Recently, housing prices in the Czech Republic have increasingly exerted upward pressure on inflation. Our June 2025 Forecast Word Cloud highlights the primary drivers influencing our projections. Consistent with recent economic trends, our forecast places particular emphasis on indicators related to construction and housing, which continue to drive upward pricing pressures.

Word Cloud Contribution Plot, Czech Republic, May 2025

Subscribers can gain insights into the key drivers influencing Turnleaf’s CPI forecasts by examining our Word Cloud. Each term represents an economic indicator’s relative importance in our CPI model. The size of each word reflects its contribution magnitude to overall inflation predictions, helping subscribers quickly identify the most influential factors. The color coding further clarifies each indicator’s impact direction: blue words represent indicators with a disinflationary effect on CPI, while red words highlight inflationary factors. For instance, ‘Inflation Market Forecast’ is large, indicating their significant weight in the model, while its color suggests whether it contribute to higher or lower inflation trends. This Word Cloud enables a quick, visual analysis of the complex landscape of inflationary and disinflationary influences in our forecasting model.

These housing market dynamics are especially impactful due to housing’s substantial weighting in the CPI basket—over 10% from imputed rents and an additional 3% from actual housing rents. The Price Index of Dwellings (Figure 1), covering new and existing residential properties, has shown steady YoY growth since early 2025.

Analyzing underlying supply-demand dynamics helps explain these rising prices. Our June 2025 forecast specifically highlighted structural market shifts driven by new quarterly data, clarifying recent intensified price pressures.

Figure 1

Construction industry sentiment in the Czech Republic has notably strengthened recently, driven by robust housing demand (Figure 2).

Figure 2

This increased demand has significantly raised wages in the construction sector, outpacing overall average wage growth as builders compete to meet surging housing demand (Figure 3).

Figure 3

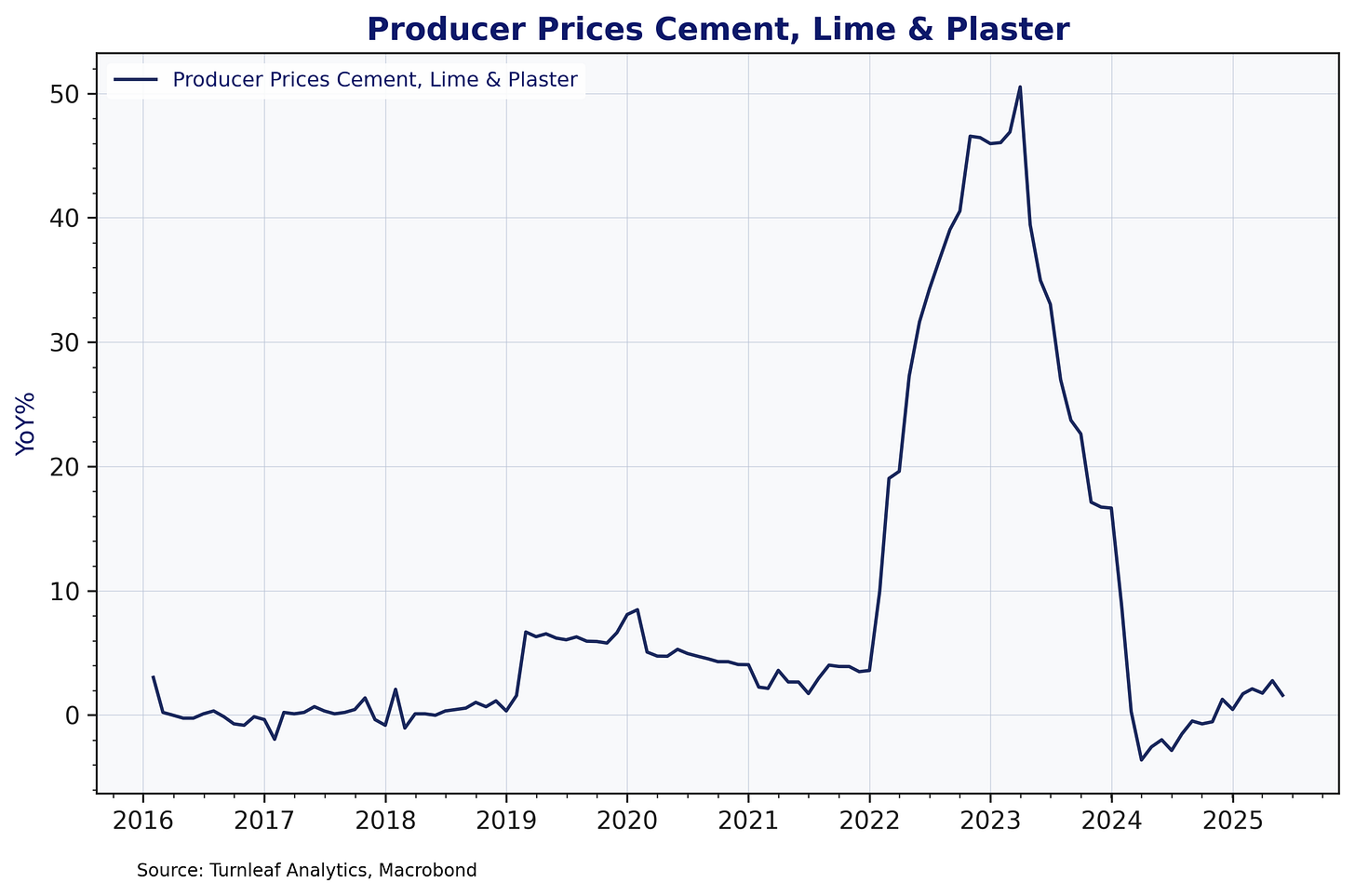

Construction input prices are also rising. Although producer prices for cement, lime, and plaster remain moderate compared to 2022–2024 peaks, their recent upward trajectory signals growing cost pressures as demand stays strong (Figure 4).

Figure 4

Evaluating Czech consumer finances helps contextualize rising housing demand. While disposable income growth aligned with high inflation until the end of 2024, recent trends show continued steady income growth amid moderating inflation, supported by strong real wage increases (Figure 5). Additionally, the Czech National Bank’s stabilization of inflation and ongoing rate cuts have lowered mortgage rates, boosting housing affordability.

Figure 5

Lower mortgage rates combined with strong wage growth and accumulated savings enhance consumer purchasing power, sustaining upward pressure on housing prices. Continued wage and income growth remain critical to this dynamic. Despite housing-driven pressures, we expect overall inflation to decline below 2% by year-end due to substantial moderation in electricity and food prices, together accounting for nearly 20% of CPI (Figure 6).

Figure 6

Nonetheless, substantial risks persist from potential supply shocks that could significantly impact construction input costs. Given the increasing economic importance of the construction sector, we will maintain close monitoring of supply chains and input prices to ensure accuracy in our future forecasts.