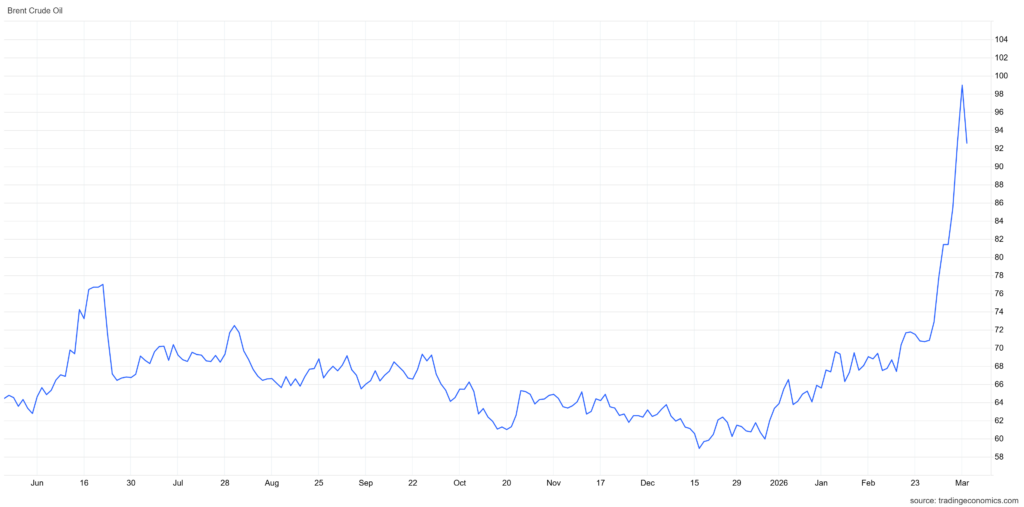

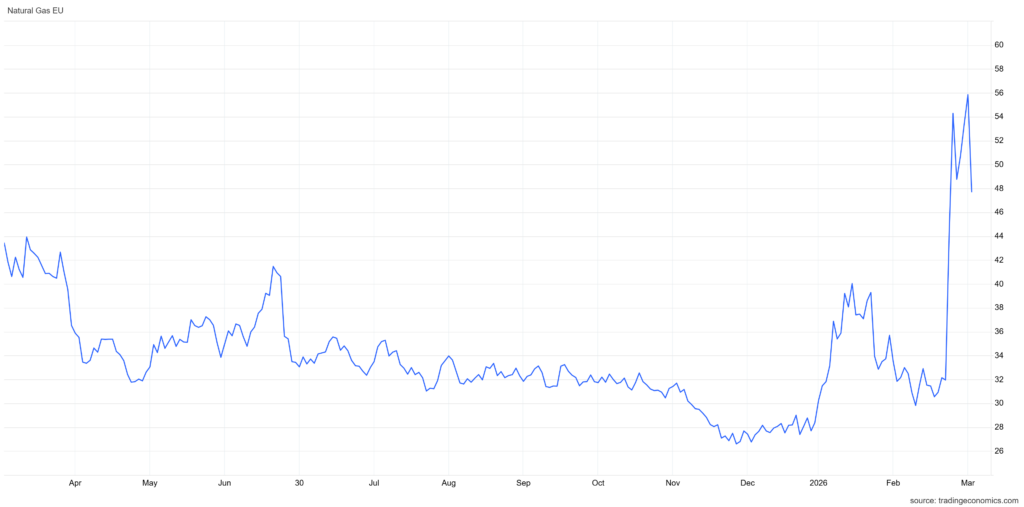

Brent crude has surged from ~$70 to above $100 following the US-Israeli strikes on Iran and the near-closure of the Strait of Hormuz (Figure 1). Dutch TTF natural gas has jumped from the low $30s to above $55/MWh in a parallel move (Figure 2). Contemporaneous (0) and lagged (1-12 month) correlations between these energy benchmarks and monthly CPI inflation across 36 countries reveal how differently this shock will propagate.

