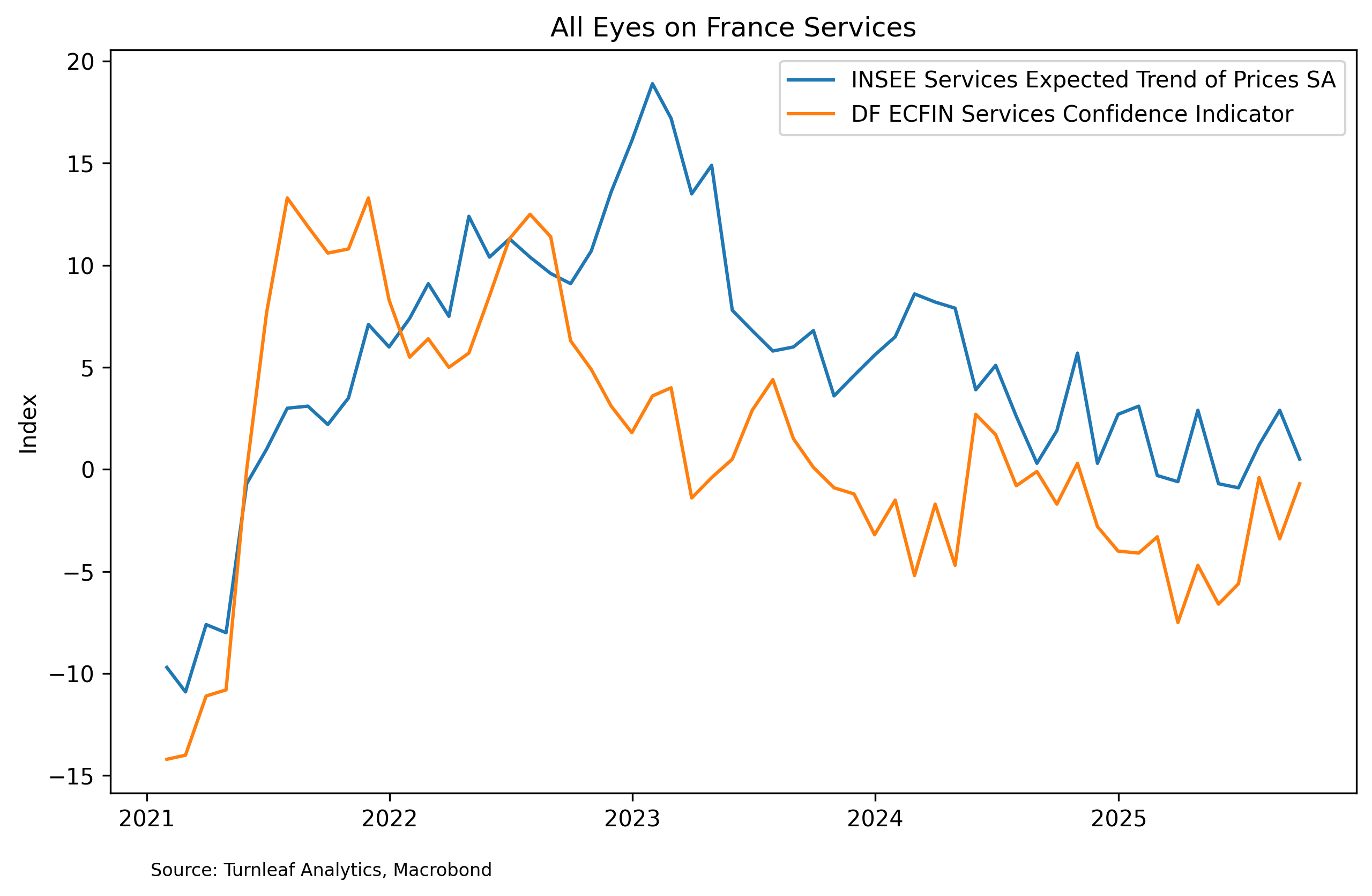

Despite those heavier weights, price expectations for services have eased toward low-positive readings while services confidence remains soft (Figure 2). Firms are finding it harder to lift prices against cautious demand. In our framework, services will contribute less to CPI momentum in the next few months but continue to partially offset goods and energy disinflation.