Figure 1

Figure 2

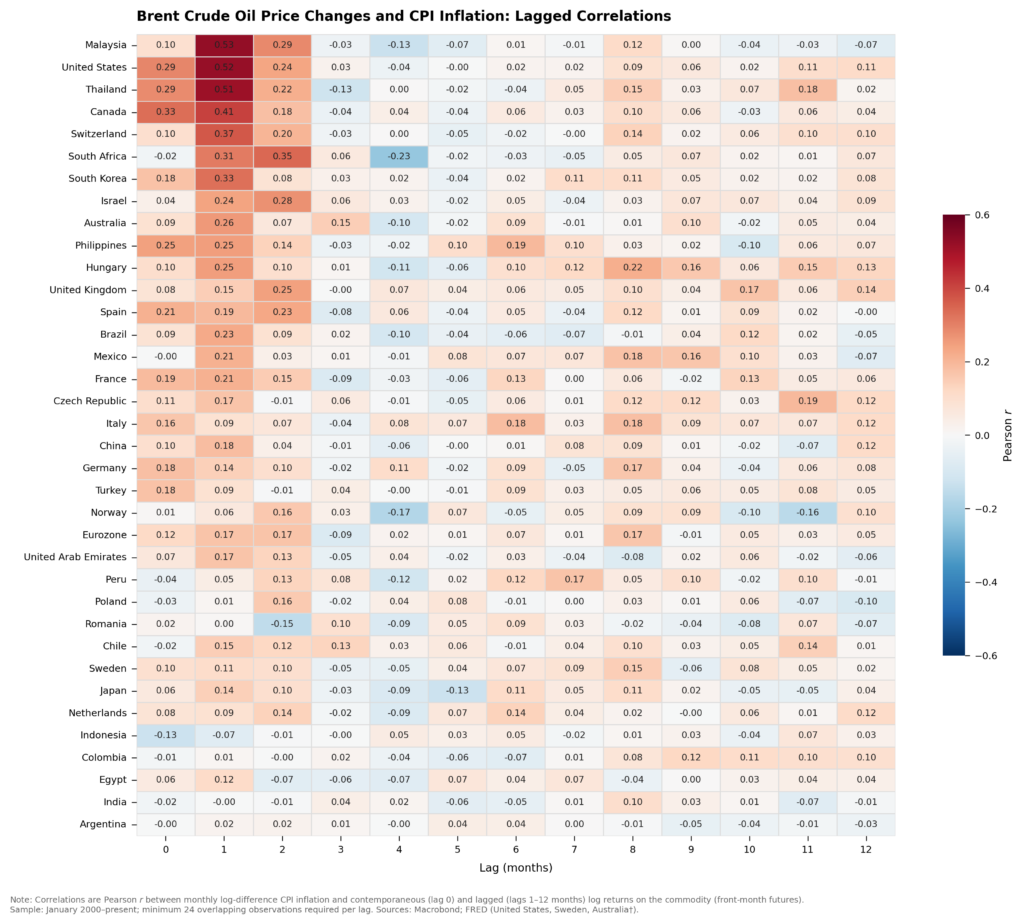

Oil hits the US fast. The Brent-CPI heatmap (Figure 3) shows the US peaking at lag 1, the strongest reading in the sample. US retail fuel prices are set by competitive markets with no administered pricing. Gasoline and motor fuel carry a combined CPI weight above 4%, and price changes at the pump flow into the index within one reporting cycle. The $30/bbl Brent move visible in the vertical spike in Figure 1 will register in March–April CPI prints almost mechanically. Canada, Thailand, and Malaysia show similar rapid pass-through profiles in Figure 3 for the same structural reasons.

Figure 3

Europe’s oil response is muted by the tax wedge. The Eurozone row in Figure 3 peaks at lag 1 at roughly a third of the US equivalent. Fuel taxes (excise duties plus VAT) account for 50–65% of the retail price across France, Germany, Italy, and the Netherlands. Because excise duties are levied per litre rather than ad valorem, a doubling of crude translates into a far smaller percentage increase at the pump. Governments also retain the option to temporarily cut duties to absorb the shock, as France and Germany both did during the 2022 spike. The weak, diffuse colouring across the European rows in Figure 3 reflects this structural dampening.

The UK sits in between. Figure 3 shows the UK Brent-CPI correlation peaking at lag 2, reflecting Ofgem’s quarterly energy price cap. Wholesale energy cost changes are not passed to households immediately and instead, the cap is recalculated each quarter based on a backward-looking observation window. This regulatory structure introduces a built-in 1–2 quarter delay between a wholesale price spike and its appearance in CPI.

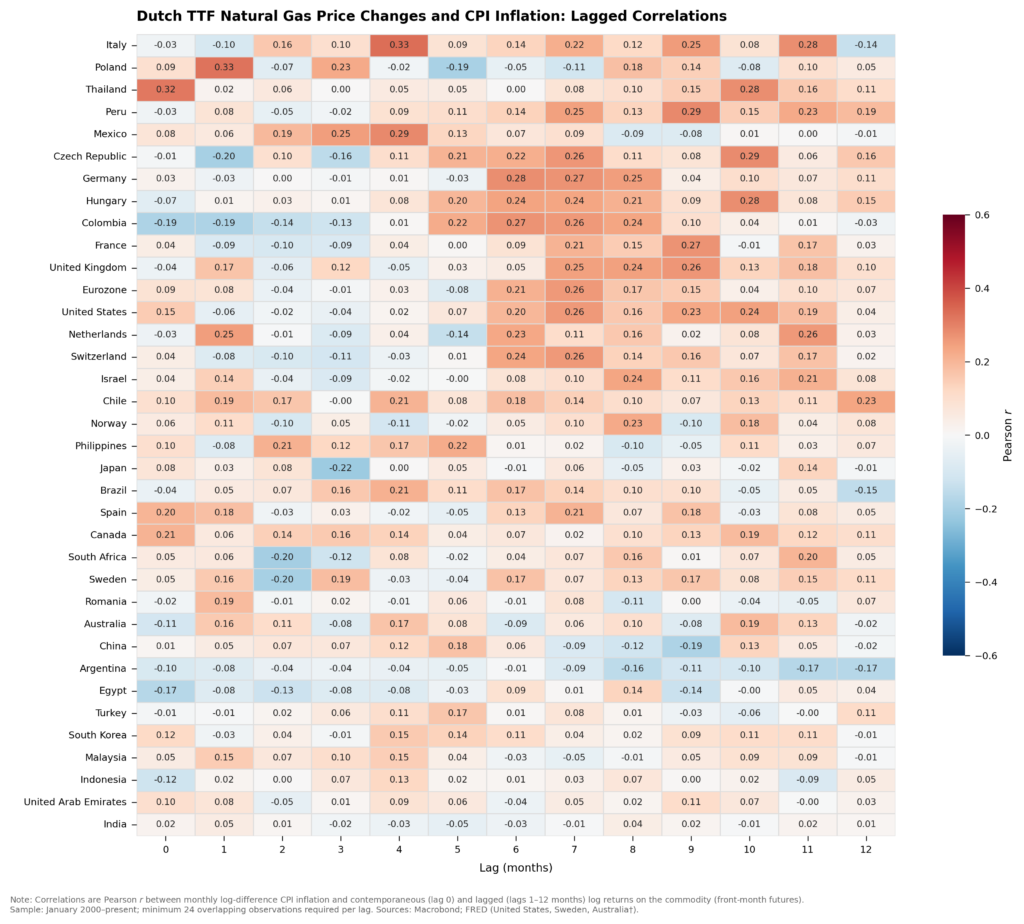

Gas is Europe’s real (delayed) vulnerability. The TTF-CPI heatmap (Figure 4) tells a strikingly different story from the Brent panel. European economies dominate the warm-shaded zone, but the peak correlations are concentrated at lags 5–8 for Italy, Germany, and the UK. Two primary mechanisms drive this delay. First, regulated utility tariffs in most European markets reset on fixed schedules (quarterly or semi-annually), creating discrete pass-through windows. Second, household heating costs depend on billing cycles and contract renewal dates, which vary by country but typically impose a 3–6 month lag between wholesale price movements and the consumer bill.

Figure 4

Implications on Turnleaf Forecasts

The spike visible in Figure 1 will produce a small near-term fuel price uptick dampened by the tax wedge (the muted European rows in Figure 3), while the spike in Figure 2 will drive a larger and more persistent gas-driven inflation impulse arriving in Q3–Q4 2026 as the strong lag 5–8 correlations in Figure 4 imply utility tariff resets, industrial cost pass-through, and heating bill adjustments feeding into CPI simultaneously. The Hormuz disruption is already feeding into our real-time inflation nowcasts via the proprietary alternative and high-frequency data we track across 36 countries, including daily shipping flows, port activity, and commodity prices.

The key factor to watch will be emerging regulatory intervention which will determine whether the historical pass-through coefficients hold or compress as they did in 2022 during the onset of the war in Ukraine. So far, several countries have already responded to higher energy prices:

- In the UK, Ofgem’s April–June price cap has already been set at £1,641, meaning households on variable tariffs are shielded from the current spike until at least July. However, Cornwall Insight’s forecast for the July–September cap has surged to £1,801, an increase of £160 on April’s level, driven by elevated wholesale gas prices. Each of these interventions will compress the historical pass-through coefficients documented in Figures 3 and 4, but only temporarily and at mounting fiscal cost.

- Hungary reimposed fuel price caps on Monday, with Orbán capping petrol at 595 forints per litre and diesel at 615 forints, alongside a release of state reserves.

- South Korea announced its first fuel price cap in 30 years, with President Lee Jae Myung ordering authorities to “swiftly introduce and boldly implement” a maximum price system for petroleum products. Seoul has also unveiled a 100 trillion won ($68.3 billion) stabilisation fund to subsidise energy costs for households and industry.

- China’s NDRC raised retail gasoline and diesel price caps by 695 and 670 yuan per metric ton respectively from Tuesday, the largest adjustment since March 2022, under its 10-working-day mechanism that links domestic prices to international crude. That mechanism includes a built-in ceiling at $130 per barrel, above which retail prices are generally frozen, meaning pass-through will cap out if Brent keeps climbing. Beijing also halted refinery exports of diesel and petrol on 5 March to preserve domestic supply.