Figure 2

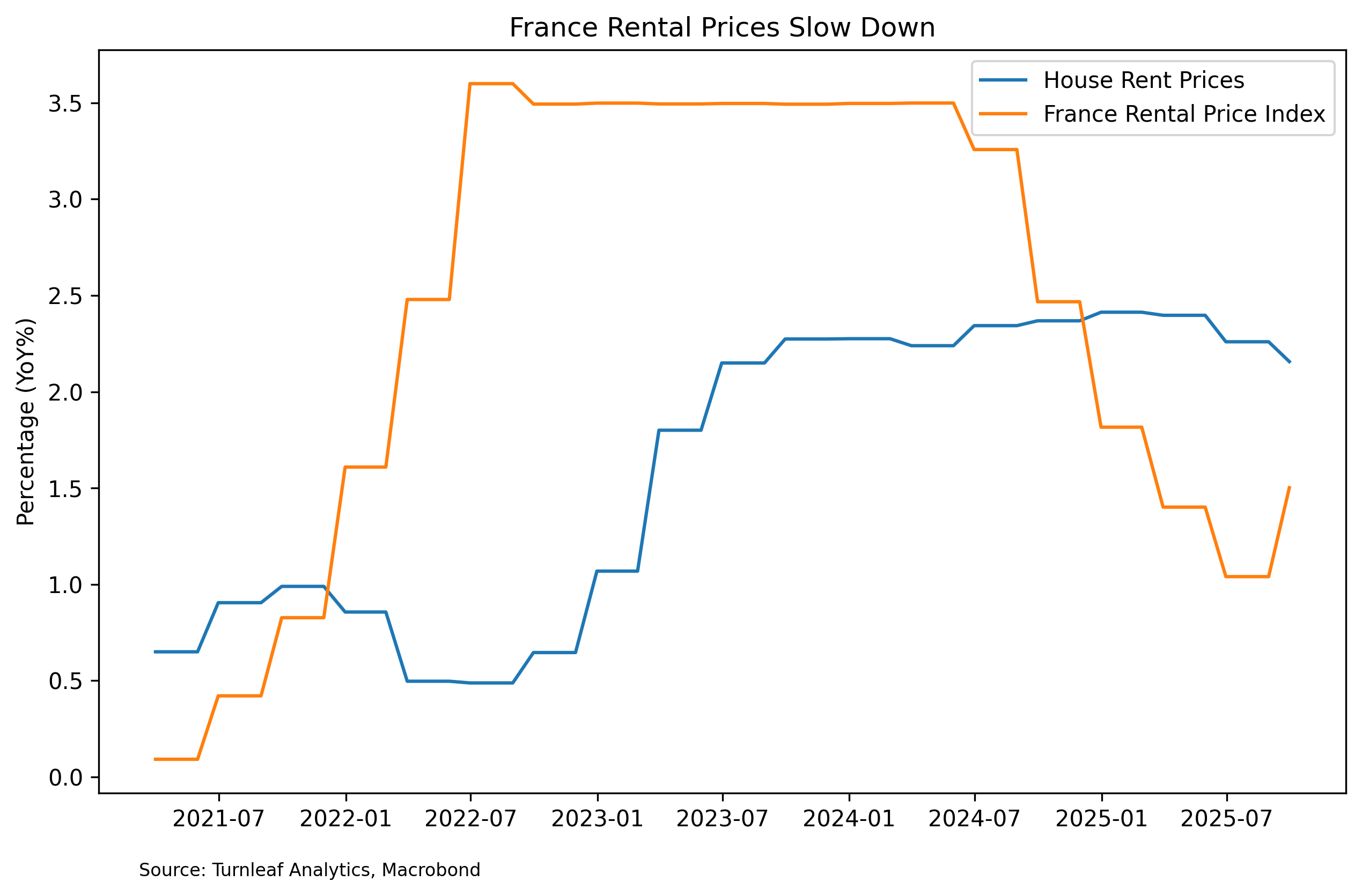

The housing channel tells a similar story and is illustrated in Figure 3. France’s rent revisions are governed by the Indice de Référence des Loyers (IRL), which is tied to CPI ex-tobacco. As disinflation took hold through 2024, the IRL fell from about 3.3% to near 1% by mid-2025, mechanically capping permissible rent increases and cooling housing services. It edged back toward 1.5% late in the year, but with most leases revised annually, the near-term passthrough should be modest. This helps reconcile the model signals. House rent prices are still running a little above 2% YoY and thus flags as inflationary, while the IRL, having dropped sharply, flags as disinflationary. In other words, current rent levels remain elevated, but the lower benchmark constrains upcoming revisions, so any lift from rents in the next prints should be limited rather than a new source of upside pressure.

Figure 3

Meanwhile, energy prices are broadly benign though in last month’s print fuel prices slowed down less than expected given base effects in petroleum. main swing risk is regulated prices, with electricity tariffs typically adjusted around February and changes to local fees and taxes taking effect at the start of the year. These can move the print even when underlying momentum is stable. Rents may add a small sequential lift as IRL-linked adjustments pass through, but contract timing keeps the impulse modest. Industrial activity looks broadly flat over the next couple of months and is unlikely to shape the near-term inflation narrative.

Ultimately, the decisive margin is the consumer. If households continue to save more and resist price increases, services should remain neutral to mildly disinflationary, keeping headline near 1% YoY. If confidence firms, expect more pricing power in transport and other labor-intensive services and accordingly, a higher print (Figure 4).

To read the rest of the article, visit Turnleaf’s Substack.